Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

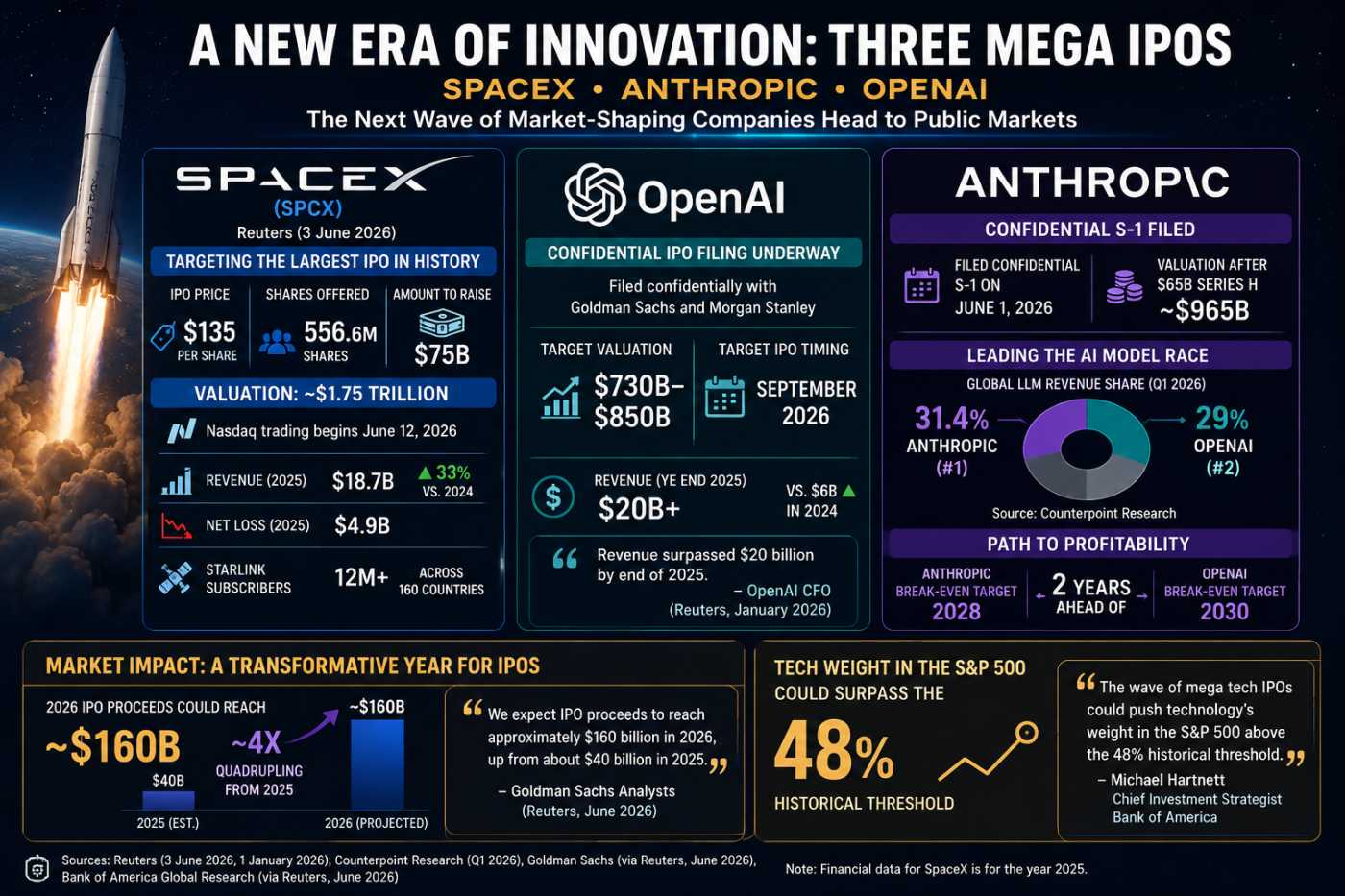

The Biggest IPO Year Ever: Can Markets Absorb It?

The Jobs Report That Crashed the Rally

The Fed Study Revealing Tomorrow's Investment Themes

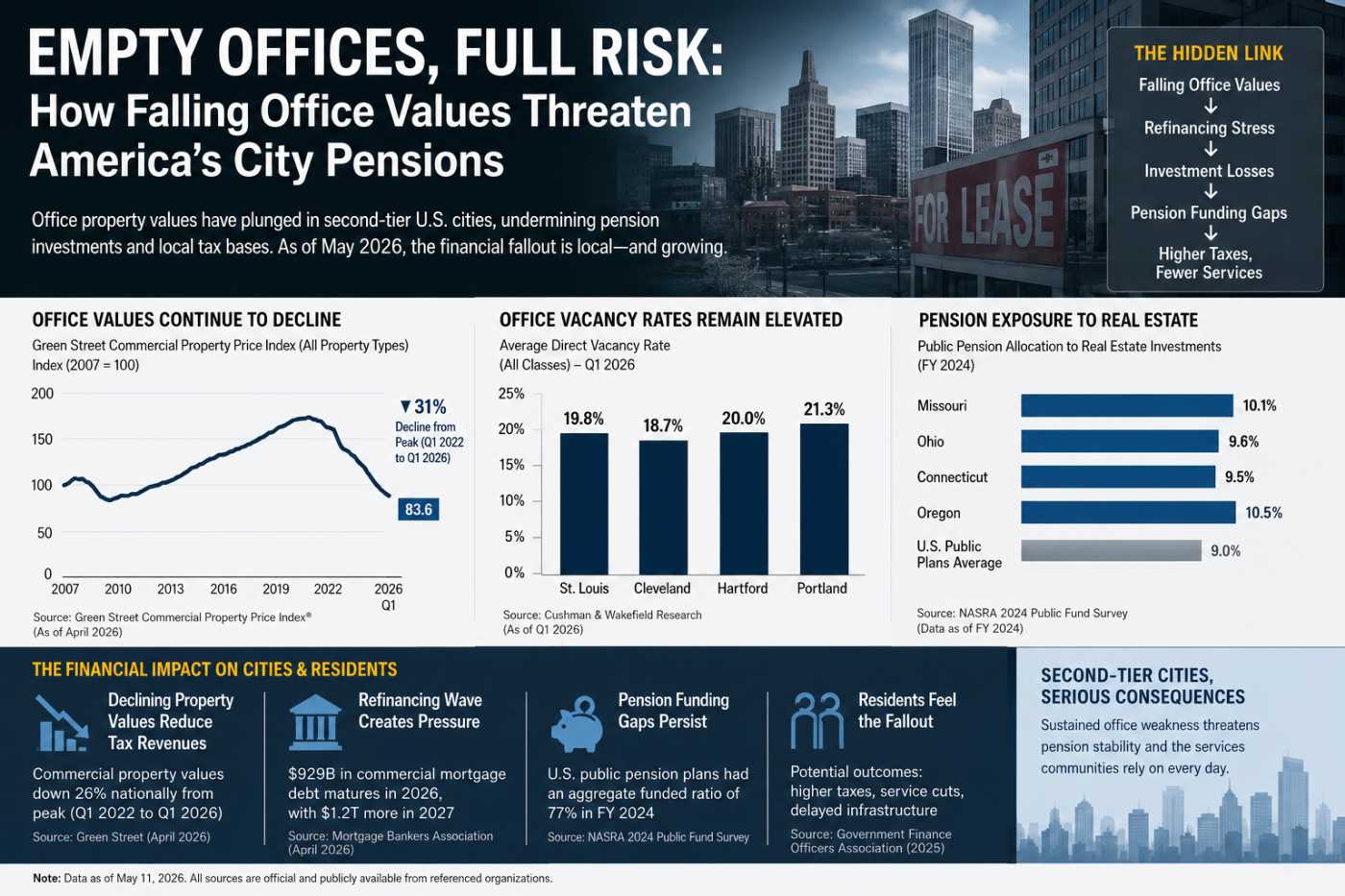

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

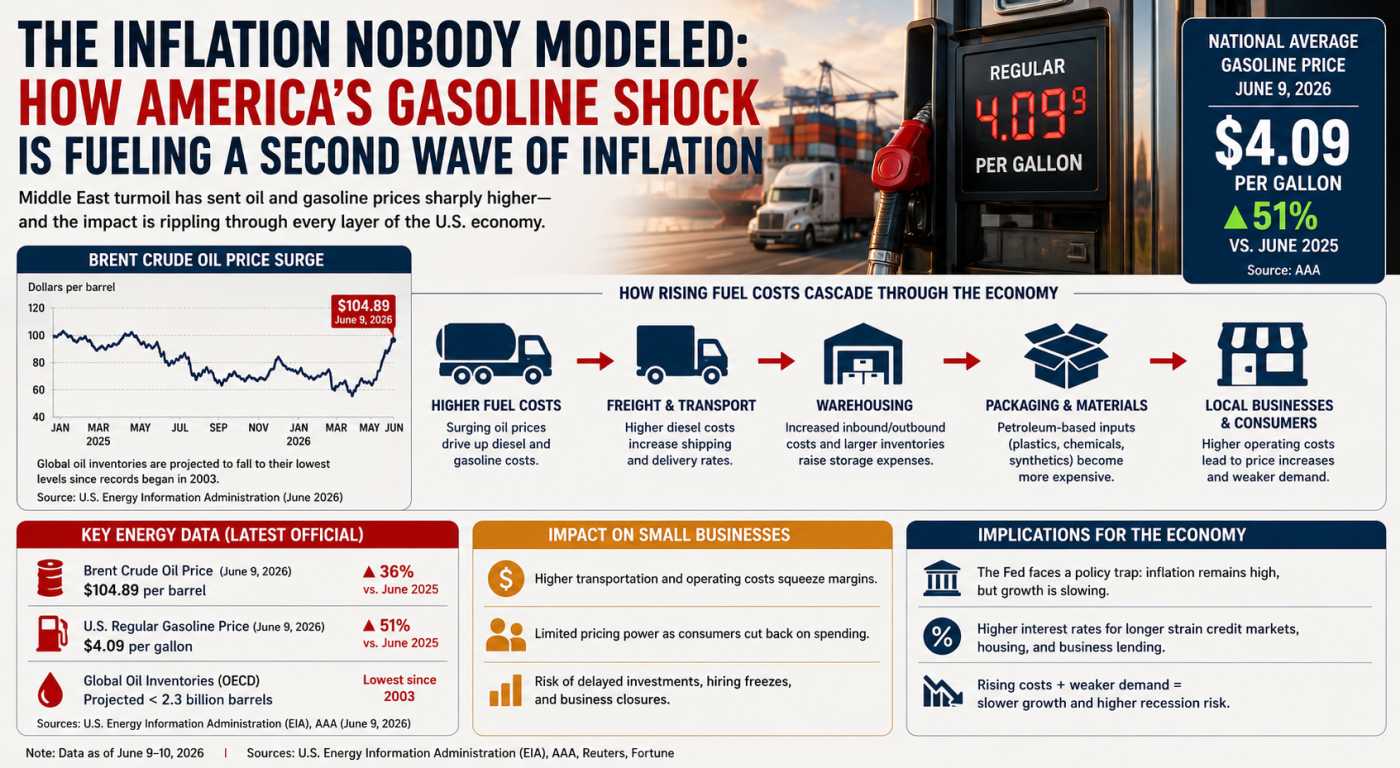

The Inflation Wave the Fed Can't Navigate

For much of early 2026, the dominant narrative surrounding the U.S. economy was that the Federal Reserve had achieved something economists rarely witness: a soft landing. Inflation had moderated from its post-pandemic peaks, unemployment remained relatively low, and financial markets spent months debating not whether interest rates would be cut, but when.

That narrative is now facing its most serious challenge of the year.

As of June 2026, a renewed energy shock tied to escalating conflict in the Middle East has sent oil and gasoline prices sharply higher, injecting a fresh source of inflation into an economy that was already struggling to return to the Federal Reserve's 2% target. What makes this inflationary surge particularly dangerous is that its effects extend far beyond the gas pump. The increase in fuel costs is beginning to ripple through freight transportation, packaging production, warehousing operations, and thousands of local service businesses, creating a second wave of price pressures that conventional monetary policy may be poorly equipped to contain.

The result is a growing risk that the United States could find itself trapped between weakening consumer purchasing power and persistent supply-side inflation an uncomfortable position that threatens small businesses, credit markets, and economic growth simultaneously.

An Energy Shock Arrives at the Worst Possible Moment

The immediate catalyst is the deterioration of energy markets following disruptions to Middle Eastern oil production and shipping routes. According to the U.S. Energy Information Administration (EIA), global oil inventories are now projected to fall to their lowest levels since records began in 2003, while Brent crude prices are expected to average approximately $105 per barrel during June and July 2026.

In its June outlook, the EIA warned that global oil stockpiles are declining rapidly due to major supply disruptions and reduced flows through the Strait of Hormuz. The agency estimates that OECD petroleum inventories could fall below 2.3 billion barrels by year-end, a historically tight level for global energy markets. Reuters reported on June 9 that the EIA expects Brent crude to average around $105 per barrel during the summer months. This represents a significant increase from levels that prevailed during much of 2025.

The impact on consumers has been immediate. National average gasoline prices have climbed above $4 per gallon, according to multiple market trackers. Rising fuel costs are once again becoming one of the most visible inflation indicators for households, affecting commuting expenses, travel budgets, and discretionary spending decisions.

Yet focusing solely on gasoline prices understates the broader economic significance of the shock.

The Inflation Multiplier Few Are Discussing

Most public discussions about energy inflation focus on drivers filling their tanks. Historically, however, fuel inflation becomes economically dangerous when it spreads through supply chains.

Modern commerce is extraordinarily energy-intensive. Every product sold in the United States requires transportation, storage, handling, packaging, and distribution. When diesel prices rise, trucking companies face higher operating costs. When trucking costs rise, warehouses experience higher inbound and outbound logistics expenses. When warehousing costs rise, retailers and manufacturers eventually face pressure to increase prices.

This transmission mechanism often operates with a lag, meaning the inflationary effects of today's fuel shock may continue appearing in economic data for months even if oil prices stabilize.

The freight sector is particularly vulnerable. Long-haul trucking remains the backbone of U.S. domestic commerce, accounting for the majority of overland freight movement. Fuel frequently represents one of the largest variable expenses for trucking operators. Many carriers use fuel surcharges to pass costs to customers, but those surcharges ultimately appear in the prices paid by businesses and consumers.

The effect extends further into packaging and manufacturing. Plastics, synthetic materials, industrial chemicals, and numerous packaging products derive directly or indirectly from petroleum feedstocks. Rising crude prices therefore influence not only transportation costs but also the cost structure of physical goods production.

Warehousing operators face a separate challenge. Higher transportation costs often coincide with increased inventory management expenses. Companies attempting to avoid supply disruptions may choose to hold larger inventories, increasing storage requirements and financing costs at precisely the moment interest rates remain elevated.

The combination creates what economists sometimes describe as a cost-push inflation cycle a form of inflation driven by rising production costs rather than excessive consumer demand.

Why the Federal Reserve Faces a Difficult Trap

Ordinarily, the Federal Reserve responds to inflation by tightening monetary conditions. Higher interest rates reduce borrowing, slow demand, and eventually moderate price pressures.

The current situation is more complicated because the source of inflation is increasingly external to domestic demand.

When inflation originates from energy supply disruptions, higher interest rates cannot produce more oil, reopen shipping routes, or restore lost production capacity. Monetary policy can suppress demand, but it cannot directly address supply shortages.

That distinction matters because the broader economy is already showing signs of sensitivity to higher borrowing costs. Mortgage rates remain elevated, business lending conditions have tightened, and interest-sensitive sectors such as commercial real estate continue to face refinancing pressures.

At the same time, inflation has not returned convincingly to target. According to a Reuters survey published on June 9, 2026, economists increasingly expect the Federal Reserve to keep interest rates unchanged throughout the remainder of the year because inflation remains stubbornly above desired levels and energy-driven price pressures are intensifying. The Reuters poll found a growing consensus that expected rate cuts may no longer materialize in 2026.

The labor market is complicating matters further. The U.S. economy added 172,000 jobs in May, significantly exceeding expectations. Strong employment growth typically signals economic resilience, but in the current environment it also reduces the Federal Reserve's flexibility to ease policy. Strong labor data increases concerns that inflation could remain persistent.

When Strong Economic Data Becomes Bad News

One of the most unusual developments of recent weeks has been financial markets reacting negatively to positive economic news.

Following the stronger-than-expected May employment report, Treasury yields climbed while major equity indexes declined. Investors interpreted the data as reducing the likelihood of future rate cuts.

As Fortune noted in its analysis of the May jobs report, the employment figures were substantially stronger than economists anticipated, raising concerns that hopes for monetary easing may have been premature. The publication observed that stronger labor market conditions could reinforce the higher-for-longer interest-rate narrative just as energy-driven inflation is re-emerging.

This dynamic illustrates the Federal Reserve's dilemma. Economic weakness would justify rate cuts but could threaten employment and growth. Economic strength supports jobs but risks prolonging inflation. An energy shock layered on top of this equation makes policy calibration substantially more difficult.

In effect, financial markets are beginning to price a scenario in which inflation remains elevated even as economic momentum slows.

The Small Business Squeeze

Large corporations often possess tools that help them manage energy shocks. They may hedge fuel costs, negotiate long-term contracts, diversify suppliers, or absorb temporary margin pressures.

Small businesses typically enjoy far fewer protections.

Independent contractors, local delivery operators, restaurants, repair services, construction firms, landscaping companies, and regional retailers all face direct exposure to fuel costs. For many, transportation is not merely a cost center but a core operational requirement.

Unlike publicly traded corporations, small businesses frequently lack pricing power. They cannot always pass rising costs to customers without risking demand destruction. As household budgets become strained by higher gasoline and utility expenses, consumers often reduce discretionary purchases, creating a second challenge for local businesses.

The result is a margin squeeze from both directions. Costs rise while customers become more price-sensitive.

This phenomenon can be especially damaging because small businesses account for a substantial share of U.S. employment and local economic activity. A prolonged period of cost-push inflation could therefore weaken hiring intentions even if national employment statistics initially remain healthy.

Credit Markets Are Sending Warning Signals

The inflation implications extend beyond consumers and businesses into financial markets.

If investors conclude that inflation will remain elevated for longer, bond yields may continue rising. Higher yields increase borrowing costs throughout the economy, affecting mortgages, auto loans, corporate debt issuance, and commercial real estate financing.

Recent movements already reflect these concerns. Treasury yields have risen as investors reassess the likelihood of Federal Reserve easing. Mortgage rates have also moved higher amid renewed inflation fears.

For heavily indebted sectors, this matters enormously. Commercial real estate borrowers facing refinancing deadlines may encounter higher costs than expected. Corporate borrowers could postpone investment plans. Consumers may become more cautious about major purchases.

Credit markets are therefore acting as a transmission mechanism through which an energy shock can influence broader economic activity.

The Risk to the Soft-Landing Narrative

The defining assumption behind the soft-landing thesis was that inflation would continue gradually declining without triggering a significant recession.

The current energy shock challenges that assumption because it introduces a source of inflation largely unrelated to domestic demand conditions. Instead of fading naturally as consumer spending cools, energy-driven inflation can spread through supply chains and persist even when economic growth slows.

Perhaps the most important underreported risk is not the immediate increase in gasoline prices but the delayed inflation embedded in freight contracts, packaging costs, inventory management, warehousing operations, and local service businesses. These secondary effects often take longer to appear and can remain in place long after the initial commodity shock.

The Federal Reserve may therefore face a situation where inflation remains too high to justify rate cuts while economic activity weakens under the combined weight of elevated borrowing costs and declining consumer purchasing power.

That combination does not necessarily imply a recession. However, it does suggest that the path toward a smooth soft landing has become considerably narrower than many investors believed only a few months ago. The gasoline shock emerging in June 2026 is not merely an energy story. It is increasingly becoming a story about the hidden inflation pipeline running through the entire American economy.

If you have enjoyed reading, spread the word:

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

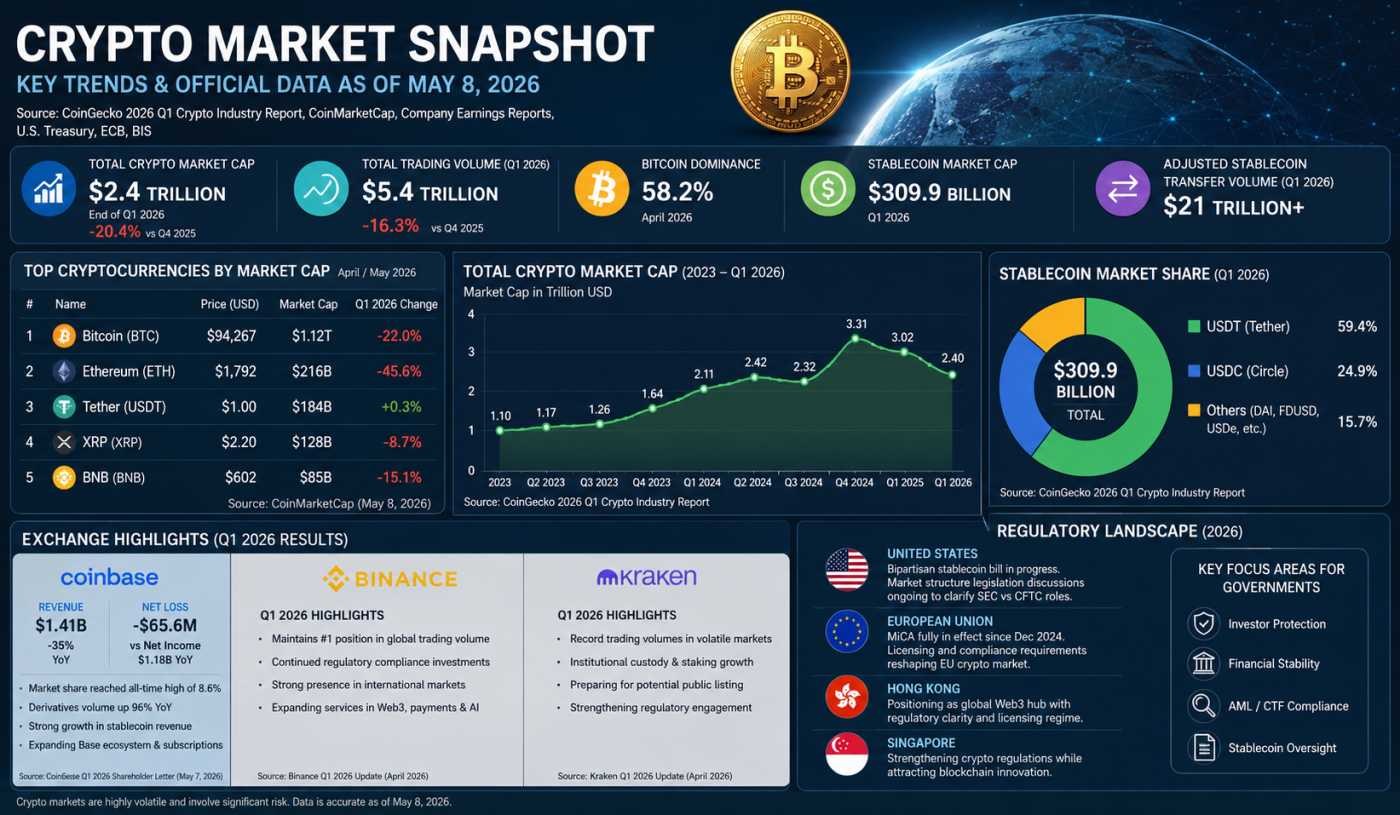

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

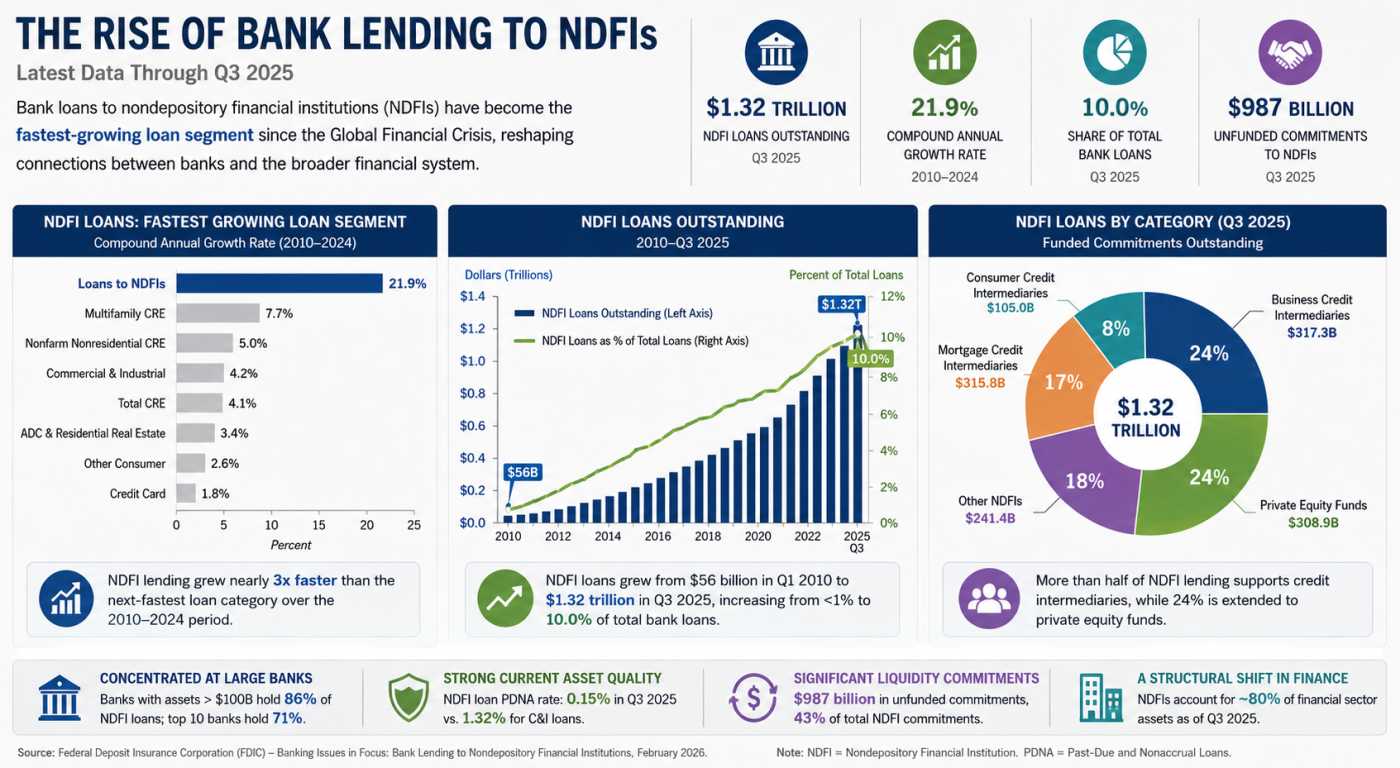

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected