Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

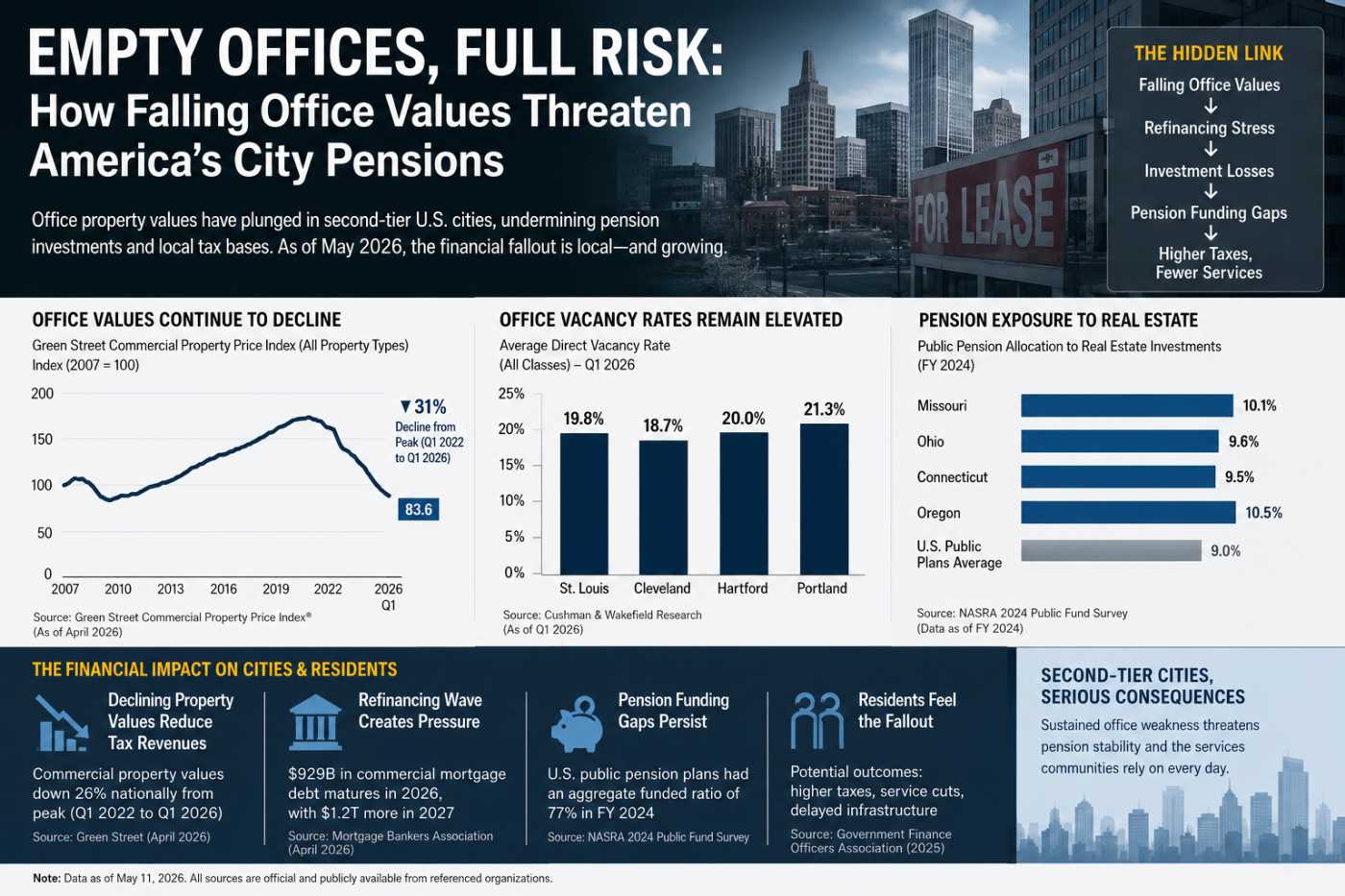

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

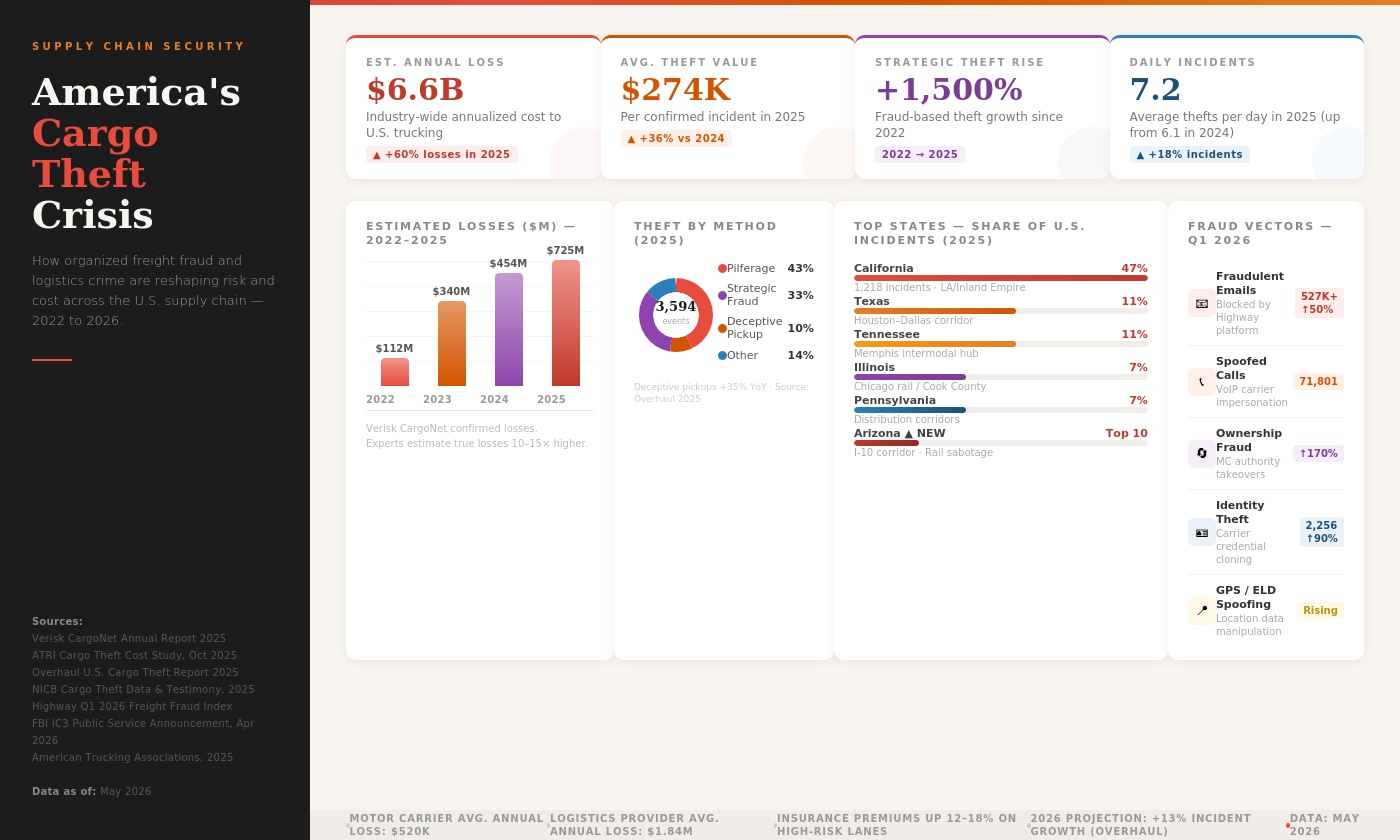

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

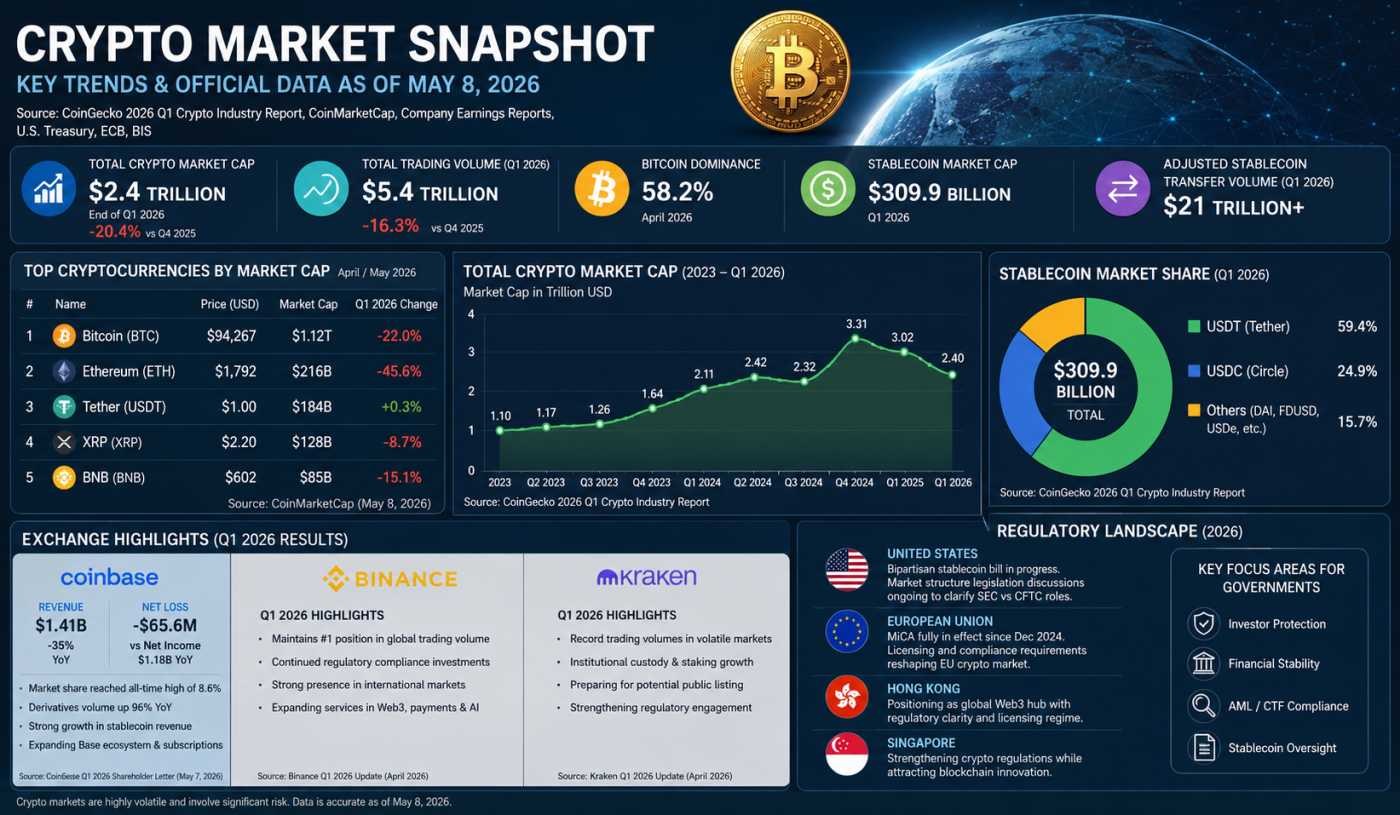

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

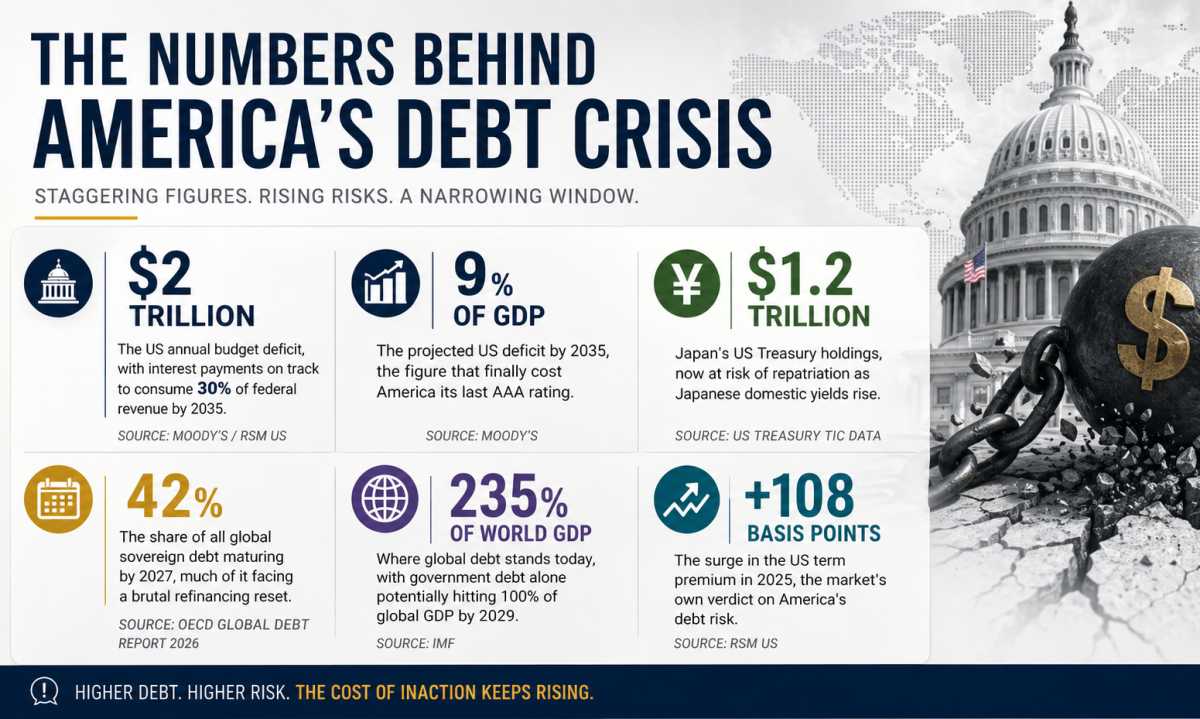

Debt, Deficits & Disaster: The Bond Market Crisis

The Gathering Storm: Why the Global Bond Market Is in Danger

On April 28, 2026, JPMorgan Chase CEO Jamie Dimon the head of the world's largest bank by market capitalization delivered one of his starkest warnings yet about the state of the global debt markets. Speaking at an investment conference hosted by Norway's sovereign wealth fund, Dimon said plainly: "The way it's going now, there will be some kind of bond crisis." It was not a casual remark. It was a carefully delivered judgment from the man who oversees a balance sheet larger than many nations' entire economies, and it deserves serious attention from anyone with money in bonds, savings, mortgages, or pensions which is to say, nearly everyone.

Dimon's Warning: Geopolitics, Oil, and Deficits

Dimon's April 2026 warning was not his first on this subject, but it was arguably his most urgent. "The level of things that are adding to the risk column are high, like geopolitics, oil, government deficits," he told the audience. "They may go away, but they may not, and we don't know what confluence of events causes the problem." His concern is structural, not cyclical. A bond crisis, he explained, would likely mean a sudden jump in yields and a breakdown in market liquidity investors rushing to sell while buyers recede forcing central banks to step in as buyers of last resort, echoing the 2022 United Kingdom gilt crisis when the Bank of England had to intervene to stabilize surging yields on British government bonds.

This warning follows a pattern of escalating concern from Dimon. Earlier, in his annual shareholder letter released on April 6, 2026, the JPMorgan chief cast himself as the "skunk at the party," stating that the biggest risks to markets are still being underpriced. He pointed to the war in the Middle East potentially causing "significant ongoing oil and commodity price shocks," along with the risk of "stickier inflation" that could keep interest rates higher than markets expect. He also warned that "high asset prices, which certainly feel good in the short run, create additional risk if anything goes wrong" a pointed message to investors anchored in complacency.

America's Fiscal Abyss

The backdrop to Dimon's warnings is a US fiscal picture that has deteriorated dramatically. In May 2025, Moody's Ratings cut the United States' sovereign credit rating from Aaa the highest possible down one notch to Aa1, citing what it described as "the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns." Moody's joined Standard & Poor's, which downgraded the US in August 2011, and Fitch Ratings, which did the same in August 2023. For the first time in history, all three major rating agencies had downgraded the United States below the top tier.

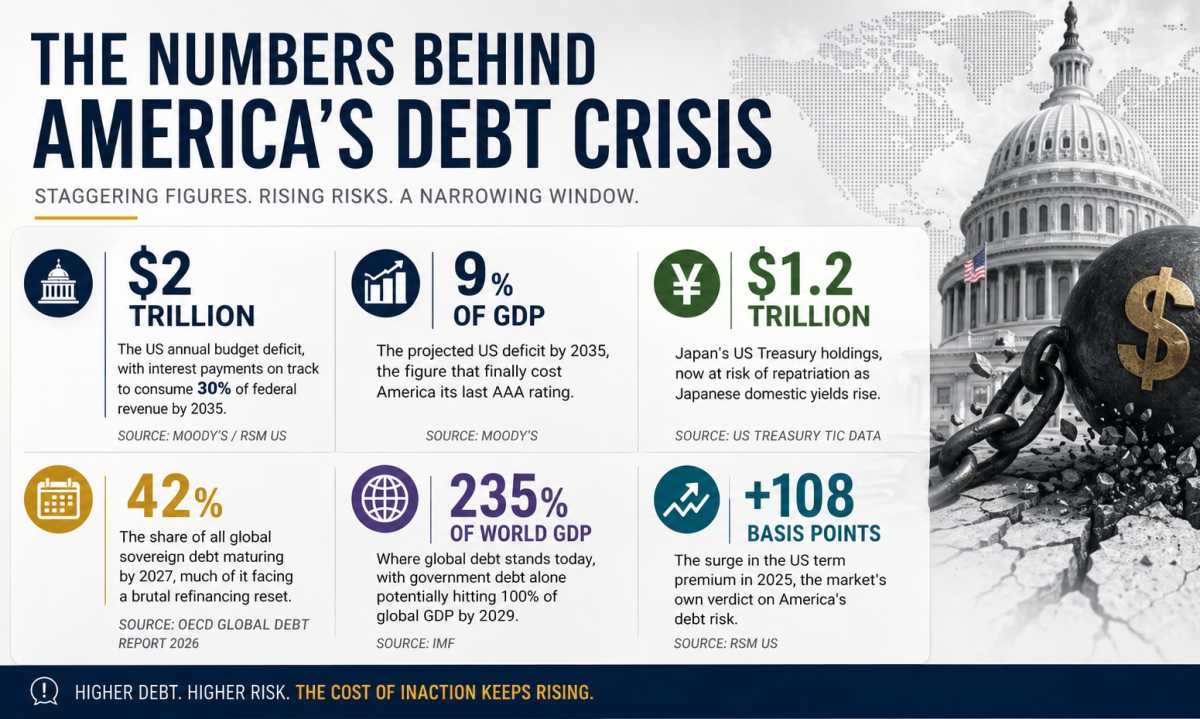

The numbers that prompted this unprecedented sweep of downgrades are sobering. Moody's projected that if the 2017 Tax Cuts and Jobs Act were extended which it called the base case the move would add approximately $4 trillion to the federal fiscal primary deficit over the next decade. The rating agency further warned that it expects federal deficits to widen to nearly 9% of GDP by 2035, up from 6.4% in 2024, driven mainly by rising interest payments on debt, growing entitlement spending, and insufficient revenue. RSM US, a leading middle-market consultancy, noted that interest payments on debt were already projected to rise from 9% of federal revenue to 30% of revenue by 2035 a figure that, if realized, would leave the US government with barely two dollars in every three available for anything other than debt service.

The Yale Budget Lab has separately estimated that current proposed legislation could add $3.4 trillion to the federal debt between 2025 and 2035, and a staggering $13.5 trillion between 2025 and 2055. Meanwhile, the US is currently running a budget deficit of roughly $2 trillion per year. The term premium the additional compensation investors demand for holding long-term Treasury bonds rather than rolling over short-term ones has risen by approximately 108 basis points in 2025 alone, reflecting mounting investor unease about the real risk of holding US government debt over the long run.

The IMF and OECD Sound the Alarm

The concerns are not confined to Wall Street. The International Monetary Fund's October 2025 Global Financial Stability Report warned that "sovereign bond markets face pressure from widening fiscal deficits," while noting that financial stability risks remain elevated across the world. The IMF's April 2026 Fiscal Monitor, titled "Fiscal Policy under Pressure: High Debt, Rising Risks," confirmed that financial market volatility has increased since late February 2026, with geopolitical tensions in the Middle East pushing global bond yields higher. The IMF expects global government debt to potentially reach 100% of global GDP by 2029, which would be the highest level since the aftermath of World War II.

The OECD's Global Debt Report 2026, published in March, highlighted a more structural risk: that geopolitical tensions can have an "outsized impact on demand from foreign investors," and that most sovereign issuers expect geopolitical risk to continue affecting both primary market operations and secondary market liquidity in government securities throughout 2026. The OECD also pointed out that 42% of all global sovereign debt is set to mature by 2027, meaning vast quantities of debt originally issued at near-zero interest rates will need to be refinanced at significantly higher rates a refinancing wall that threatens to substantially increase the debt service burden for governments worldwide.

Japan: The Canary in the Global Coal Mine

One of the most alarming signals in the global bond market in early 2026 has come from an unexpected corner: Japan. The yield on Japan's 40-year government bonds rocketed above 4.2% in January 2026, a record high. Japan's 10-year government bond yield simultaneously surged to its highest level since 1999, while 20-year yields jumped sharply as well. The trigger was Prime Minister Sanae Takaichi's pledge to suspend the consumption tax ahead of snap elections a move that analysts described as large-scale, near-term fiscal loosening at precisely the moment the Bank of Japan was trying to normalize monetary policy after decades of ultra-low interest rates.

The reason this matters far beyond Japan is the role Japanese investors play in global bond markets. As of November 2025, Japanese entities held approximately $1.2 trillion in US Treasury securities making Japan the largest single foreign holder of US government debt, according to the US Treasury Department's Treasury International Capital data. Ed Yardeni, president of Yardeni Research, put it plainly in comments cited by CNBC: "Now that their yields are going up, you're likely to see that Japanese bond investors may be more likely to stay home and invest in their own bonds rather than in the U.S., so that could put some upward pressure on U.S. bond yields." In short, as Japan's domestic bonds become more attractive, the global anchor that Japanese capital provided to US Treasury markets begins to loosen.

The Retreat of Foreign Buyers

Japan is not alone in this retreat. The People's Bank of China has also been selling US Treasury holdings in substantial monthly quantities, choosing to allocate resources to domestic priorities and diversify its reserves away from dollar-denominated assets. The OECD's Global Debt Report 2026 noted that demand from foreign investors has become "more uneven" across the board, contributing to persistently elevated long-dated yields even in the absence of high inflation. What is emerging is a structural shift in who is willing to buy US government debt, and at what price.

According to a Bank of America analysis published in December 2025, nearly half of investors surveyed expected the 10-year Treasury to end 2026 between 4% and 4.5%. Goldman Sachs, in its Fixed Income Outlook Q1 2026, noted a "steepening bias" in its US Treasury outlook, warning that fiscal expansion could push long-term yields higher. Charles Schwab, in its 2026 bond market outlook, flagged that the 10-year Treasury yield was likely to hold near 4% given sticky inflation, an expected increase in Treasury supply to finance growing federal deficits, and rising global bond yields. These forecasts, from some of the most respected financial institutions in the world, collectively paint a picture of a market where the gravitational pull of fiscal excess is keeping yields structurally elevated.

The Zombie Company Threat and Corporate Bonds

The dangers in the bond market are not confined to government debt. LPL Financial, in its 2026 fixed income outlook, warned of a growing tally of so-called "zombie companies" mostly smaller-cap firms with interest costs that exceed their income whose survival depends entirely on refinancing at rates that no longer exist. The refinancing wall looming in 2026 and 2027 poses additional risks, especially for companies that issued debt during the ultra-low-rate era and now face significantly higher rollover costs. LPL analysts warned that these firms may face restructuring or default unless they can repair their balance sheets, noting that credit spreads the additional return investors demand for holding risky corporate debt remain at or near historically tight levels even as underlying default risk is quietly rising.

The Dollar, the Reserve Currency Question, and Systemic Risk

Perhaps the deepest risk embedded in the current environment is one that Dimon has repeatedly raised: the potential erosion of confidence in the US dollar itself as the world's reserve currency. "If people decide that the US dollar isn't the place to be, you could see credit spreads gap out; that would be quite a problem," Dimon warned. "It hurts the people raising money. That includes small businesses, that includes loans to small businesses, includes high-yield debt, includes leveraged lending, includes real estate loans." As of mid-2025, the US dollar had already fallen nearly 10% a historically dramatic move for a reserve currency raising concerns at AllianceBernstein that continued dollar weakness could motivate Treasury holders to accelerate their selling, further driving yields higher in a self-reinforcing cycle.

Dimon has also connected these short-term market dynamics to a longer-term existential question for American economic supremacy. "If we are not the preeminent military and the preeminent economy in 40 years, we will not be the reserve currency. That's a fact. Just read history," he warned. The reserve currency status of the dollar is not simply a matter of financial prestige it is the mechanism by which the US borrows cheaply from the world, finances its deficits, and maintains geopolitical leverage. If that status begins to fray, the entire edifice of US fiscal management becomes more fragile.

A Global Problem With No Easy Exit

Yardeni Research's Ed Yardeni, speaking to CNBC, framed the challenge in terms that apply well beyond any single country: "The basic problem in the global bond market is this: major governments of the major economies are living deficits. They've accumulated a great deal of debt, and investors are starting to demonstrate that they're not happy about that." Global debt remains elevated after years of pandemic and stimulus-era borrowing, staying above 235% of world GDP even as private debt has eased slightly, while government obligations continue to swell and outpace economic growth.

Geopolitical pressures are adding a further layer of fiscal strain. NATO members, having agreed in 2025 to raise defense spending to 5% of GDP by 2035, face the long-term budgetary cost of a more militarized world. European nations, already wrestling with high debt ratios France at roughly 101% of GDP, the UK at around 115%, and the US at approximately 125% are under dual pressure from defense spending commitments and the need to refinance pandemic-era debt. The IMF's October 2025 Global Financial Stability Report warned that financial stability risks globally remain "elevated," with valuation models showing risk asset prices well above fundamentals, raising the specter of sharp corrections.

The road ahead for the global bond market is one of competing pressures: central banks trying to ease policy to support growth, while governments issue ever more debt to finance deficits, while foreign buyers quietly step back, while zombie companies approach their refinancing deadlines, and while geopolitical shocks continue to threaten both oil prices and investor sentiment. Jamie Dimon, with his unsettling directness, has named this confluence for what it is. The question is not whether the pressures are real the data from the IMF, OECD, Moody's, and markets themselves confirm that they are. The question is whether policymakers will act before the market delivers its own reckoning.

If you have enjoyed reading, spread the word:

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun

The Repair Economy Boom in Rural America

Debt, Deficits & Disaster: The Bond Market Crisis