Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

The Hidden Time Bomb in AI Finance

Why Electricians Now Out-Earn Software Engineers

The Apartment Glut Changing America’s Rental Market

Why Community Colleges Are Winning Again

The Liquidity Trap Hidden Inside Leveraged ETFs

When Losing Money Pays: America's Broken Market Logic

Something unusual is happening in the American stock market, and it is not the kind of unusual that tends to resolve quietly. Over the past year, companies that lose money have outperformed companies that make money. Not marginally. Not in one obscure corner of the market. Across a broad, measurable swath of U.S. equities, the reward for burning cash has exceeded the reward for generating it. Torsten Sløk, Partner and Chief Economist at Apollo Global Management, flagged the anomaly in a note published June 20, 2026. His language was blunt: "Something is broken in price discovery when companies with negative earnings keep outperforming companies with positive earnings." That sentence, terse and precise, is one of the more damning diagnoses of American capital markets in recent memory. It deserves to be examined not as a curiosity, but as a structural warning one arriving at precisely the moment when the broader architecture of market risk is shifting in ways that could make any correction far more painful than it appears on the surface.

The Data Behind the Anomaly

The evidence is not subtle. Within the Russell 2000 small-cap index a proxy for the riskier, less-established tier of American business approximately 806 of roughly 2,000 constituent companies carry negative trailing earnings. That is roughly 40% of the index burning cash while their share prices climb. Since the market bottomed following the Liberation Day tariff shock in early April 2025, the Russell 2000 has surged nearly 44% off its low. But unprofitable companies within that index have done even better, posting gains of roughly 60%, decisively outpacing their profitable counterparts, who gained approximately 9% over a comparable window, according to Apollo data.

Sløk first flagged this divergence in November 2023, warning that loss-making firms would be especially vulnerable to high rates and slowing growth. Two and a half years later, those same names are leading the market higher. That reversal is the puzzle that defines the current moment. The gap, rather than closing as fundamentals reasserted themselves, has only widened through mid-2026. The mechanism holding it open appears to be a combination of cheap speculative capital, AI-adjacent enthusiasm, and a persistent investor appetite for narrative over accounting. Morgan Stanley's Lisa Shalett has noted that many small-cap firms carry a cost of capital that already exceeds their return on assets a definition of value destruction that markets are, for now, choosing to ignore.

Meanwhile, the concentration problem at the other end of the market is equally striking. Apollo's own data shows that since January 2026, the entire gain in the S&P 500 has come from just two corners of the market: AI-linked stocks and energy. Everything else in the S&P 500 is, as a basket, trading below where it started the year. A market that looks diversified by the numbers is, in practice, running on two engines. And one of those engines the AI trade is now showing signs of serious mechanical stress.

The AI Spending Anxiety and the Nasdaq's Five-Day Skid

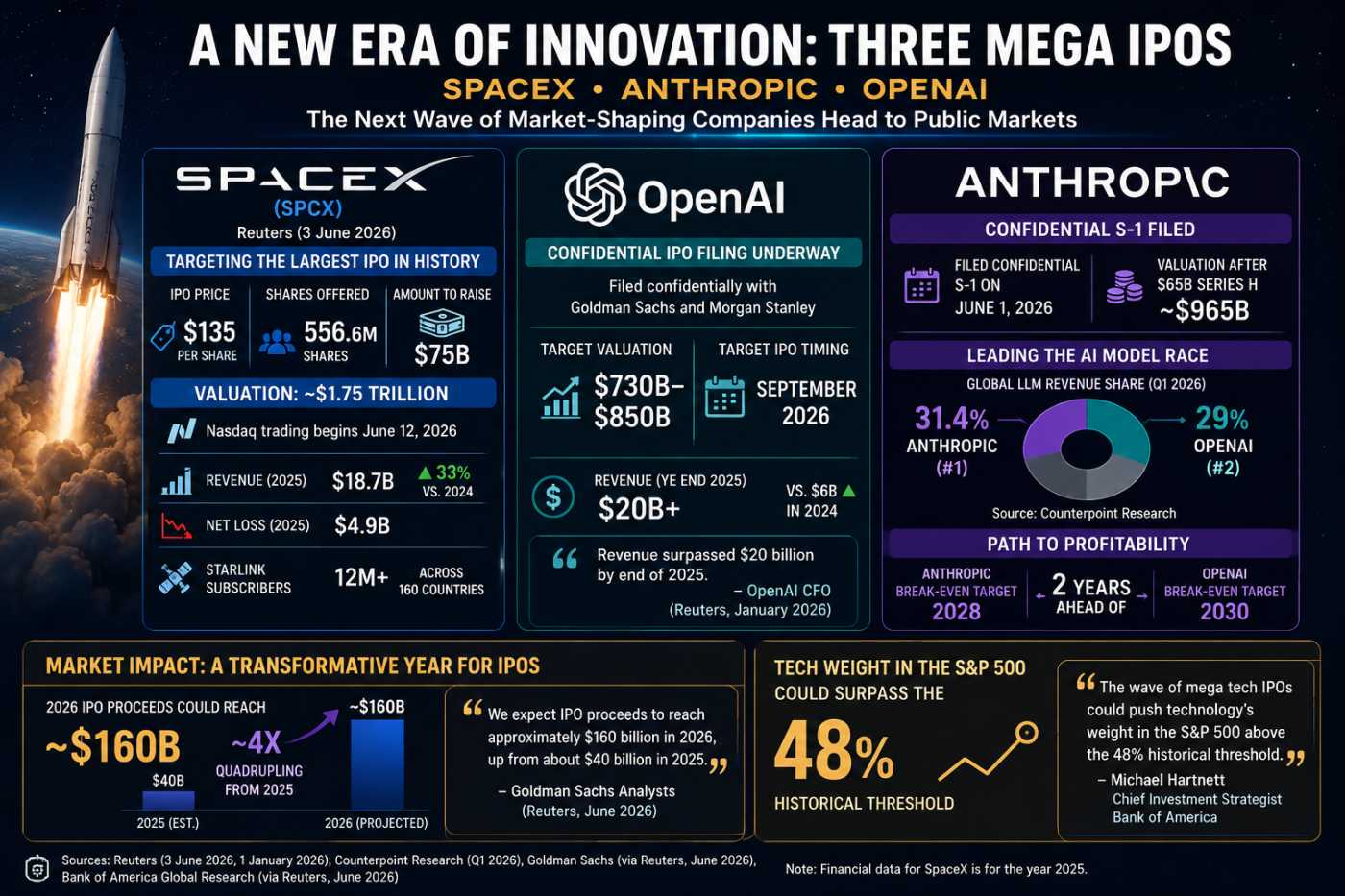

The Nasdaq Composite posted five consecutive sessions of losses through June 27, 2026, its worst such streak since February, with the index falling roughly 4.6% on the week ending June 27. The proximate cause was a familiar cluster of anxieties around AI infrastructure spending. OpenAI's reported leaning toward delaying its IPO until 2027 spooked in part by SpaceX's turbulent post-debut collapse from an intraday high above $225 back toward its $135 listing price rattled chip stocks because it raised a pointed question: if the biggest buyer of AI compute cannot yet justify going public at a $1 trillion valuation while burning $21 billion annually, how durable is the spending that underlies the entire AI infrastructure trade?

JPMorgan analysts noted that the OpenAI delay raised concerns about the "sustainability of their infrastructure spending given the delay in funding from the capital markets." That framing matters. The AI infrastructure buildout data centers, chip demand, power contracts is not funded by profit. It is funded by capital raises, private credit, and the expectation that public markets will eventually absorb the risk. When that expectation wobbles, as it visibly did this week, the entire chain of dependencies shudders. Nvidia, Broadcom, AMD, and the broader semiconductor ecosystem all felt the pressure as investors rotated out of technology and into healthcare, industrials, and defensive sectors. By late June 2026, 63% of S&P 500 stocks were trading above their 50-day moving average a sign of improving breadth but that breadth improvement came precisely because the mega-cap AI names were being sold.

What is structurally troubling here is not the rotation itself. Rotation is normal. What is troubling is what the rotation reveals: that a multi-trillion-dollar bull market has been quietly running on the fiction that a handful of deeply unprofitable AI companies represent durable economic value at trillion-dollar valuations. The speculative premium embedded in those valuations requires constant narrative maintenance new product launches, new revenue announcements, new IPO milestones to hold in place. When any of those narrative anchors slip, the repricing can be sudden.

Bank of America's Hawkish Pivot and the Rate Hike Reckoning

Against this already fragile backdrop, Bank of America delivered what may be the most consequential single forecast revision of 2026. On June 22, economist Aditya Bhave reversed the bank's prior hold forecast held as recently as the prior week and now expects three consecutive 25-basis-point rate hikes from the Federal Reserve in September, October, and December. The projected moves would lift the federal funds rate from its current 3.50%-3.75% range to 4.25%-4.50%. "The Fed's inflation problem has gotten unambiguously worse," Bhave wrote, pointing to core PCE trending toward 3.5%, housing-driven disinflation that has "mostly run its course," and energy costs elevated by the Iran conflict adding persistent pressure.

The speed of that reversal from hold to three hikes in a single week is itself a signal. It suggests that the inflation picture in mid-2026 is moving faster than any of the major Wall Street forecasting desks can model. Deutsche Bank has also turned hawkish, projecting two hikes in September and December. CME FedWatch data as of late June shows traders assigning 72.8% odds to a September hike, 80.6% to October, and 87.9% to December a striking market-implied convergence with BofA's most aggressive call. New Fed Chair Kevin Warsh, in his first FOMC meeting on June 17, referred to "price stability" approximately a dozen times, a repetition that markets read as unambiguous hawkish intent. The June FOMC held rates at 3.50%-3.75% but flagged that further increases could be warranted, with nine of 18 committee members projecting at least one hike by year-end.

The implications for a market structured around the broken price discovery Sløk described are severe. The entire outperformance of unprofitable companies depends on an environment where capital is cheap and speculative appetite is high. Both of those conditions are now directly threatened by a Fed tightening cycle. Companies with negative earnings and high cash burn rates are among the most interest-rate-sensitive instruments in the equity market. Their valuations are effectively duration instruments: the longer the timeline to profitability, the more sensitive they are to changes in the discount rate. Three rate hikes, compressing financial conditions into the second half of 2026, would reprice that risk with force.

A Structural Problem, Not a Temporary Mispricing

To understand why this moment is different from prior bouts of speculative excess, it helps to trace how American capital markets arrived here. The pandemic triggered an unprecedented monetary and fiscal response. Interest rates went to zero, then stayed there. In that environment, the conventional logic of equity valuation the idea that a company's worth is the discounted present value of its future cash flows became almost meaningless. When the discount rate approaches zero, a dollar of earnings fifty years from now is worth nearly as much as a dollar of earnings today. That mathematical reality, applied to a market full of technology companies with compelling long-term stories, produced a systematic bias toward narrative.

Companies that could tell a better story more users, more TAM, more AI exposure attracted more capital than companies that could show a better income statement. The market began rewarding the promise of future earnings more richly than it rewarded actual current earnings. Momentum became the dominant factor. A company's stock going up became a reason, in and of itself, for other investors to buy it. This is the environment in which the broken price discovery Sløk identified took root. It did not appear overnight. It was cultivated over years of zero interest rates, quantitative easing, and a venture-capital infrastructure that learned to channel extraordinary sums into growth-over-profitability business models.

The problem is that this structure now has to survive a world of higher-for-longer rates, sticky inflation, and a Fed chair who used the phrase "price stability" twelve times in a single press conference. Apollo's own 2026 macro outlook framed the U.S. in a stagflationary environment: slowing growth combined with inflation above the Fed's 2% target, a combination that historically has been unkind to both equities and bonds simultaneously. With Q4 2025 GDP growth recorded at just 0.5% annualized, and the full-year 2025 expansion described by EY-Parthenon chief economist Gregory Daco as "the year that could have been," the underlying economic foundation for sustaining trillion-dollar AI narratives is considerably weaker than the surface-level index performance suggests.

When the Momentum Trade Meets the Rate Hike Cycle

The collision between broken price discovery and a tightening Fed is not a theoretical risk. It is the operative market scenario as of late June 2026. The Schwab Center for Financial Research noted that the rolling 52-week correlation between the cap-weighted and equal-weighted S&P 500 is at its lowest since 2003 a measure of how extreme the divergence has become between a handful of mega-cap AI names and the rest of the market. Kevin Gordon, head of macro research and strategy at SCFR, highlighted this divergence as a structural feature, not a temporary glitch.

What makes the coming months particularly hazardous is the interaction effect. Rising rates compress multiples most aggressively for the longest-duration assets precisely the unprofitable, speculative-momentum names that have led the market over the past year. At the same time, a slowing economy, where CEO confidence fell to 47 in Q2 2026 from 59 in Q1 (any reading below 50 signals negative outlooks outnumber positive ones), reduces the earnings power of the profitable companies that might otherwise offer refuge. The result is a market where the expensive things are getting more expensive to hold and the cheap things are not actually cheap they are just less overvalued.

Sløk's warning about broken price discovery is, at its core, a warning about the bill that comes due when speculative cycles end. Markets can sustain the mispricing of risk for longer than any rational framework would predict. But they cannot sustain it indefinitely against a Fed explicitly moving to tighten, an inflation backdrop described as getting "unambiguously worse," an AI spending cycle whose largest participant cannot yet justify going public, and an underlying economy that grew at 0.5% in the final quarter of 2025. The conditions that allowed unprofitable companies to outperform profitable ones are, one by one, being removed. What happens when the last one goes is not a question the data can answer in advance. But the data available today makes the direction of travel difficult to argue with.

If you have enjoyed reading, spread the word:

SpaceX IPO Spawned a New Speculation Machine

How SpaceX Gave Main Street a Seat at the IPO

How Workers Became Capitalists

The Inflation Wave the Fed Can't Navigate