Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

The Appalachian Energy Reboot: Inside the Unexpected Nuclear Startup Boom

Theatrical Finance: Credit Unions Use Drama to Attract Youth

Fraud, Delays, and High Fees—Gone: The Underrated Fintech Shift Reshaping U.S. Local Economies

From Rhode Island to Vermont: The Proficiency Gap That's Quietly Dividing New England's Workforce

Regional Airports Poised for Growth Amid Airline Shakeups

Before They Can Walk, They're Invested: How Trump Accounts Are Transforming Financial Culture

A $1,000 Seed and a Generational Promise: How Trump Accounts Are Quietly Changing What Wealth Means in Working-Class America

In the cramped waiting room of a pediatric clinic in eastern Kentucky, a laminated flyer taped to the wall has been quietly starting conversations that no one expected. It reads simply: "Your baby was born with $1,000. Here's how to claim it." The receptionist, a mother of three herself, has answered the same questions dozens of times since January: What is a Trump Account? Is it really free? Will this affect our food stamps? How do I fill out the form?

This is not the Wall Street story of 2026's most talked-about financial product. It is something far more intimate and arguably far more consequential. Across hollows, trailer parks, small farms, and immigrant neighborhoods from Appalachian Ohio to the cornfields of Iowa, a federal policy born inside a 2,000-page tax bill is slowly filtering down through the most unlikely of messengers: pediatricians, credit union tellers, PTA volunteers, and church secretaries. And for the first time in a generation, it is planting the idea that wealth is not just something you inherit or stumble into it can be built, deliberately, from the very first day of a child's life.

What the Law Actually Does and Why It Matters More in Some ZIP Codes Than Others

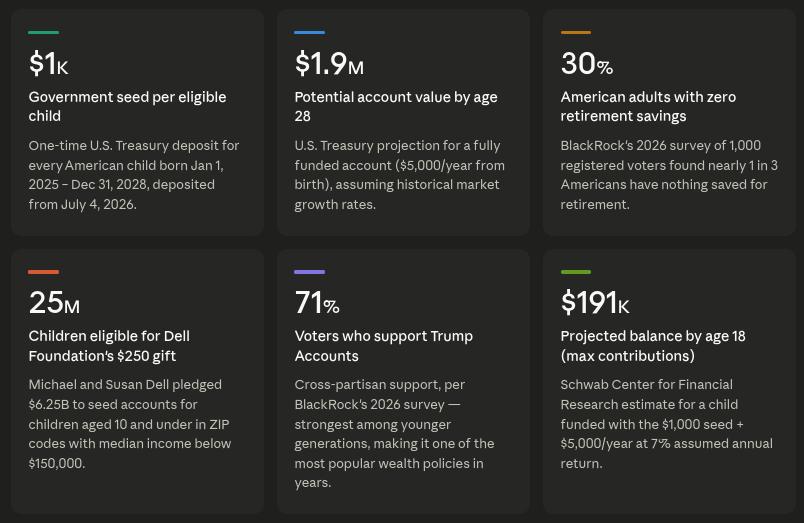

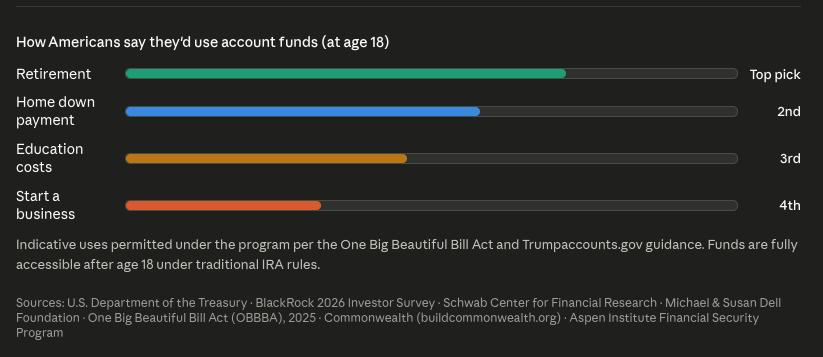

The Trump Account, formally known as the 530A Account, was created under the One Big Beautiful Bill Act signed into law in July 2025. Under the program, any U.S. citizen under the age of 18 with a valid Social Security number is eligible to have an account opened in their name. For children born between January 1, 2025, and December 31, 2028, the U.S. Treasury will deposit a one-time $1,000 seed contribution expected no earlier than July 4, 2026, the nation's 250th birthday. Parents, guardians, family members, and employers may contribute up to $5,000 per child per year (with employers allowed to contribute up to $2,500 of that amount as a pre-tax fringe benefit). The funds are invested in low-cost index funds or ETFs, with an expense cap of 0.10%, and cannot be withdrawn before the child turns 18.

In April 2026, the U.S. Treasury announced it had designated BNY Mellon as a financial agent to manage initial accounts, with Robinhood Markets partnering to develop a dedicated app and customer service platform. Families can initiate enrollment now by filing IRS Form 4547 with their 2025 tax return, or through the government's online portal at TrumpAccounts.gov.

The math alone is staggering in its long-term implications. According to projections from the U.S. Department of the Treasury, a fully funded account with maximum contributions of $5,000 per year from birth could be worth as much as $1.9 million by the time a child turns 28. Even more modestly, a child who receives only the initial $1,000 seed and no further contributions could, assuming modest 6% average annual returns, enter adulthood with nearly $3,000 and reach retirement age with over $44,000 a figure drawn from research compiled by the national nonprofit Commonwealth, which has been conducting outreach and research specifically focused on low-to-moderate income families. And for children born in qualifying low-income ZIP codes, there is an additional $250 charitable contribution from the Michael and Susan Dell Foundation a $6.25 billion philanthropic commitment announced in December 2025 that could reach up to 25 million children under the age of 11.

But here is the tension at the heart of this program and the reason the next few months matter enormously: enrollment is not automatic. A family must affirmatively opt in. And as Jin Huang, co-director of the Center for Social Development at Washington University in St. Louis, has noted, that design choice introduces a very real risk: the families who need the accounts most may never find out about them in time.

The Unlikely Outreach Network Taking Shape Across Small-Town America

Walk into the First Community Credit Union branch in a mid-sized town in western Pennsylvania on any given Tuesday morning, and you are likely to find a trifold brochure on the counter explaining Trump Accounts alongside a hand-lettered sign asking: "Did you have a baby in 2025 or 2026? Ask us about your child's $1,000." The branch manager, a 34-year-old who grew up in the same county and whose own parents never had a savings account until their 40s, runs monthly information sessions with local parents often in partnership with the nearest Women, Infants, and Children (WIC) office two streets away.

America's Credit Unions, the national advocacy organization, has been actively lobbying the Treasury Department to designate credit unions as eligible trustees for 530A accounts a move that could dramatically expand reach in communities where traditional banks are scarce. Credit unions already serve as trusted financial partners in tens of thousands of rural and underserved communities across the country, and their not-for-profit structure and member-first philosophy make them natural conduits for this kind of wealth-building outreach.

Meanwhile, Commonwealth the Boston-based national nonprofit launched a formal research initiative in early April 2026 specifically designed to map how low-to-moderate income families learn about and engage with Trump Accounts, and to develop messaging and outreach strategies that actually work in these communities. The organization has been building a coalition of regional and community-based partners pediatric practices, Head Start programs, employer payroll departments, and faith communities to serve as trusted messengers. Their research is urgency-driven: the optimal window for securing the $1,000 government seed contribution for eligible 2025 newborns is shrinking with every passing month.

The Aspen Institute's Financial Security Program has similarly sounded an optimistic but cautious note, calling the Trump Account potentially "one of the most significant federal investments in child asset-building in decades" while emphasizing that policy design and community implementation will determine whether it becomes a universal ladder or a tool that primarily benefits families who are already financially connected. Their researchers have been studying lessons from Maine's My Alfond Grant program a decade-old state-level baby bond initiative as a successful template for what universal early wealth-building can look like when it is delivered with genuine grassroots infrastructure.

Maria's Story: "I Never Thought the Government Would Do Something Like This for Us"

Maria Reyes-Gutiérrez does not think of herself as an investor. She is 28 years old, works the morning shift at a food processing facility in rural central Iowa, and sends $200 a month back to her mother in Oaxaca, Mexico. When her daughter Esperanza was born in February 2025, Maria assumed the first year would be spent simply staying afloat. She had no 401(k), no savings account to speak of, and no experience with anything she would describe as a "financial product."

She learned about the Trump Account in the most accidental of ways a bilingual flyer stapled to the bulletin board at her daughter's daycare, put there by a local volunteer from a community development financial institution (CDFI) that had been partnering with the facility since early 2026. The volunteer, who spoke Spanish, explained the basics: the federal government would put $1,000 into an investment account for Esperanza, automatically growing in a stock index fund until she turned 18. Maria would need to fill out a single IRS form. The account would be in her daughter's name. She could add money if she ever had extra, up to $5,000 per year or she could simply let the $1,000 seed grow untouched for 18 years.

"I asked her three times if this was real," Maria says, laughing softly. "I thought there must be some catch. But she said, no this is the law. Your daughter was born into this." Maria submitted her Form 4547 in March, with help from a volunteer tax preparer at her local VITA (Volunteer Income Tax Assistance) site. Because Esperanza was born in a ZIP code with a median household income below $150,000, she also qualifies for the additional $250 Dell Foundation charitable deposit meaning her account will be seeded with at least $1,250 on July 4th. "For someone like me, that is not just money. That is hope with a number on it."

The Harmon Family: When a Coal County Learns to Think Long-Term

In Letcher County, Kentucky one of the most economically distressed counties in Appalachia, where median household income hovers around $32,000 and generational poverty has been woven into the landscape for decades the Trump Account is landing in ways that go beyond the balance sheet.

Darlene Harmon is 31, a home health aide and single mother of two. Her youngest, a boy named Cody, was born in October 2025. Darlene had never thought about retirement planning the concept felt like a luxury for a different class of person, the kind of family that lived in the newer houses on the other side of the county road. But when her son's pediatrician's office distributed a one-page explainer about Trump Accounts in January 2026 part of a coordinated push by the local federally qualified health center to reach parents during well-baby visits something shifted.

"The doctor's office is the one place every mama goes with their baby," says a regional coordinator at a local CDFI who helped develop the outreach materials. "We realized it was the most trusted point of contact we had." Darlene enrolled Cody in the program through TrumpAccounts.gov with help from a family resource center at her county's elementary school, which had set up a tablet station specifically for parents who did not have reliable internet access at home. She was also pointed toward the employer contribution provision: her employer, a regional home health agency, has since announced it will match the government's $1,000 for all employees' eligible children a benefit Darlene describes as "the first time this job ever felt like it was investing in me."

"I used to think that money was something that happened to other people," she says. "But Cody's going to know he had something in his name since the day he was born. That changes something in your head."

What Local Financial Advisors Are Seeing and Why They Are Surprised

Across small-town America, a cohort of local financial planners and credit union loan officers are watching something unfold that they did not expect: a genuine cultural conversation about long-term wealth is breaking out in communities where such conversations have historically been absent.

"On Wall Street, a $1,000 account is a rounding error. On Main Street, it is a breakthrough," says one certified financial planner based in rural western North Carolina who has been hosting evening informational sessions at the local library. "The number isn't the point. The point is that for the first time, a parent who has never owned a stock in her life is being asked to think about what her child's money might look like in 18 years. That is a fundamentally new conversation."

The bipartisan support for the program has itself been striking. A BlackRock survey published earlier in 2026 found that 71% of voters across the political spectrum support the concept of Trump Accounts, with the strongest enthusiasm among younger generations. BlackRock CEO Larry Fink, in his annual chairman's letter to investors in March 2026, cited Aspen Institute research from 2023 showing that early wealth-building accounts make it statistically more likely for recipients to earn advanced degrees, start a business, and own a home. BlackRock, Bank of America, and JPMorgan Chase are among the major employers that have announced they will match the government's $1,000 seed contribution for their U.S. employees' eligible children.

But it is in the communities farthest from those corporate headquarters where the conversation feels most electric and most fragile. Commonwealth's ongoing research has found that awareness of the program remains alarmingly low among exactly the families the seed contribution is designed to help. Many parents in low-income households do not realize enrollment is optional and time-sensitive. Others are confused about whether participation could affect eligibility for means-tested benefits a fear that, while largely unfounded based on current guidance, speaks to a deep institutional distrust that any outreach strategy must acknowledge and address.

The $15 Billion Bet on a Different Kind of American Dream

At its core, the Trump Account is a bet a bipartisan, $15 billion federal wager, according to projected cost estimates that giving every American child an early stake in the stock market will change not just their balance sheets but their relationship to the future itself. The evidence from international precedents is encouraging: programs in Canada, the United Kingdom, and Singapore have shown that early wealth-building accounts correlate with higher educational attainment, greater rates of homeownership, and improved psychological well-being, according to research cited by BlackRock's Larry Fink.

Charles Schwab's Center for Financial Research has modeled that a child born today whose family maxes out the $5,000 annual contribution each year could accumulate more than $191,000 by age 18 more than twice what most American adults currently have saved for retirement. Even assuming no family contributions beyond the initial $1,000 seed, the account projects to grow meaningfully over 18 years through the compounding power of broad U.S. equity index exposure.

What no projection can fully capture is the subtler transformation playing out in real time in waiting rooms and PTA meetings and Sunday school halls from Pike County, Kentucky to Story County, Iowa. It is the quiet but seismic shift in what it means to be born in America in 2025 or 2026: the idea, novel for millions of families, that from your very first breath, the market is working for you. That you have a stake. That the distance between your starting line and a life of financial security is not fixed.

For Darlene Harmon in eastern Kentucky, and for Maria Reyes-Gutiérrez in central Iowa, and for the tens of thousands of parents like them who are learning about a government form in a pediatrician's waiting room or at a credit union teller's window, the Trump Account is not a retirement vehicle or a tax-planning instrument. It is something older and more human than that. It is the first evidence that someone, somewhere, planned ahead for their child even before they knew how.

DISCLAIMER: We provide information and our musings based on events, but nothing on this site can be considered professional advice of any kind.

If you have enjoyed reading, spread the word:

From Fuel Shock to Factory Revival: The Surprising Rise of Hyper-Local Supply Chains in the U.S.

AI Data Centers Transform Small-Town USA: Jobs, Taxes, and Tech Ecosystems Explode

The $919 Billion Warning: What the Wholesale Inventory Explosion Really Means for Main Street

How U.S. Cities Are Turning Data and Infrastructure into Billion-Dollar Opportunities