Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

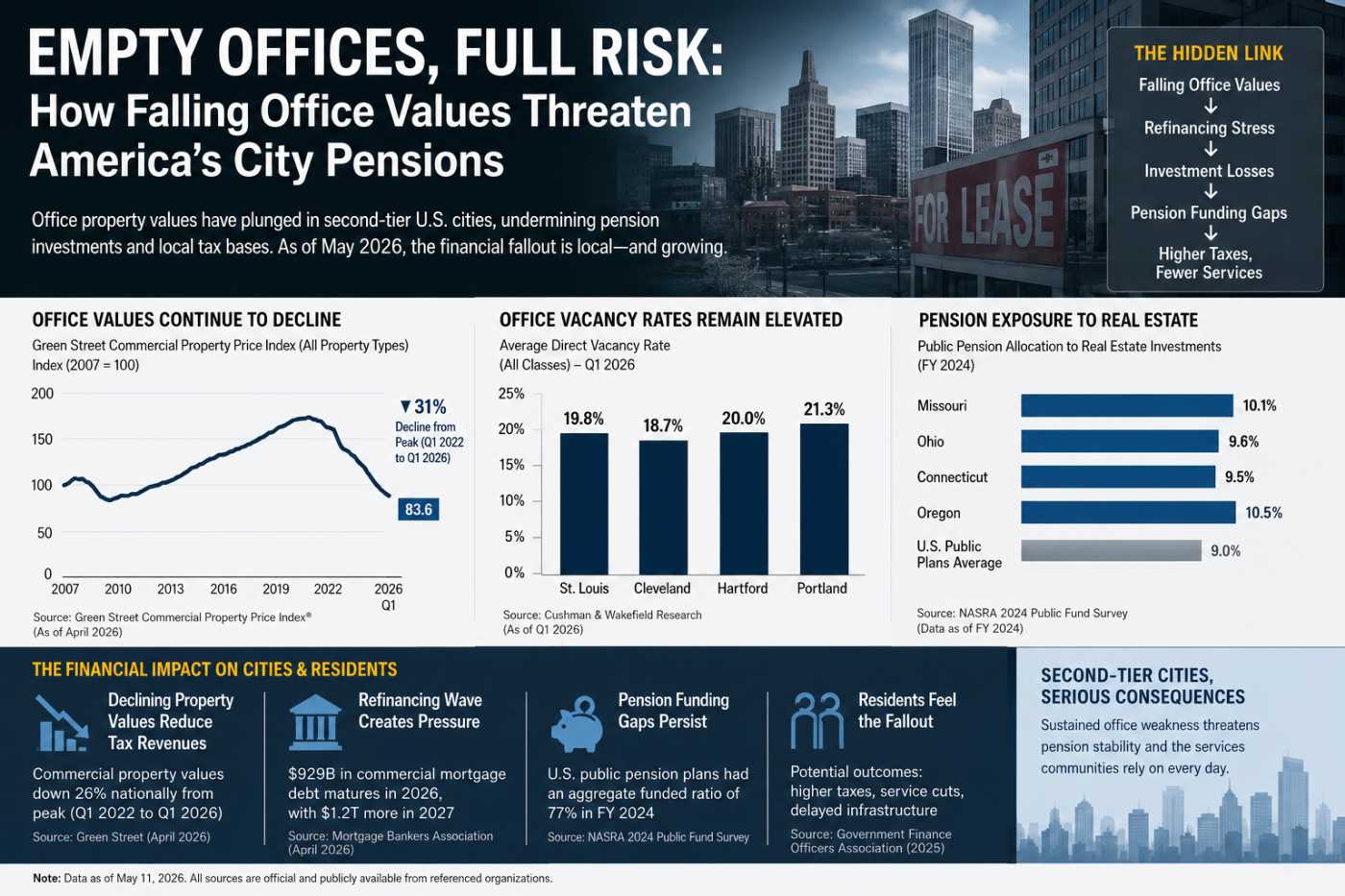

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

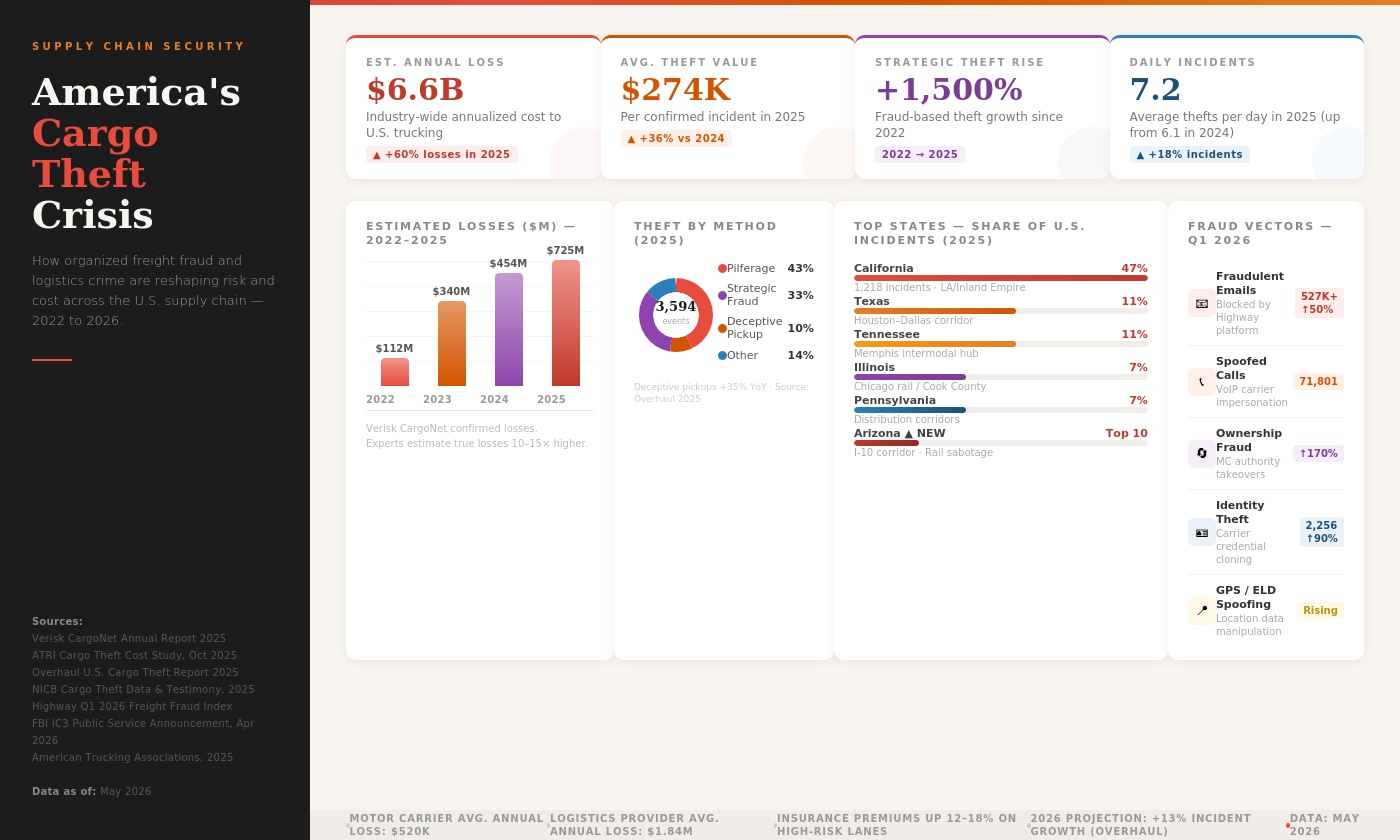

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

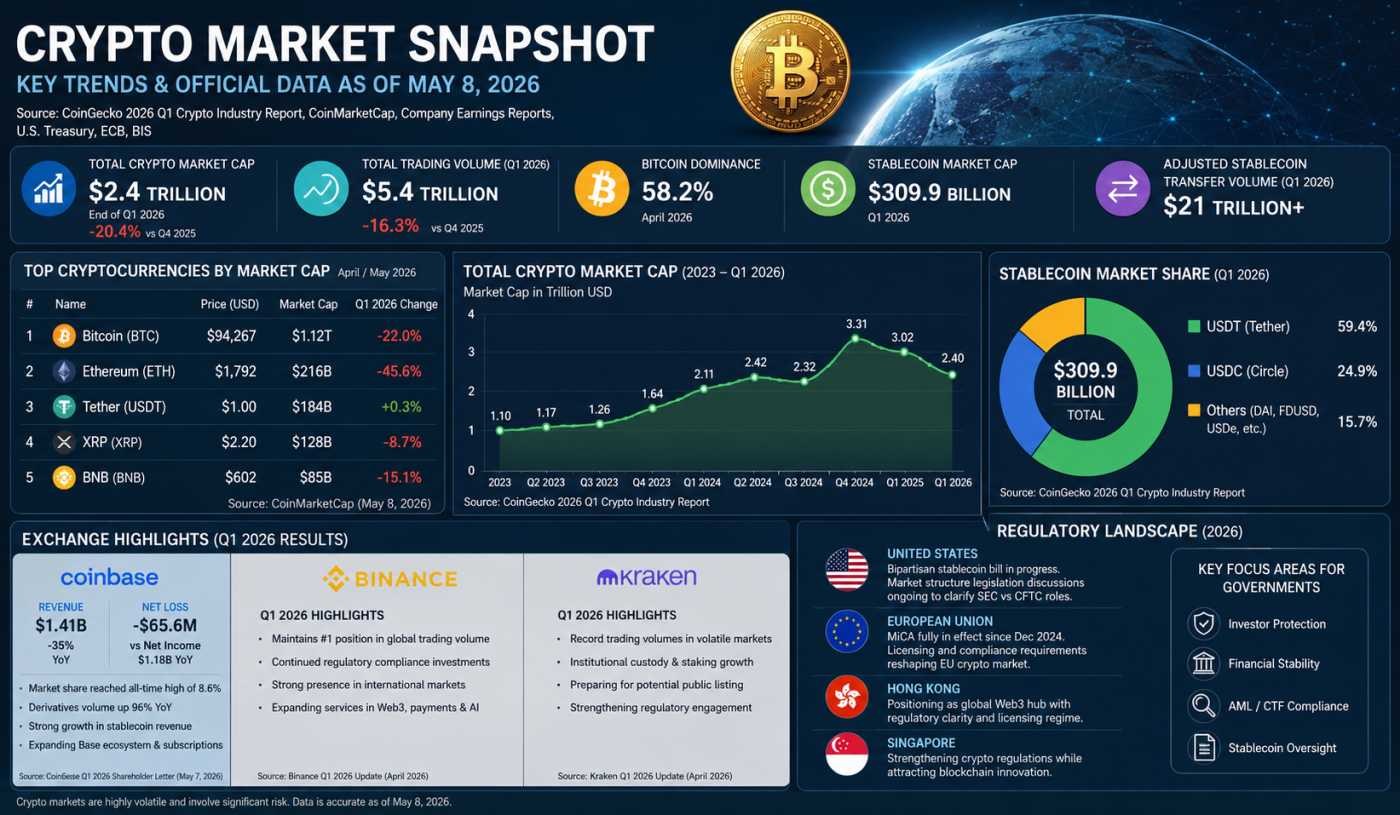

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

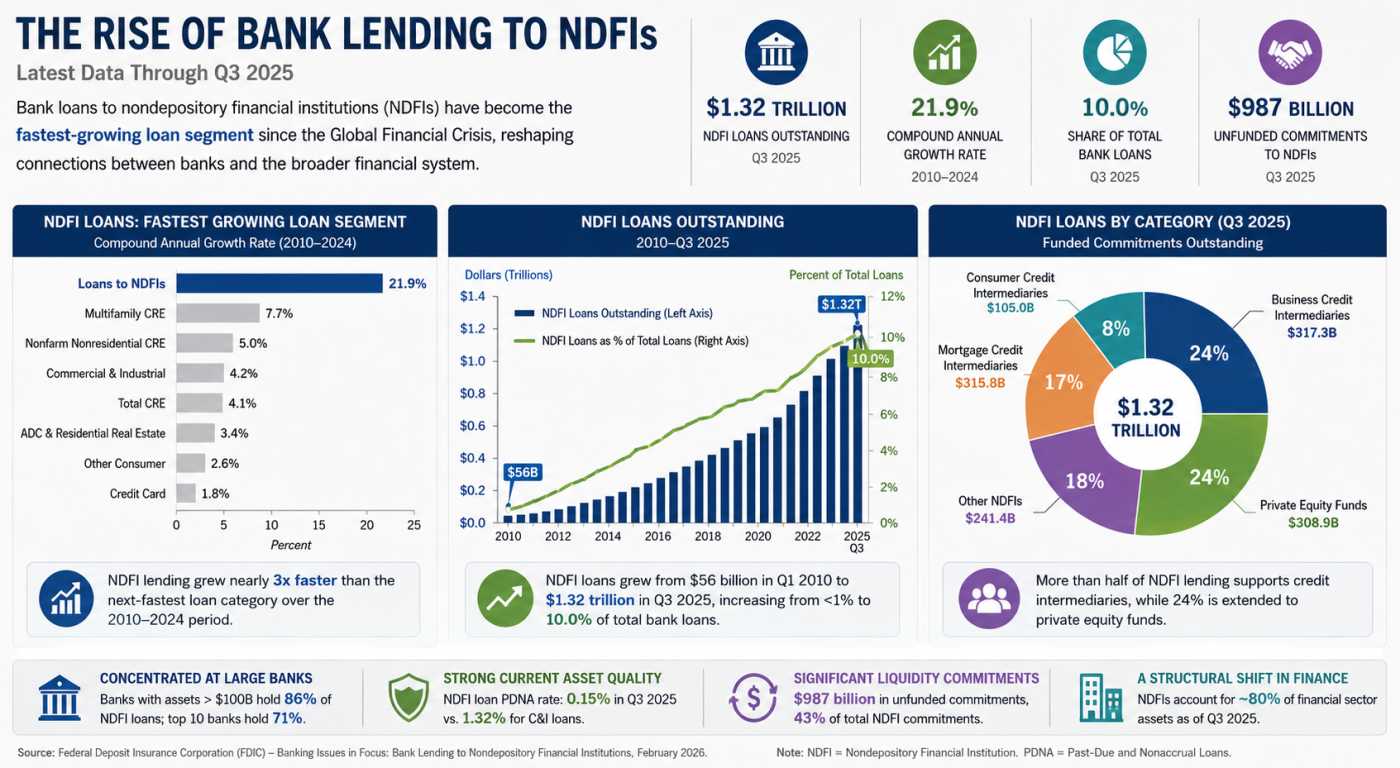

Bank lending to nondepository financial institutions (NDFIs) has quietly become one of the most important structural shifts in modern finance. A February 2026 report published by the Federal Deposit Insurance Corporation (FDIC), authored by Kate Fritzdixon and Joycelyn Lu, reveals that loans from banks to NDFIs have emerged as the fastest-growing category in banking since the 2008-2009 Global Financial Crisis. For investors, the trend offers a revealing look into how credit creation, liquidity provision, and risk transmission are evolving beneath the surface of the traditional banking system.

According to the FDIC report, outstanding bank loans to NDFIs surged from just $56 billion in early 2010 to approximately $1.32 trillion by the third quarter of 2025. That represents a compound annual growth rate of nearly 22 percent, dramatically outpacing every other major lending category tracked in U.S. bank Call Reports. Multifamily commercial real estate loans, the next-fastest-growing segment, expanded at less than one-third that pace.

For investors, the significance is not simply the scale of growth, but what it says about the changing structure of the financial system. NDFIs now account for 10 percent of all bank loans and more than one-third of lending to businesses not secured by real estate. The result is a financial ecosystem where banks increasingly finance the lenders, funds, and intermediaries that themselves finance households and corporations.

The Rise of the Financial Middle Layer

NDFIs include mortgage lenders, finance companies, insurance firms, private equity funds, private credit funds, broker-dealers, securitization vehicles, and asset managers. Unlike banks, these institutions do not rely primarily on insured deposits. Instead, they depend on capital markets, institutional investors, warehouse funding, subscription lines, and revolving credit facilities from banks.

The FDIC data suggests that banks are increasingly becoming infrastructure providers to the broader nonbank financial system. This shift matters because many of the fastest-growing corners of credit markets now sit outside traditional bank balance sheets. Private credit funds, venture capital vehicles, mortgage intermediaries, and securitization conduits have all expanded aggressively during the era of low interest rates and abundant liquidity.

One of the most striking findings in the FDIC report is the concentration of these exposures. Banks with assets greater than $100 billion hold approximately 86 percent of all bank loans to NDFIs, while just ten institutions account for roughly 71 percent of total exposure. This concentration effectively ties the health of large banks to the stability of private credit and nonbank financing markets.

The trend also illustrates how financial innovation has altered the flow of capital. In previous decades, banks originated and retained a larger portion of loans. Today, many forms of lending are originated, packaged, distributed, or managed by nonbanks, while banks increasingly provide the leverage and liquidity behind the scenes.

Why Investors Should Pay Attention to Private Credit

The growth of private credit appears to be one of the central drivers of NDFI expansion. The report notes that banks have reduced exposure to highly leveraged borrowers and unprofitable companies over the past decade, especially following the 2013 Interagency Guidance on Leveraged Lending. As banks tightened underwriting standards, private credit funds stepped into the gap.

This dynamic has created a parallel lending universe. Companies that may struggle to access syndicated bank loans can often secure financing from private debt providers willing to offer higher leverage ratios, faster approvals, and customized deal structures.

For investors, this has two major implications. First, private credit has evolved from a niche alternative asset class into a major channel of corporate finance. Separate industry data cited in the FDIC report indicates that private equity, private credit, and real estate fund assets expanded from around $500 billion in 2000 to more than $7 trillion by 2023.

Second, banks themselves are now indirectly exposed to this ecosystem through revolving credit facilities, capital call lines, and collateralized lending arrangements. In many cases, banks are no longer bearing the first layer of corporate credit risk directly. Instead, they are financing the entities that originate and hold those loans.

This creates a more interconnected financial structure. During periods of stability, the model can enhance liquidity and diversify funding channels. During periods of stress, however, losses or liquidity shocks inside the nonbank sector could migrate rapidly into the banking system.

New FDIC Data Reveals the Anatomy of NDFI Lending

One of the most important developments for investors may actually be regulatory rather than financial. Beginning in December 2024, U.S. banking regulators expanded Call Report disclosures to provide greater detail on NDFI exposures.

Banks with more than $10 billion in assets must now break down NDFI lending into five categories: mortgage credit intermediaries, business credit intermediaries, consumer credit intermediaries, private equity funds, and other NDFIs.

The third-quarter 2025 data provides the clearest picture yet of where risks and opportunities are accumulating. Mortgage credit intermediaries accounted for approximately $315.8 billion in funded exposure, while business credit intermediaries represented $317.3 billion. Consumer credit intermediaries accounted for $105 billion, private equity funds represented $308.9 billion, and other NDFIs made up roughly $241.4 billion.

The composition is revealing. More than half of all NDFI lending now supports credit intermediaries directly involved in originating or packaging loans. Meanwhile, nearly one-quarter supports private equity funds, much of it through capital call facilities secured by investor commitments.

For investors tracking systemic risk, the new reporting framework provides a more transparent map of the shadow banking ecosystem. The data also underscores how deeply embedded nonbank finance has become within regulated banking institutions.

The Hidden Liquidity Risk

Perhaps the most underappreciated figure in the report is not the $1.32 trillion in funded loans, but the $987 billion in unfunded commitments tied to NDFIs. Roughly 43 percent of total NDFI commitments remain undrawn.

These facilities are often structured as revolving credit lines. Under normal market conditions, utilization rates may remain manageable. During periods of stress, however, nonbank borrowers may rapidly draw down available funding to replace evaporating market liquidity, investor withdrawals, or frozen securitization markets.

This creates a classic liquidity transmission channel. If multiple NDFIs simultaneously seek funding, banks could face sudden liquidity pressures precisely when financial markets are already unstable.

The Bank for International Settlements highlighted similar concerns in a 2025 report examining interconnections between banks and nonbank financial intermediaries. The concern is not necessarily immediate defaults, but rather the possibility of synchronized liquidity stress spreading through interconnected balance sheets.

For investors, this distinction matters. Modern financial crises increasingly emerge from funding mismatches and liquidity spirals rather than straightforward credit deterioration.

Asset Quality Remains Surprisingly Strong

Despite rapid growth, current loan performance metrics remain favorable. The FDIC report notes that the past-due and nonaccrual (PDNA) rate for bank loans to NDFIs stood at just 0.15 percent in the third quarter of 2025. By comparison, commercial and industrial loans recorded a PDNA rate of 1.32 percent.

Several factors explain the stronger performance. Many NDFI credit facilities are heavily collateralized and structured with conservative advance rates. Capital call facilities to private equity funds are often backed by contractual investor commitments from pension funds, sovereign wealth funds, and institutional investors. Additionally, some NDFIs operate with long lock-up periods that reduce redemption pressure.

Large banks also appear to manage these exposures more effectively than smaller institutions. Banks with assets exceeding $100 billion reported an NDFI PDNA rate of just 0.12 percent, compared with 0.49 percent at banks with assets under $10 billion.

Still, investors should be cautious about extrapolating current performance indefinitely. Many rapidly growing private credit and nonbank lending platforms have not yet experienced a full credit cycle under prolonged high interest rates and tighter liquidity conditions.

The report explicitly notes that newer NDFIs may not have been fully tested during a severe downturn. If collateral values decline sharply or secondary market liquidity evaporates, banks could face indirect exposure through pledged assets and committed facilities.

A Structural Shift, Not a Temporary Trend

The broader context may be even more important than the current numbers. According to Federal Reserve Financial Accounts data cited by the FDIC, NDFIs collectively account for roughly 80 percent of total financial sector assets, a share that has remained relatively stable since 2000 even as the financial system itself expanded dramatically.

Total financial sector assets rose from approximately $40 trillion in 2000 to $148 trillion by the third quarter of 2025. Meanwhile, the ratio of financial sector assets to GDP climbed from 400 percent to 477 percent.

Exchange-traded funds alone expanded from just $40 billion in assets in 2000 to $12.6 trillion in 2025. Mutual funds quadrupled to $23.5 trillion. The transformation reflects a financial system increasingly dominated by asset managers, investment vehicles, and capital market intermediaries rather than traditional deposit-funded banks.

For investors, this means that understanding future market dynamics may require looking beyond conventional banking indicators. Liquidity conditions inside private funds, leverage embedded in financing vehicles, and refinancing capacity within nonbanks may become just as important as traditional bank earnings or loan growth metrics.

The FDIC's expanded reporting regime effectively acknowledges this reality. Regulators are no longer treating NDFIs as peripheral actors. Instead, they are recognizing that the modern financial system increasingly operates through a network of interconnected banks, private funds, securitization structures, and capital market intermediaries.

For markets, that interconnectedness may become one of the defining financial themes of the second half of the decade.

If you have enjoyed reading, spread the word:

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun

The Repair Economy Boom in Rural America

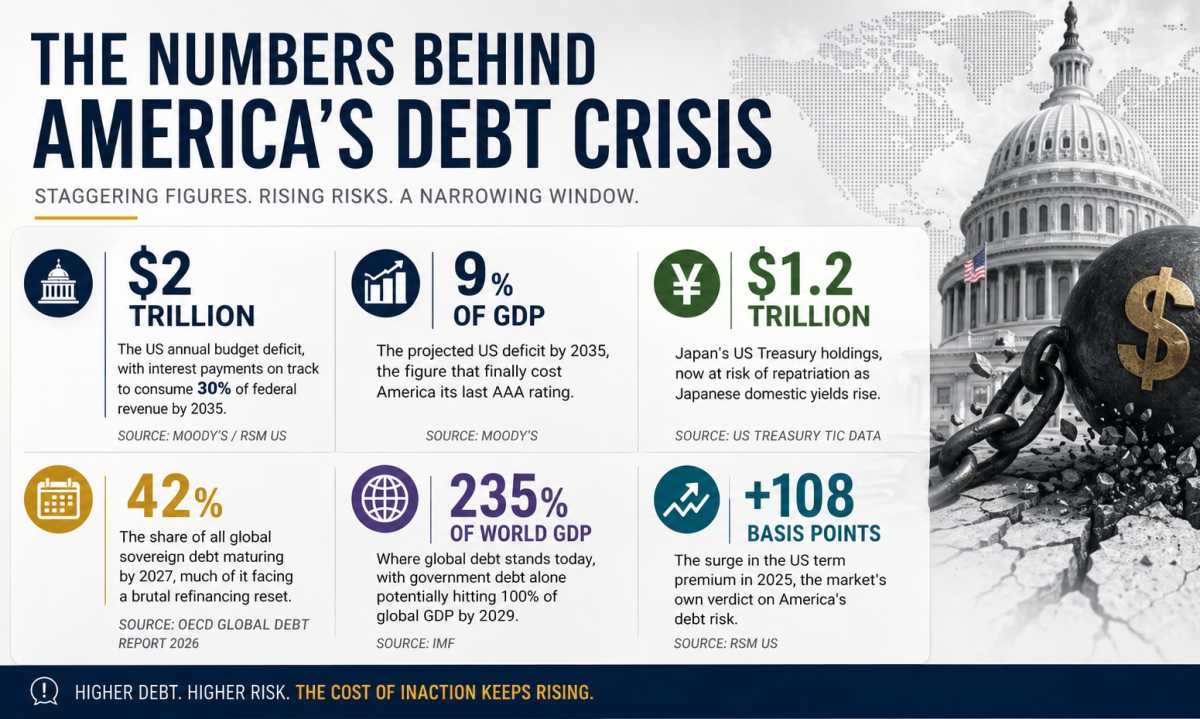

Debt, Deficits & Disaster: The Bond Market Crisis