Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

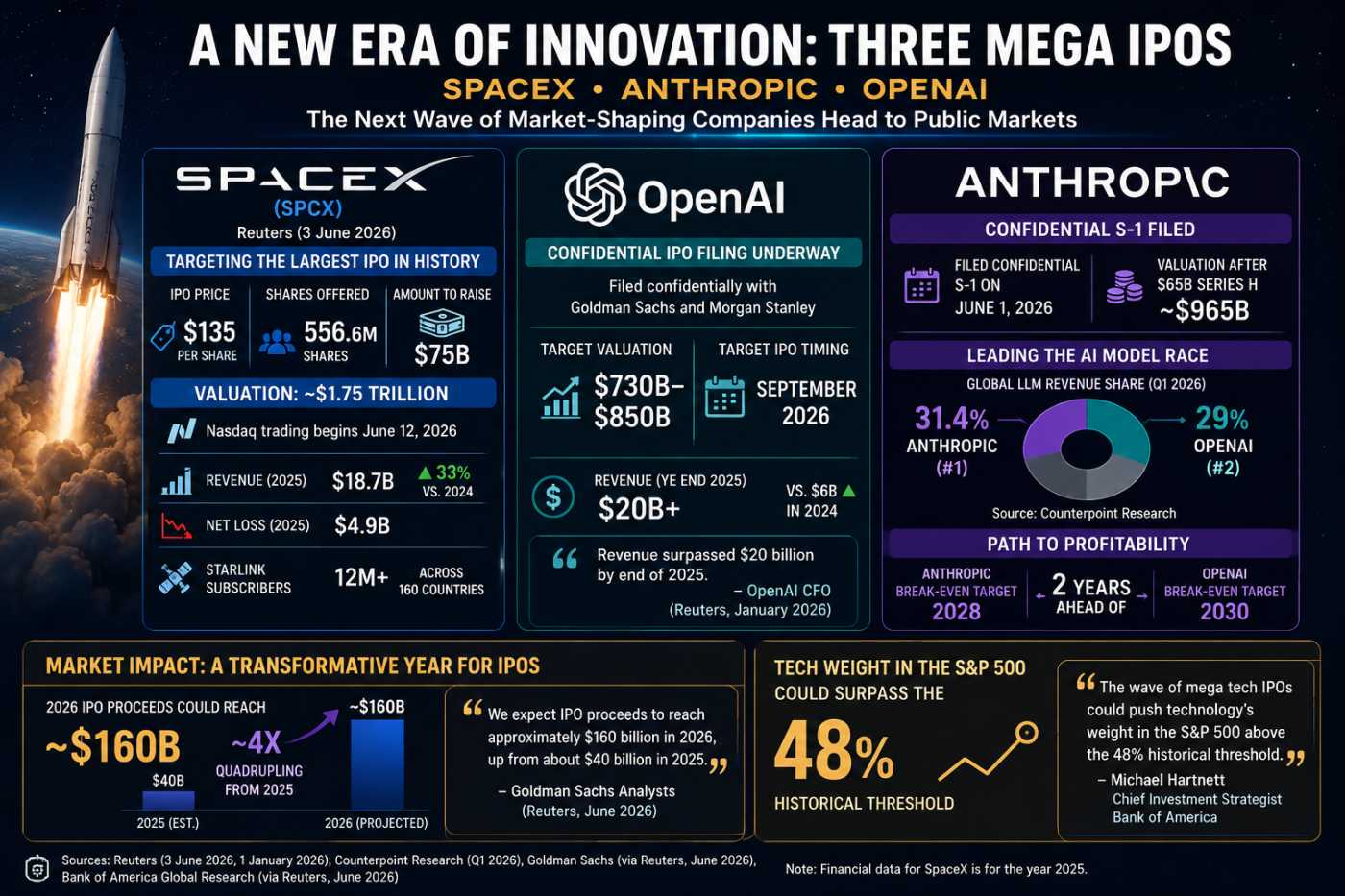

How SpaceX Gave Main Street a Seat at the IPO

How Workers Became Capitalists

The Inflation Wave the Fed Can't Navigate

The Biggest IPO Year Ever: Can Markets Absorb It?

The Jobs Report That Crashed the Rally

SpaceX IPO Spawned a New Speculation Machine

The Fastest Financial Product Launch in IPO History?

Wall Street has always been adept at turning investor excitement into investable products. Yet even by modern standards, what happened after SpaceX's June 2026 IPO was extraordinary.

SpaceX completed the largest IPO in history, raising approximately $75 billion at an initial valuation approaching $1.75 trillion. Within days of the company's stock beginning public trading, investors were presented with something unprecedented: an entire ecosystem of leveraged exchange-traded funds designed to magnify SpaceX's daily price movements.

According to reporting by Axios, approximately eleven leveraged SpaceX ETFs began trading almost immediately after the IPO, offering investors 2x long, 2x short and other leveraged exposures to one of the world's newest publicly traded mega-cap companies. The speed of the rollout was remarkable not merely because of the number of products involved, but because many were approved, marketed and prepared before the market had even established a meaningful public trading history for the stock itself.

For decades, leveraged ETFs were largely associated with broad market indexes, commodities and established companies with deep trading histories. SpaceX represents a potentially important turning point. For perhaps the first time, an entire leveraged ETF ecosystem emerged before the underlying stock had completed even a single week as a public company.

The question is not whether investors should be allowed to trade these products. The more interesting question is whether Wall Street's race to monetize demand has created a new category of speculation-first investment products that arrive before genuine price discovery has occurred.

A Product Category Built Before the Market Existed

The most striking aspect of the SpaceX ETF launch wave was its timing.

Reuters reported in March 2026 that asset managers including T-Rex, Tuttle Capital and others were already filing for leveraged SpaceX ETFs before the company had completed its IPO process. In effect, product manufacturers were preparing leverage-based investment vehicles before public investors even had access to the stock itself.

This represented a significant departure from the traditional sequence of financial product development.

Historically, a company would go public, establish a trading history, develop institutional ownership patterns, become covered by analysts and eventually attract derivatives products. Only after markets had accumulated substantial information would more complex structures emerge.

SpaceX reversed that timeline.

As Reuters noted in March, firms sought to launch 2x leveraged SpaceX funds even before the IPO had taken place. By June, multiple issuers were competing simultaneously for market share. Products from ProShares, Direxion, Defiance, GraniteShares, Leverage Shares, Tradr and others were either launched or prepared for launch within days of the offering.

The result was a situation in which Wall Street appeared to have greater certainty about investor demand for leveraged products than about the appropriate valuation of the underlying company.

Price Discovery Was Barely Beginning

Price discovery is one of the most important yet least discussed functions of financial markets.

When a company first becomes public, investors gradually establish consensus regarding future earnings potential, competitive position, growth prospects and risk factors. Institutional investors build positions, hedge funds test assumptions, analysts publish research and markets slowly incorporate new information.

For most companies, this process takes months or years.

SpaceX had not completed that process when leveraged products arrived.

By June 16, 2026, the company had been publicly traded for only a handful of sessions. During that brief period, its market capitalization fluctuated by hundreds of billions of dollars. Reuters reported that SpaceX's options market generated more than 500,000 contracts of trading volume within the first hour of its debut, an unprecedented figure for a newly public company. The same report noted that the stock surged more than 25% during its first trading session and quickly exceeded a $2 trillion valuation. Reuters described the options debut as one of the most active ever recorded for a newly listed company.

Such activity reflects enthusiasm, but enthusiasm is not the same thing as price discovery.

When valuation swings of hundreds of billions of dollars occur within days, markets are still gathering information rather than expressing settled judgment.

Introducing leveraged products during this phase effectively allows investors to amplify uncertainty itself.

The Free Float Problem Nobody Is Discussing

One underappreciated issue involves share availability.

Following the IPO, only a relatively small percentage of SpaceX shares became freely tradable. Reuters reported that roughly 7% of total shares were expected to be available in the public float initially.

This matters because price discovery functions best when a large and diverse set of investors can transact freely.

Limited float conditions can amplify volatility. Small changes in demand can produce disproportionately large changes in price. This dynamic is particularly important for a company with an initial valuation approaching $2 trillion.

When leveraged ETFs enter the picture, they often rely on swaps, derivatives and daily rebalancing mechanisms that react to underlying price movements.

In a stock with limited float and incomplete institutional ownership development, those flows can become more influential than they would be in a mature company.

The irony is striking. At the exact moment when markets are attempting to determine a fair valuation, leveraged products introduce additional trading flows that are unrelated to fundamental analysis.

From Investing Product to Trading Product

The SpaceX ETF launch wave also highlights a broader transformation occurring within the ETF industry.

For much of its history, the ETF sector marketed itself as a democratizing force. ETFs reduced costs, increased diversification and simplified long-term investing.

Many of the new SpaceX products pursue a different objective entirely.

They are explicitly designed for short-term trading.

Investopedia noted that the new leveraged SpaceX ETFs seek to deliver approximately twice the daily return of the stock through derivatives and daily rebalancing mechanisms. Because returns are reset daily, long-term performance can diverge substantially from the expected multiple due to volatility decay and compounding effects. Investopedia emphasized that these products are generally intended for short-term tactical exposure rather than long-term ownership.

That distinction is important.

The fundamental purpose of investing is capital allocation. The fundamental purpose of a leveraged single-stock ETF is amplified exposure to price movement.

Those objectives overlap less than many investors realize.

In the case of SpaceX, leveraged products arrived before many investors had even finished evaluating the company's first public filings.

The Rise of Speculation-First Product Design

SpaceX may represent the clearest example yet of a broader industry trend.

Increasingly, ETF issuers appear to be designing products around investor excitement rather than investor needs.

The evidence can be seen in the marketing language surrounding many recent launches.

Product providers compete to be first. They compete for ticker symbols. They compete for social media attention. They compete for trading volume.

The underlying investment thesis often becomes secondary.

Axios summarized the phenomenon bluntly when discussing the SpaceX ETF boom. The publication described the launch wave as an example of the increasingly aggressive risk-taking culture that has spread through modern financial markets. In its coverage, Axios observed that leveraged ETFs tied to SpaceX were being prepared before the stock had even begun public trading. Axios characterized the development as an extreme illustration of a broader shift toward speculation-oriented financial products.

The significance extends beyond SpaceX itself.

If ETF issuers can successfully launch a dozen leveraged products around a company that has traded publicly for less than a week, there is little reason to believe future high-profile IPOs will be treated differently.

Anthropic, Stripe, Databricks and other anticipated listings may face similar product ecosystems almost immediately upon going public.

Institutional Ownership Patterns Had Not Yet Formed

Another overlooked issue involves ownership structure.

Large institutional investors play a critical role in price discovery. Pension funds, mutual funds, sovereign wealth funds and long-horizon asset managers often establish positions gradually and evaluate companies based on detailed research.

Their activity tends to stabilize markets because investment decisions are tied to long-term expectations rather than short-term price fluctuations.

During SpaceX's first week as a public company, many of these ownership patterns were still evolving.

Some institutions were restricted from purchasing until index inclusion occurred. Others were conducting post-IPO due diligence. Some were waiting for lock-up periods to expire.

Yet leveraged ETF activity was already fully operational.

This creates an unusual imbalance. Short-term speculative flows can become highly visible before long-term ownership structures have had time to emerge.

In effect, traders gain amplified exposure before investors have completed valuation analysis.

The Derivatives Market Is Becoming the Tail That Wags the Dog

The rapid emergence of SpaceX options trading further complicates the picture.

Reuters reported that SpaceX options generated record-setting volume almost immediately after launch. Dealers managing those options exposures must hedge continuously as prices move.

Leveraged ETF providers similarly rely on derivatives and hedging mechanisms to maintain target exposures.

The result is a growing ecosystem of financial products whose trading activity depends not on SpaceX's business performance but on SpaceX's stock volatility.

This distinction matters.

Price discovery traditionally involves investors evaluating information about revenue growth, margins, competition and management execution.

Derivative-driven trading often responds primarily to price itself.

As more products are layered onto a newly public stock, a greater share of market activity becomes linked to volatility management rather than fundamental assessment.

The risk is not necessarily a market crash. The risk is that valuation signals become noisier precisely when investors are trying to determine what a company is actually worth.

A New Financial Template May Have Been Created

The most important development may be what SpaceX reveals about the future rather than the present.

The company is unique in scale, public interest and technological significance. Yet the ETF industry's response may establish a template that extends far beyond aerospace.

For decades, financial innovation typically followed market maturity. New products emerged after underlying markets became established.

The SpaceX experience suggests the order may now be reversing.

Financial engineering is increasingly arriving before market maturity rather than after it.

The launch of roughly a dozen leveraged SpaceX ETFs within days of the largest IPO in history signals a profound shift in how modern markets monetize investor enthusiasm. The traditional sequence of valuation, ownership formation and product expansion appears to be giving way to a new sequence: excitement first, leverage second and price discovery later.

Whether that evolution ultimately improves market efficiency remains uncertain. What is already clear is that SpaceX's IPO did more than create a new public company. It may have inaugurated an entirely new era in which leveraged speculation becomes a product category from day one rather than a consequence of market maturity.

If you have enjoyed reading, spread the word:

The Fed Study Revealing Tomorrow's Investment Themes

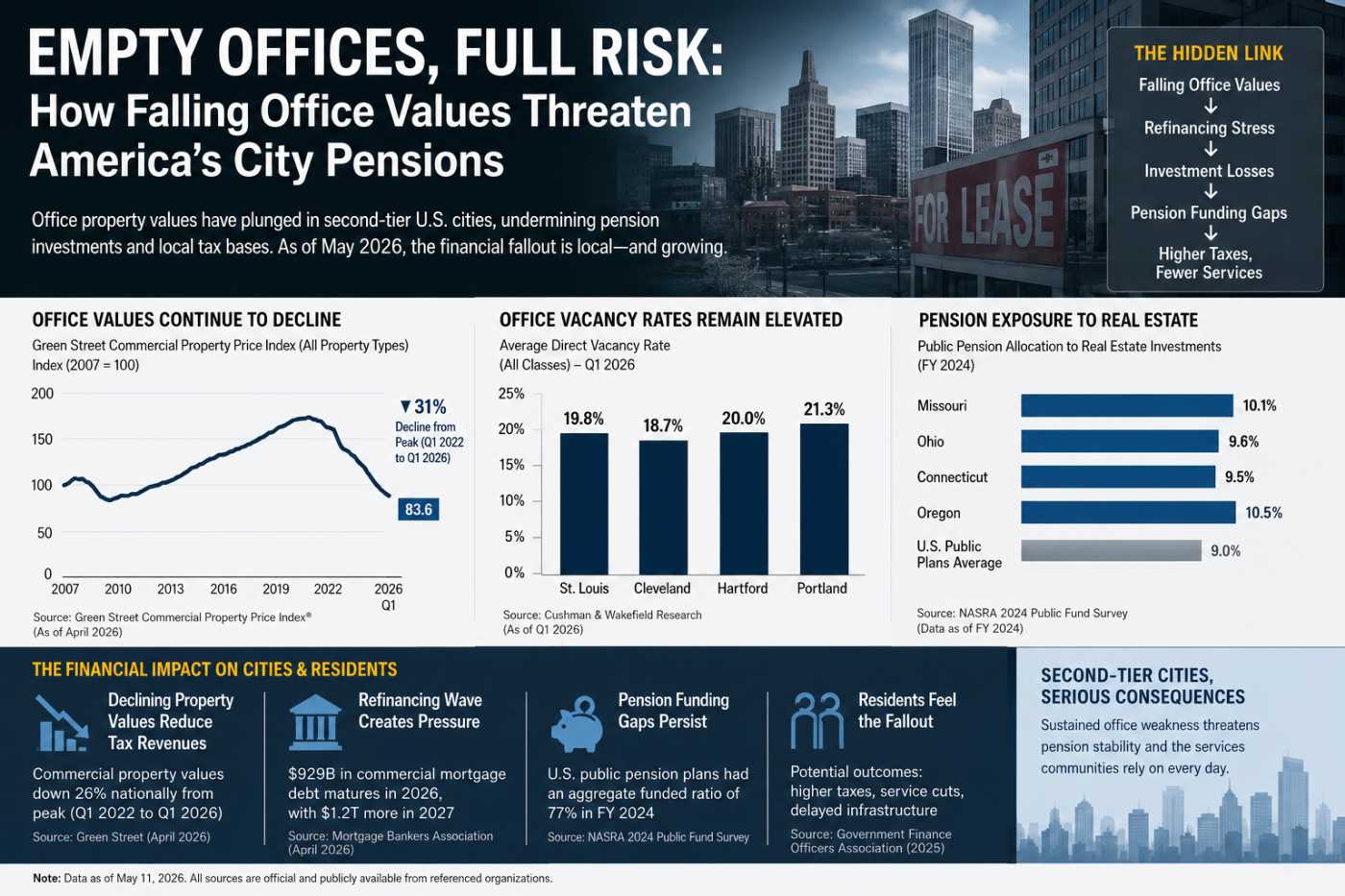

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

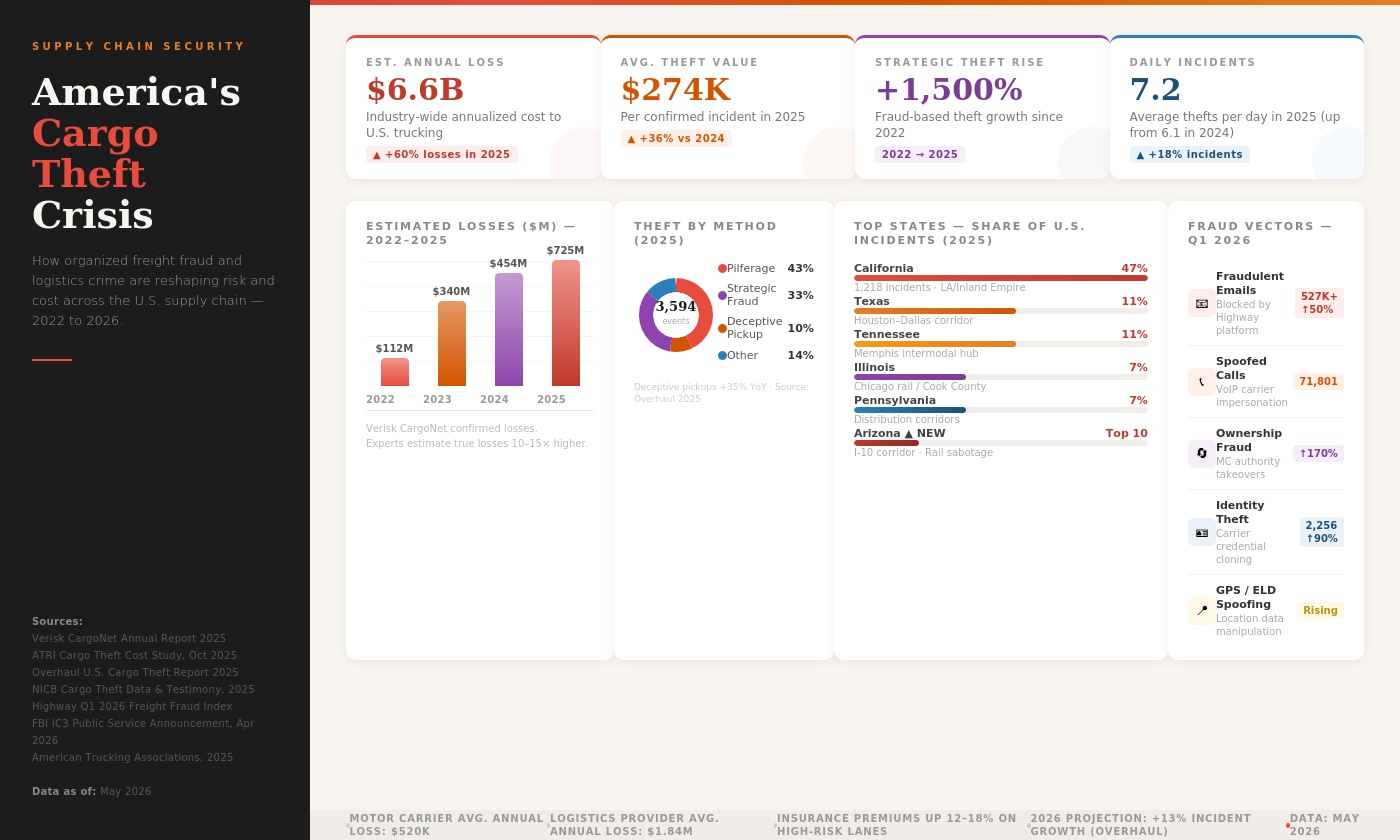

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?