Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

When Flooding Pays: A New Financial Bet

Breakfast for Life How Local Diners and Hardware Stores are Outsmarting Amazon

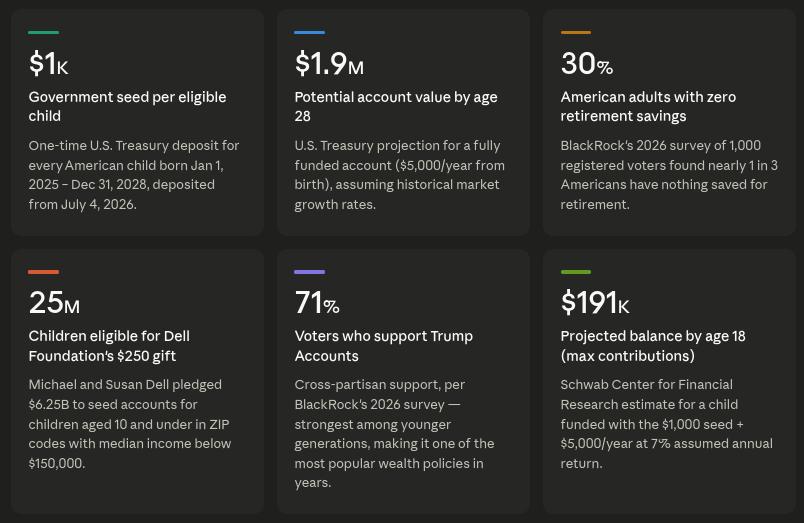

Before They Can Walk, They're Invested: How Trump Accounts Are Transforming Financial Culture

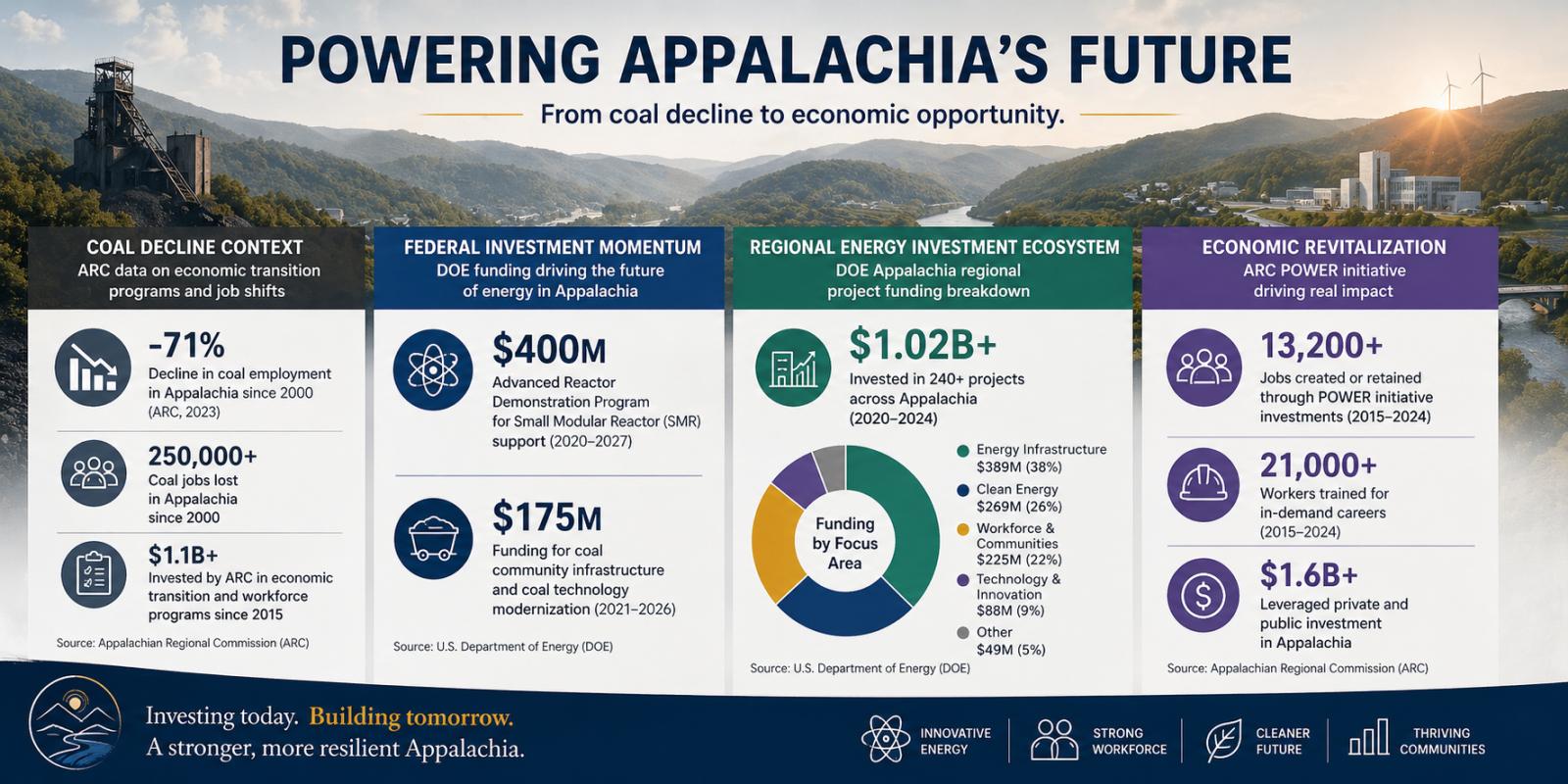

The Appalachian Energy Reboot: Inside the Unexpected Nuclear Startup Boom

Theatrical Finance: Credit Unions Use Drama to Attract Youth

Not Wall Street, But AI: The Real Force Democratizing Finance Across America

The Quiet Financial Revolution No One on Wall Street Saw Coming

In the long arc of American finance, personalization has always been a luxury product. For decades, the idea of tailored financial advice meticulously calibrated to an individual’s income volatility, regional economic conditions, and personal aspirations was reserved for clients with portfolios large enough to command attention inside glass towers in New York or San Francisco. Everyone else got something far blunter: standardized credit scores, templated lending decisions, and generic budgeting advice.

That hierarchy is now being quietly dismantled not by legacy banks, but by a new generation of AI-powered financial tools that are spreading into places Wall Street rarely studied, let alone served. Rural counties in Mississippi, tribal lands in Arizona, and post-industrial towns across Ohio and Pennsylvania are emerging as unlikely frontiers of financial sophistication. And the transformation is not theoretical it is measurable, lived, and increasingly visible in the way small businesses operate and households plan their futures.

From Static Advice to Living Financial Systems

At the core of this shift is a simple but profound change: financial advice is no longer static. AI systems are turning it into something dynamic, continuously updated, and hyper-contextual. Instead of a one-time consultation or a quarterly review, users now interact with dashboards that adapt daily to changes in cash flow, supply costs, or even local weather patterns that affect foot traffic.

According to a 2025 report by the Consumer Financial Protection Bureau, authored by senior analysts focusing on fintech accessibility, over 42% of new financial tool adoption in the United States is now occurring outside major metropolitan areas. This marks a reversal from a decade ago, when innovation diffusion was heavily urban-centric. The same report highlights that subscription-based AI financial tools priced under $100 per month have seen a 3.5x increase in adoption among small businesses since 2022.

What distinguishes these tools is not just affordability, but capability. Features once exclusive to Fortune 500 finance departments predictive cash-flow modeling, scenario planning, and automated risk detection are now embedded in user-friendly interfaces accessible on a smartphone.

Main Street Meets Machine Intelligence

Consider a bakery owner in rural Mississippi. Historically, her financial planning might have consisted of handwritten ledgers, seasonal intuition, and occasional advice from a local banker. Today, she uses an AI-powered dashboard that forecasts demand fluctuations based on local school calendars, regional events, and historical sales data. It alerts her weeks in advance when ingredient costs are likely to spike and suggests optimal times to bulk-purchase flour or sugar.

In the Ohio Rust Belt, a second-generation auto mechanic faces a different set of challenges volatile parts prices, unpredictable customer demand, and thin margins. Using an AI-driven inventory system, he now receives predictive alerts about which components are likely to run short based on regional vehicle repair trends. The system doesn’t just flag shortages; it recommends pricing adjustments and promotional strategies tailored to his specific customer base.

These are not isolated anecdotes. Data from the Small Business Administration’s 2025 Small Business Profile, compiled under the Office of Advocacy, indicates that over 31% of small businesses in non-metro counties have adopted at least one AI-enabled financial or operational tool. The authors of the report note that the trend is particularly strong among businesses with fewer than 10 employees traditionally the least likely to invest in advanced software.

The $100 Threshold That Changed Everything

The economics of this transformation are striking. For less than $100 a month often closer to $40 or $50 small business owners can now access tools that replicate the analytical capabilities of corporate finance teams. This price point has proven to be a psychological and practical tipping point. It aligns with what economists describe as “micro-investment thresholds,” where the perceived risk of adoption is low enough to encourage experimentation.

Research from the Federal Reserve Bank of Kansas City, authored by regional economist Jordan Rappaport, underscores this dynamic. The study found that small businesses in rural areas are significantly more likely to adopt new technology when subscription costs remain below 2% of monthly operating expenses. AI financial tools have, perhaps inadvertently, hit this sweet spot.

But affordability alone does not explain the surge. Equally important is the shift in design philosophy. Modern AI tools are built for non-experts. They translate complex financial concepts into plain language, often accompanied by visualizations that make trends immediately apparent. Instead of asking users to interpret spreadsheets, they provide actionable insights: “You’re likely to face a cash shortfall in three weeks,” or “Raising prices by 3% could stabilize margins without reducing demand.”

The Human Bridge: Translating Technology into Trust

For all their sophistication, these tools do not operate in a vacuum. Their real impact is being unlocked by a network of local intermediaries community college instructors, librarians, and small business development center (SBDC) counselors who are acting as translators between technology and users.

In many rural and underserved communities, trust in financial institutions has historically been fragile. Decades of redlining, branch closures, and impersonal service have left a legacy of skepticism. AI tools, despite their promise, initially encounter the same barrier. This is where human bridges become indispensable.

Community colleges, in particular, have emerged as unlikely hubs of financial innovation. Instructors are incorporating AI financial tools into business and accounting curricula, not as abstract concepts but as practical skills. Students learn to use real dashboards to manage simulated businesses, and many carry those skills directly into local enterprises after graduation.

The American Association of Community Colleges, in a 2025 report authored by workforce development specialists, found that over 60% of community colleges have introduced some form of fintech or AI literacy program. These initiatives are often tailored to regional economic needs agriculture in the Midwest, tourism in the Southwest, manufacturing in the Rust Belt.

Librarians, too, are playing a pivotal role. In towns where the library remains one of the few accessible public institutions, staff are hosting workshops on digital financial tools, guiding users through setup प्रक्रesses, and helping them interpret outputs. Their involvement lends credibility to technologies that might otherwise seem opaque or intimidating.

Meanwhile, SBDC counselors are integrating AI tools into their advisory sessions. Instead of offering generic guidance, they can now work with clients in real time, using live data to explore scenarios and refine strategies. The result is advice that is both personalized and grounded in local realities.

Tribal Lands and the Rewriting of Financial Narratives

Perhaps the most profound impact of AI-driven financial tools is unfolding on tribal lands, where access to traditional banking services has often been limited. Here, the technology is not just enhancing existing systems it is filling fundamental gaps.

According to a 2025 study by the National Congress of American Indians, authored by policy analysts specializing in economic development, AI-enabled financial platforms are being adopted by tribal enterprises at an accelerating pace. These tools are helping businesses navigate complex revenue streams, including federal grants, tourism income, and local commerce.

More importantly, they are enabling a form of financial sovereignty. By providing granular insights into cash flow and risk, AI tools empower tribal leaders and entrepreneurs to make decisions with a level of precision that was previously unattainable. This is particularly significant in communities where economic resilience is closely tied to cultural preservation and self-determination.

Data as a Local Asset

One of the most underappreciated aspects of this transformation is the localization of data. Traditional financial models often rely on national averages or broad regional trends, which can obscure the realities of specific communities. AI tools, by contrast, are increasingly incorporating hyper-local data everything from regional supply chain disruptions to local event calendars.

This localization has a compounding effect. As more users in a given area adopt these tools, the data becomes richer and more accurate, further improving the quality of insights. In essence, communities are collectively building their own financial intelligence systems, tailored to their unique conditions.

The Brookings Institution, in a 2026 analysis led by senior fellow Mark Muro, highlights this phenomenon as a key driver of what it calls “distributed economic intelligence.” The report argues that when data and analytical capabilities are decentralized, they can unlock productivity gains in regions that have historically lagged behind national averages.

The Cultural Shift Toward Financial Agency

Beyond the metrics and case studies, there is a subtler but equally महत्वपूर्ण change underway: a shift in how people perceive their own financial agency. When individuals and small business owners have access to tools that demystify finance, they begin to see themselves not as passive participants but as active decision-makers.

This shift is evident in the language users employ. Instead of talking about “making ends meet,” they discuss “optimizing margins” or “managing liquidity.” These are not just semantic changes; they reflect a deeper engagement with financial concepts that were once considered out of reach.

Importantly, this democratization of financial sophistication does not eliminate risk or guarantee success. Markets remain volatile, and small businesses continue to face structural challenges. But the playing field is becoming less uneven. Information asymmetry long a defining feature of financial inequality is being eroded.

An Unfinished but Irreversible Transformation

The rise of AI-powered financial tools is not a panacea, nor is it without challenges. Issues of data privacy, algorithmic bias, and digital literacy remain significant. Yet, the trajectory is clear. What began as a niche innovation is evolving into a foundational layer of economic infrastructure.

And perhaps the most striking aspect of this transformation is where it is taking root. Not in the financial capitals that once dictated the terms of access, but in the communities that were long excluded from the conversation. In these places, technology is not just enhancing finance it is redefining who gets to participate in it.

For the first time in generations, the tools of financial foresight are within reach of those who need them most. And in that quiet redistribution of capability lies the potential for a more inclusive, resilient, and dynamic American economy.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

Fraud, Delays, and High Fees—Gone: The Underrated Fintech Shift Reshaping U.S. Local Economies

From Rhode Island to Vermont: The Proficiency Gap That's Quietly Dividing New England's Workforce

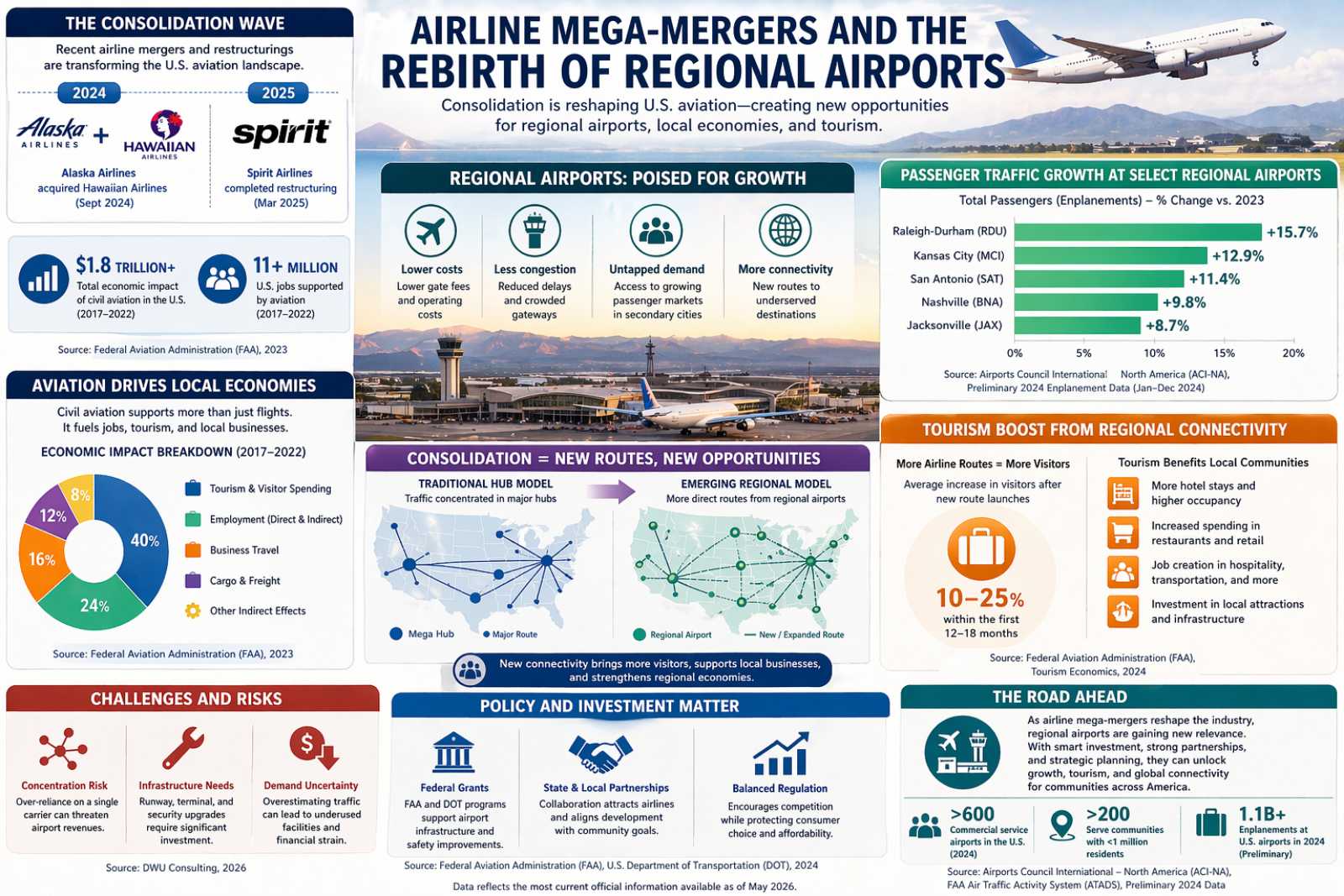

Regional Airports Poised for Growth Amid Airline Shakeups

From Fuel Shock to Factory Revival: The Surprising Rise of Hyper-Local Supply Chains in the U.S.