Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

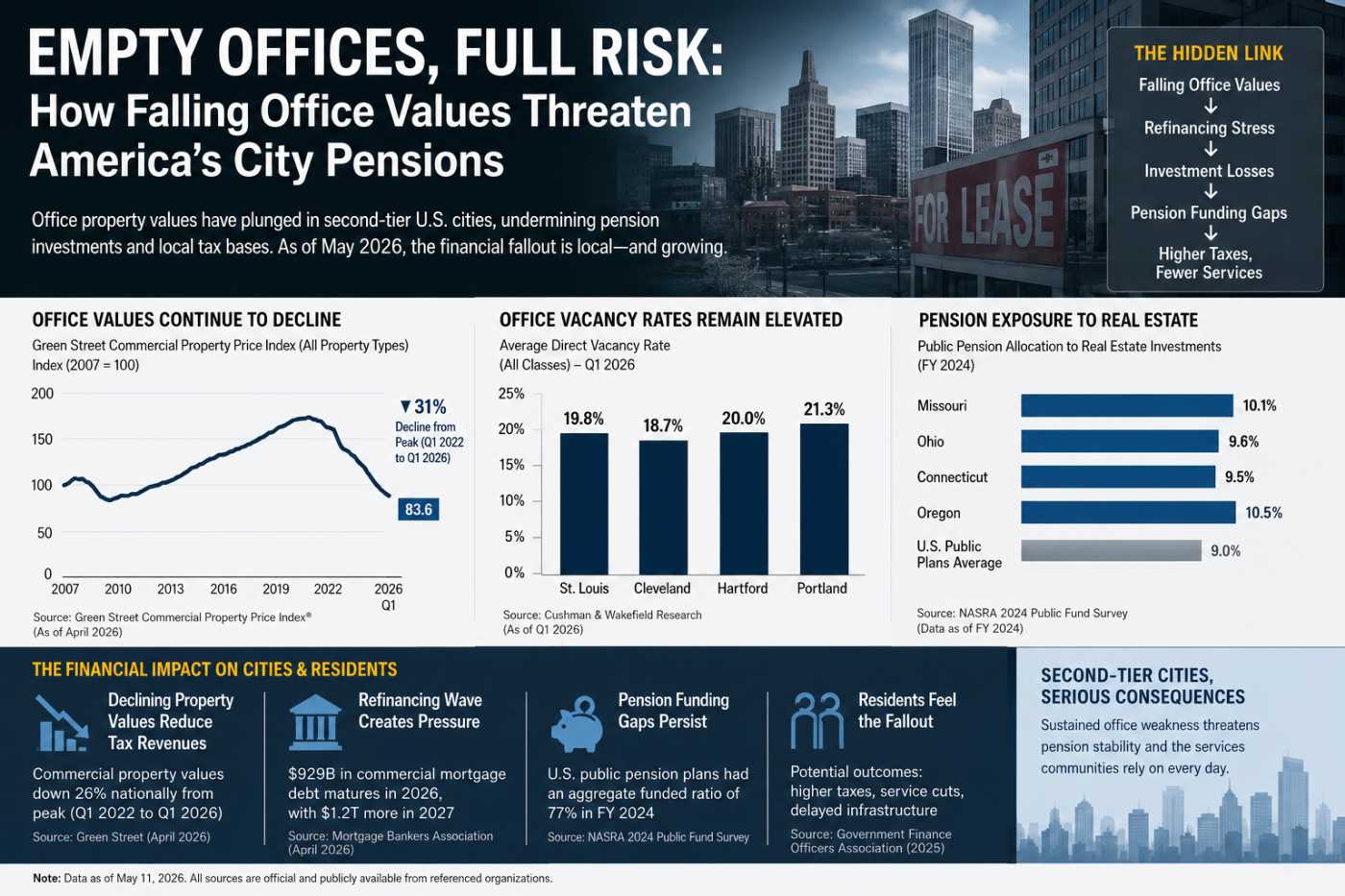

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

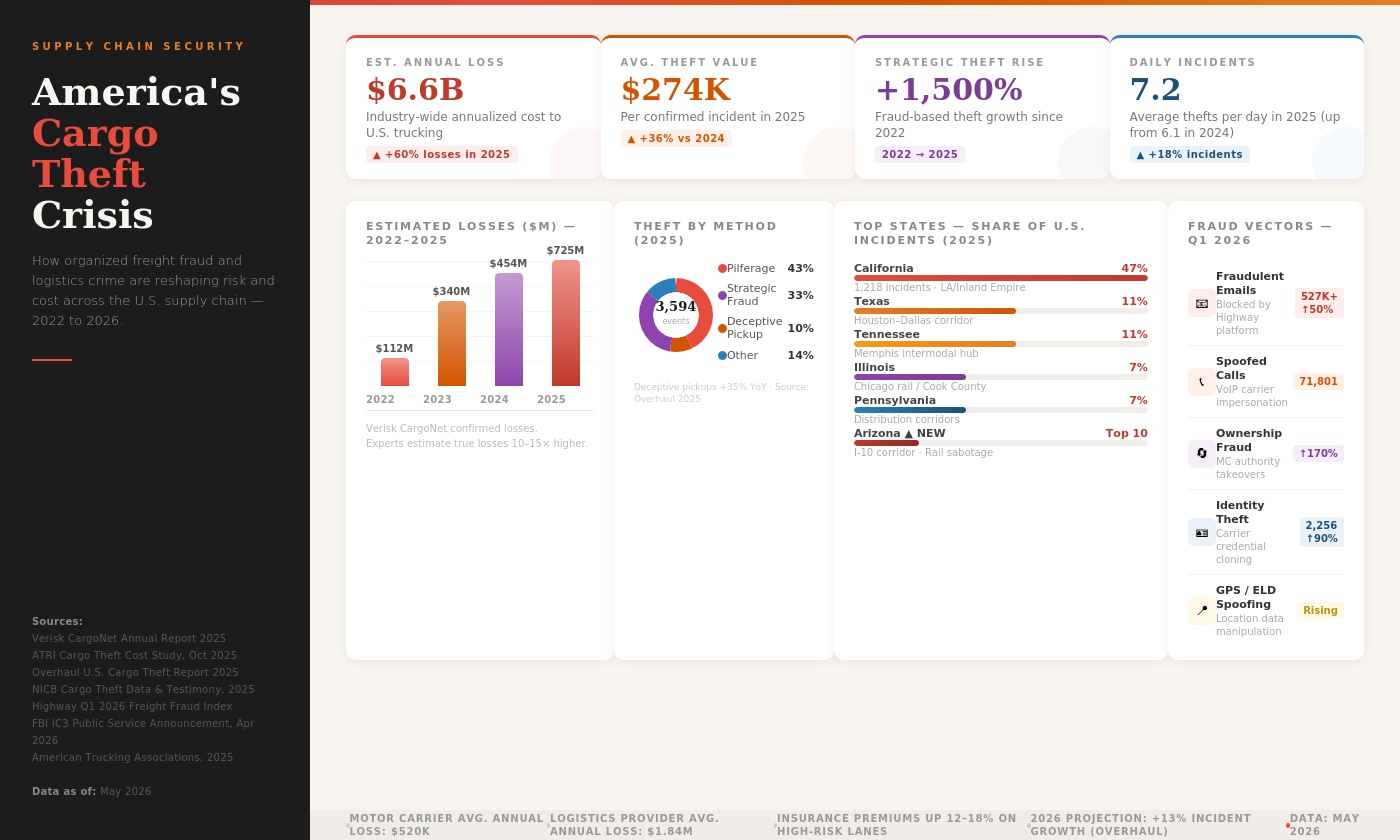

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

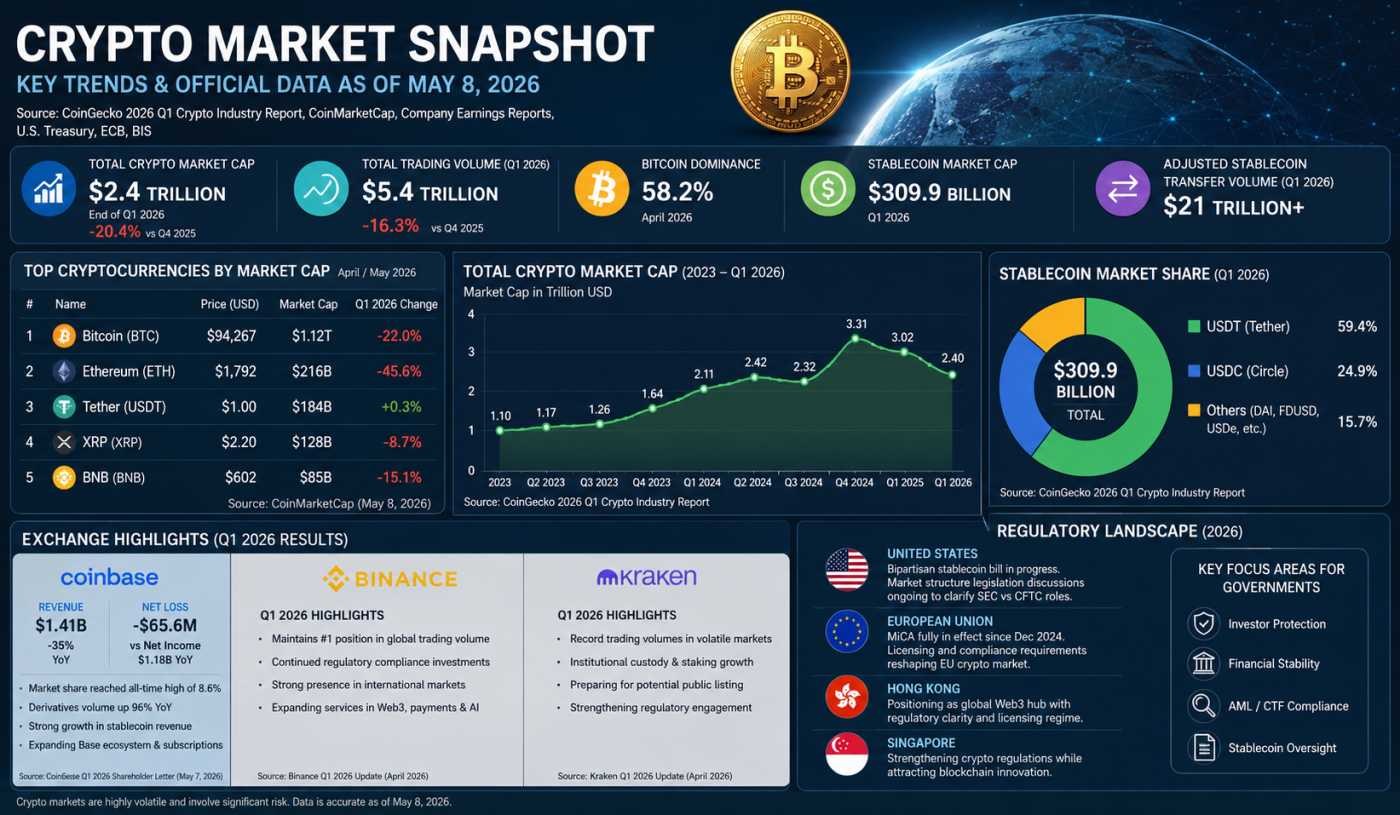

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

When Flooding Pays: A New Financial Bet

The Quiet Emergence of a Market That Profits From Decline

In the fragmented landscape of structured finance, a new class of instruments has begun to circulate quietly among hedge funds and specialty insurers: so-called “reverse green bonds.” Unlike traditional green bonds, which tie investor returns to environmental improvements, these securities invert the premise. They reward deterioration. Specifically, they are structured so that payouts increase when environmental indicators air quality, flood risk, or heat exposure worsen.

While still niche, their emergence coincides with a broader recalibration of climate risk pricing in U.S. housing markets. Nowhere is this more visible or more unsettling than in a controversial 2024 issuance targeting neighborhoods in Harris County, Texas. There, a hedge fund structured a series of credit-linked notes whose performance is tied directly to localized environmental stressors. The implications ripple far beyond bond desks, reaching into insurance premiums, rental markets, and the daily lives of residents.

The Mechanics of ‘Reverse Green Bonds’

At their core, these instruments are a variant of credit-linked notes (CLNs), a structure that allows investors to take on specific risks in exchange for higher yields. Traditionally, CLNs reference corporate credit events defaults, downgrades, or restructuring. In the Harris County issuance, however, the “credit event” is environmental degradation.

The notes are tied to a basket of environmental triggers derived from publicly available datasets, including floodplain expansion metrics maintained by county authorities and air quality indices reported by federal monitoring systems. If predefined thresholds are breached such as a measurable increase in flood-prone acreage or sustained deterioration in particulate matter levels the notes deliver enhanced payouts to investors.

According to disclosures in filings reviewed by analysts at the Securities and Exchange Commission (SEC), the structure includes three tiers of triggers. The first tier, labeled “soft deterioration,” activates when annual flood risk scores increase by more than 5%. The second tier, “acute stress,” is tied to extreme weather events and insurance claim surges. The third tier rare but lucrative activates under conditions of severe environmental decline, such as consecutive years of worsening flood maps combined with measurable air quality degradation.

The coupon rates on these notes range from 9.5% to as high as 18%, depending on trigger activation. For comparison, traditional municipal bonds in the same region yield between 3% and 5%. The spread reflects both the novelty of the structure and the moral hazard embedded within it.

A Targeted Geography: Harris County’s Vulnerable Zones

The 2024 issuance specifically references census tracts in eastern and northeastern Harris County, areas that have experienced repeated flooding events over the past decade. Data compiled from county property records indicates that more than 60% of the targeted tracts are majority Latino, with median household incomes significantly below the county average.

These neighborhoods have long been at the intersection of environmental vulnerability and economic precarity. Following Hurricane Harvey in 2017, floodplain maps were revised to include thousands of additional properties. By 2023, internal county assessments estimated that nearly 1 in 4 homes in these tracts faced elevated flood risk.

What makes the bond structure particularly controversial is its reliance on precisely these metrics. As floodplain designations expand or as mitigation efforts stall the probability of trigger activation increases, directly benefiting investors.

Property-level data underscores the stakes. Between 2020 and 2025, average homeowners’ insurance premiums in the targeted tracts rose by approximately 47%, according to filings compiled by the Texas Department of Insurance. In some zip codes, premiums doubled, driven largely by updated flood risk models. Renters, meanwhile, have absorbed indirect costs through rising rents, as landlords pass along higher insurance expenses.

Public Comments Reveal Unease

The SEC filing for the issuance drew an unusual volume of public comments, many of which highlighted concerns about the ethical implications of the structure. Among them were submissions from local advocacy groups, housing researchers, and even individual residents.

One comment, attributed to a coalition of Houston-based non-profits, argued that the bonds “create a financial incentive structure that is fundamentally misaligned with public policy goals.” The authors noted that while investors stand to gain from worsening conditions, local governments are simultaneously struggling to fund flood control and environmental remediation projects.

Another submission, from a researcher affiliated with a university housing lab, pointed out that the bonds effectively “externalize climate risk onto populations least equipped to manage it.” The comment cited data showing that renters in the targeted tracts spend an average of 38% of their income on housing, leaving little room to absorb additional cost pressures.

Even within financial circles, the structure has prompted debate. Analysts at a major ratings agency described the instrument as “innovative but potentially destabilizing,” noting that it introduces feedback loops between environmental outcomes and financial incentives.

The Perverse Incentive Problem

The most troubling aspect of reverse green bonds lies not in their complexity but in their incentives. By design, they reward deterioration. This creates a scenario in which investors directly or indirectly benefit from the failure of environmental mitigation efforts.

While there is no evidence that bondholders have actively lobbied against flood control projects, the potential for such behavior is difficult to ignore. Infrastructure decisions in Harris County are often subject to political negotiation, budget constraints, and public input. In such an environment, even subtle shifts in advocacy can influence outcomes.

Consider the economics: a large-scale flood mitigation project that successfully reduces risk could suppress trigger activation, lowering returns for investors. Conversely, delays or underfunding could increase the likelihood of payouts. The asymmetry is stark.

This dynamic is particularly concerning given the scale of investment. Market participants estimate that the 2024 issuance totaled approximately $600 million, with additional tranches planned. While small relative to the broader municipal bond market, it is large enough to attract attention and potentially influence behavior.

Insurance Markets as the Transmission Mechanism

The effects of these bonds are not confined to financial statements. They intersect directly with the insurance market, which serves as the primary channel through which environmental risk is priced into housing costs.

In recent years, insurers have recalibrated their models to account for increased climate volatility. In Harris County, this has translated into higher premiums, reduced coverage options, and, in some cases, market exits. Data from the Texas Department of Insurance shows that the number of active homeowners’ insurance providers in high-risk zip codes declined by nearly 15% between 2021 and 2025.

Reverse green bonds amplify these dynamics by effectively monetizing the same risk factors that insurers use to set premiums. As environmental indicators worsen, insurers raise rates and bondholders receive higher payouts. The result is a dual burden on residents: higher housing costs and diminished environmental quality.

For renters, the impact is indirect but no less significant. Analysis of rental listings across eastern Harris County shows that average rents increased by 22% between 2022 and 2025, outpacing wage growth. Landlords cite insurance costs as a primary driver, alongside property maintenance expenses linked to flooding.

Data as Destiny

One of the defining features of these bonds is their reliance on granular, publicly available data. Flood maps, air quality indices, and insurance claims data are all incorporated into the trigger framework. This creates a veneer of objectivity an impression that the bonds simply reflect underlying realities.

But data is not neutral. It is shaped by measurement choices, reporting practices, and policy decisions. For example, the expansion of floodplain maps can be influenced by updated modeling techniques or regulatory changes. Similarly, air quality measurements depend on the placement and calibration of monitoring stations.

In this context, the bond structure effectively transforms data points into financial levers. Small changes in measurement can have outsized effects on payouts. This raises questions about transparency, accountability, and the potential for manipulation intentional or otherwise.

The Transfer of Risk From Wall Street to Main Street

Perhaps the most consequential aspect of reverse green bonds is the way they redistribute risk. Traditionally, financial markets have been mechanisms for dispersing risk among investors. In this case, however, the risk is not merely shared it is shifted.

Investors receive high yields in exchange for exposure to environmental deterioration. But the underlying consequences of that deterioration flood damage, health impacts, rising costs are borne by residents. In effect, the bonds allow investors to profit from risks that others must live with.

This dynamic is particularly acute in renter-heavy neighborhoods. Unlike homeowners, renters have limited control over property-level mitigation measures and are often excluded from insurance decisions. Yet they face the same environmental risks and absorb cost increases through rent.

Data from local housing authorities indicates that more than 55% of households in the targeted tracts are renters. For these residents, the bond market’s bet against environmental improvement translates into higher living costs and increased vulnerability.

A Market Still in Its Infancy

Despite their unsettling implications, reverse green bonds remain a relatively small segment of the market. Analysts estimate that total issuance across the United States is under $2 billion as of early 2026. However, growth is accelerating, driven by investor appetite for high-yield instruments and the increasing availability of environmental data.

Several hedge funds and specialty insurers are reportedly exploring similar structures in other regions, including coastal areas in Florida and wildfire-prone zones in California. Each iteration introduces new variations different triggers, alternative data sources, and more complex payout mechanisms.

The trajectory suggests that what began as a niche experiment could evolve into a broader asset class. If so, the questions raised by the Harris County issuance will become increasingly relevant not just for investors, but for policymakers, residents, and anyone navigating the changing landscape of climate risk.

An Uncomfortable Reflection

For residents of Houston and its surrounding suburbs, the rise of reverse green bonds adds a new layer of complexity to an already challenging environment. Insurance premiums are rising. Flood risks are evolving. And now, financial markets are beginning to price and profit from these dynamics in ways that are not always visible.

The unsettling reality is that the bond market is no longer just a passive observer of environmental change. It is becoming an active participant, with incentives that do not always align with community well-being. In Harris County, that participation has taken a particularly stark form: a financial instrument that pays more when conditions get worse.

Whether this model remains a niche curiosity or expands into a defining feature of climate finance will depend on a range of factors regulatory responses, market demand, and public scrutiny among them. For now, it stands as a stark illustration of how financial innovation can intersect with environmental vulnerability in ways that challenge conventional notions of risk, responsibility, and justice.

If you have enjoyed reading, spread the word:

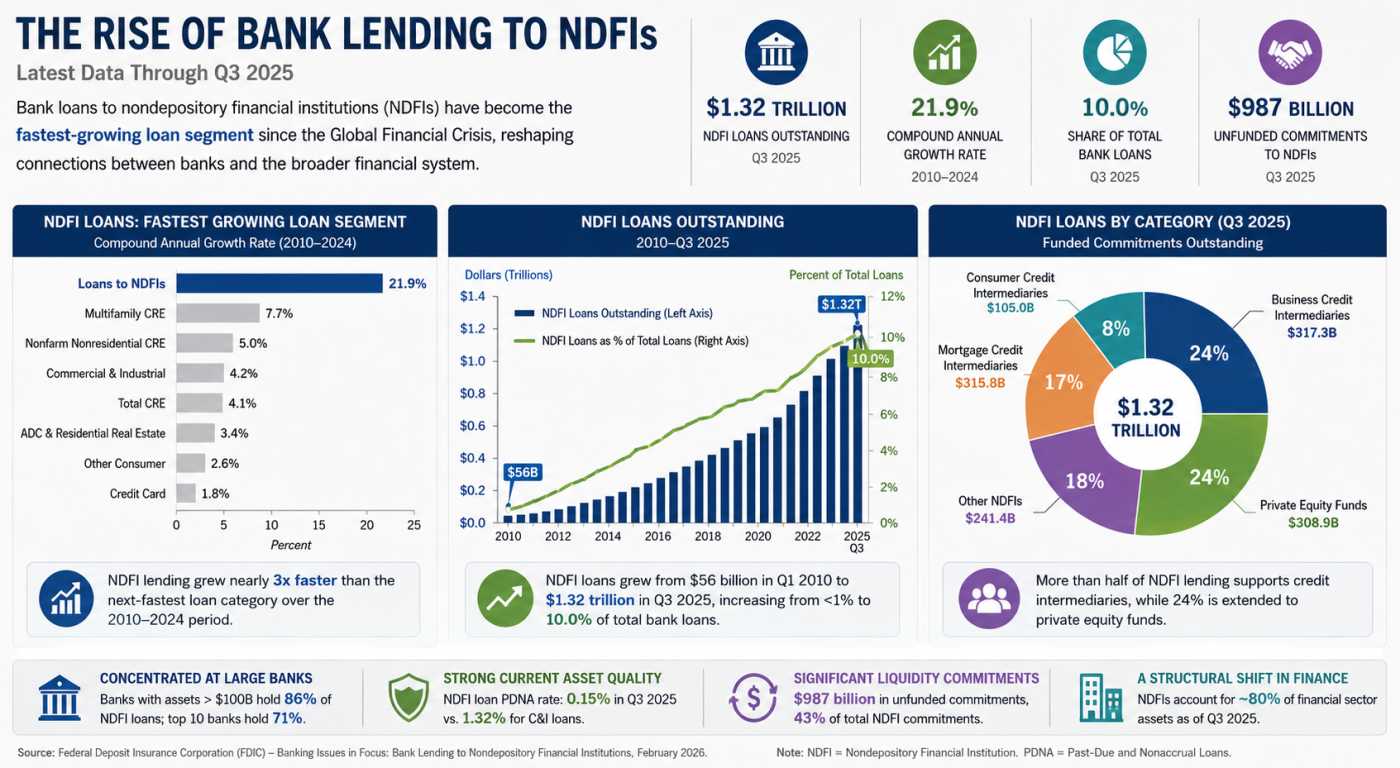

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun

The Repair Economy Boom in Rural America

Debt, Deficits & Disaster: The Bond Market Crisis