Good prospects:

Latest Regulatory Filings for SP5

Companies with the best and the worst fundamentals.

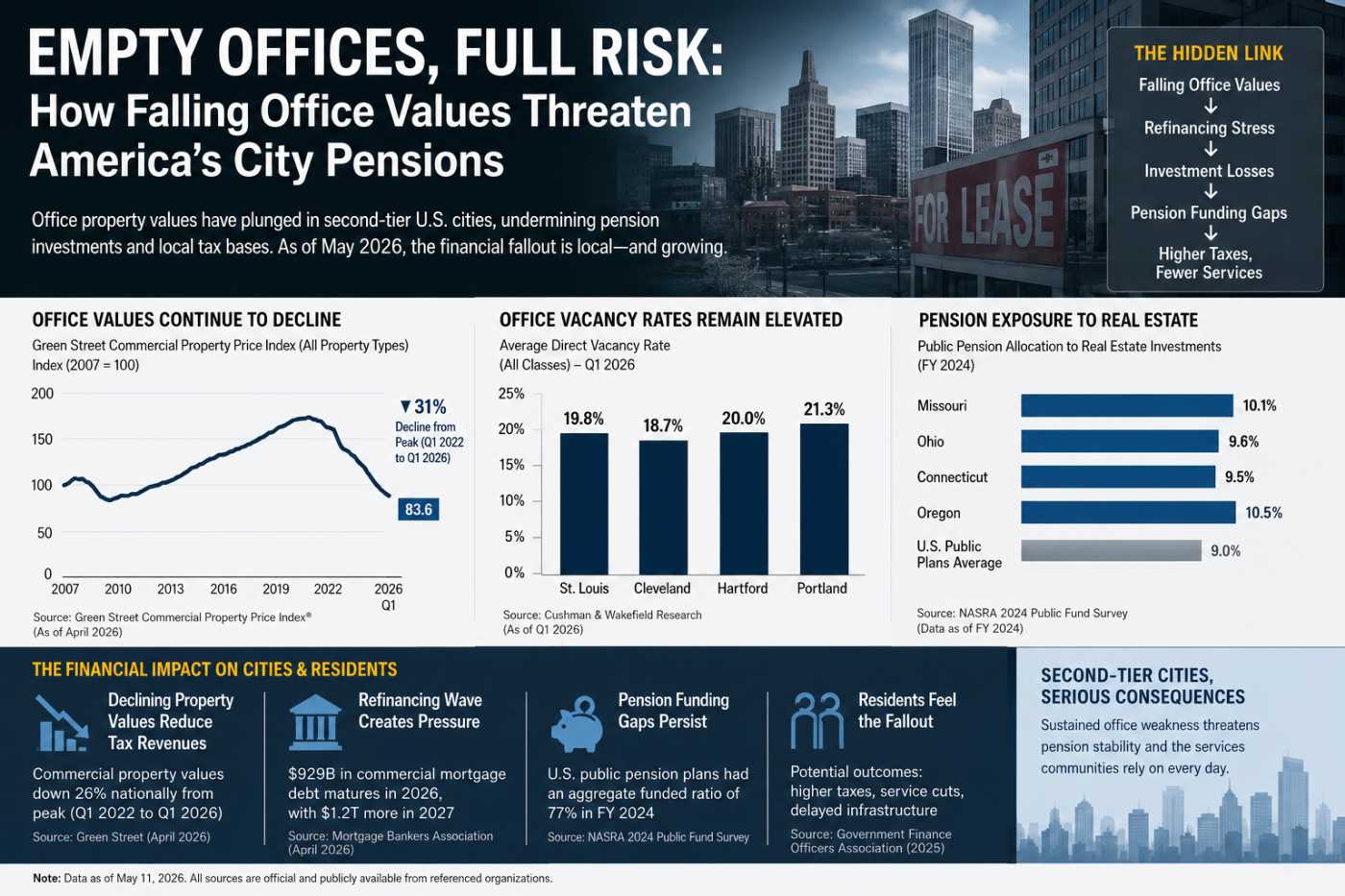

America’s Empty Offices Hit Pensions Hard

Rural Hospitals Buckle Under Private Equity

Fake Brokers, Spoofed GPS: Who Pays for Cargo Crime?

Crypto’s $2.4T Reality Check in 2026

The Machines That Ate the Grid: Five Centuries of Power Hunger

America’s Empty Offices Hit Pensions Hard

The Pension Risk Hidden Inside America’s Empty Offices

As of May 2026, the commercial real estate downturn in the United States is no longer confined to headlines about empty skyscrapers in San Francisco or Manhattan. A quieter but increasingly dangerous financial problem has emerged in second-tier American cities where municipal pension systems, regional retirement funds, and local redevelopment agencies became deeply intertwined with office real estate during the low-interest-rate era of the 2010s. In cities such as St. Louis, Cleveland, Hartford, and Portland, falling office valuations are beginning to expose structural weaknesses that could ultimately affect local taxpayers, public services, and long-term infrastructure investment.

Unlike the highly visible banking stresses of 2023 and 2024, the risks building inside regional pension systems are fragmented and difficult for residents to detect. Public retirement systems rarely own office towers directly. Instead, they often hold indirect exposure through commercial mortgage-backed securities, private real estate debt funds, downtown redevelopment bonds, regional banks, and office-focused real estate investment trusts. The decline in occupancy rates since the widespread adoption of remote and hybrid work has sharply reduced property cash flows, making refinancing increasingly difficult at today’s elevated interest rates.

Research from the National Council of Real Estate Investment Fiduciaries and analyses published by the Urban Land Institute during 2025 showed that office property values in many mid-sized American cities had declined between 25% and 45% from pre-pandemic peaks. In certain downtown corridors, especially older Class B and Class C office buildings, valuation declines exceeded 50%. While global gateway cities attracted most national attention, smaller metropolitan areas often faced weaker capital inflows and lower tenant demand, making recovery far slower.

Why Second-Tier Cities Are More Vulnerable

The financial ecosystem surrounding office real estate in second-tier cities differs substantially from coastal financial centers. In places like St. Louis and Cleveland, downtown office districts are frequently tied to local pension systems through tax-increment financing projects, municipal bond issuance, and regional bank lending. These cities spent decades attempting to revitalize central business districts using public-private partnerships designed around assumptions of steadily rising office occupancy and property tax revenue.

Now those assumptions are being challenged simultaneously.

According to data published by the real estate analytics firm MSCI Real Assets and occupancy tracking by Kastle Systems, office utilization rates in many mid-sized cities remained well below 2019 levels entering 2026. Average weekday office occupancy in several Midwest and Northeast metros continued to hover between 45% and 60% of pre-pandemic levels. Older office buildings lacking modern amenities experienced particularly severe tenant losses as corporations consolidated operations into newer, energy-efficient properties.

This matters because pension systems depend heavily on stable long-duration investment returns. Many regional retirement systems increased allocations to private real estate and alternative investments over the past decade after persistently low Treasury yields reduced fixed-income returns. Public pensions from Ohio, Missouri, Connecticut, and Oregon all expanded allocations to private markets between 2015 and 2024 in pursuit of higher yields capable of meeting actuarial return assumptions often exceeding 6.5% annually.

As office values decline, those assumptions become harder to sustain.

St. Louis and the Downtown Debt Spiral

In St. Louis, falling occupancy in the downtown office market has become increasingly entangled with municipal finance concerns. Several large office towers have struggled with refinancing amid rising interest rates and declining tenant demand. Reports from brokerage firms including CBRE and Colliers during late 2025 noted that vacancy rates in downtown St. Louis exceeded 30% in some submarkets, among the highest levels recorded in decades.

The city’s redevelopment strategy during the 2000s and 2010s relied heavily on tax abatements and downtown financing districts backed by projected growth in commercial property taxes. Many local pension funds and retirement-oriented investment vehicles indirectly gained exposure to this ecosystem through municipal bond holdings and regional lending institutions.

Analysts at the Government Finance Officers Association warned in several public discussions during 2025 that weakening commercial assessments could create pressure on municipal budgets already struggling with rising pension obligations. If assessed office values continue to decline, the resulting reduction in tax revenues may force local governments to redirect funds away from transit upgrades, public safety investments, and road maintenance toward pension stabilization.

The challenge becomes especially severe when office buildings enter distress simultaneously. Once a property fails refinancing or enters special servicing, valuation declines can accelerate rapidly, reducing collateral values throughout surrounding districts. This can create a cascading effect in which municipal bond-backed redevelopment districts collect lower-than-expected tax increment revenues, weakening their ability to service debt obligations.

Residents may not immediately connect deteriorating sidewalks or delayed infrastructure repairs to office vacancies downtown, but the financial relationships are increasingly direct.

Cleveland’s Pension Exposure Through Regional Banking

Cleveland illustrates another underappreciated transmission channel: regional banking exposure. Many local pension systems hold significant investments in regional financial institutions either directly through equity portfolios or indirectly through index allocations. Regional banks throughout the Midwest became major lenders to office projects during the prolonged low-rate environment of the 2010s.

According to analyses released by the Federal Deposit Insurance Corporation and the Federal Reserve Bank of Cleveland during 2025, smaller regional banks remained disproportionately exposed to commercial real estate loans relative to larger national institutions. In certain Midwest banking markets, commercial real estate loans accounted for more than 300% of total bank capital.

As office refinancing stress intensifies, pension systems can experience losses through multiple channels simultaneously: declining values in real estate debt funds, pressure on regional bank equities, and weaker municipal tax collections. Cleveland’s public pension challenges were already significant before the office downturn accelerated. Additional market stress could further widen funding gaps for city retirement systems and public worker benefits.

Researchers from the Brookings Institution and economists associated with the Lincoln Institute of Land Policy have noted that second-tier cities often lack the economic diversification necessary to quickly absorb prolonged downtown real estate weakness. Unlike larger coastal markets, these cities typically rely more heavily on local employers and regional lending networks rather than international capital inflows.

That localized dependence increases the probability that office distress spreads through broader municipal finances.

Hartford’s Insurance Economy Faces New Pressures

Hartford presents a different but equally fragile dynamic. Long known as an insurance industry hub, the city experienced substantial shifts toward hybrid work among major employers after 2020. Several insurers reduced office footprints or adopted flexible work arrangements that permanently lowered demand for downtown space.

The office market slowdown has complicated efforts to stabilize municipal finances in a city already facing fiscal constraints. Hartford’s redevelopment initiatives over the past decade frequently depended on bond structures tied to expectations of sustained commercial activity and rising downtown assessments.

Public pension systems in Connecticut have historically faced significant unfunded liabilities, prompting policymakers to seek stronger investment returns from alternative assets, including private real estate. According to annual reports from the Connecticut Retirement Plans and Trust Funds, allocations to private equity and real assets increased materially throughout the late 2010s and early 2020s.

The problem emerging in 2026 is not necessarily catastrophic immediate losses but rather the slow erosion of long-term return expectations. When office properties are refinanced at sharply lower valuations, pension funds may eventually need to recognize markdowns that reduce portfolio performance over multiple years.

This creates difficult political tradeoffs. Municipal governments may face pressure to increase pension contributions at precisely the moment when commercial property tax revenue weakens. The likely outcomes include deferred maintenance, delayed public transportation projects, or reductions in discretionary city services.

Economists at the Center for Retirement Research at Boston College have repeatedly warned that public pension systems remain highly sensitive to prolonged periods of underperformance because actuarial assumptions compound over time. Even relatively modest annual shortfalls can create major funding deficits over a decade.

Portland and the Collapse of the Urban Recovery Model

Portland’s office market deterioration has become particularly symbolic of the broader challenges facing mid-sized urban economies. While national discussions often focused on public safety concerns or migration trends, a less visible issue has been the extent to which local redevelopment financing depended on continued downtown office demand.

According to market data published during 2025 by Newmark and JLL, downtown Portland office vacancy rates reached historic highs, with some Class B properties struggling to maintain occupancy above 50%. Several prominent buildings traded at steep discounts relative to pre-pandemic valuations, reinforcing concerns about appraisal declines across the region.

The implications extend well beyond landlords. Oregon’s public pension system, like many others, maintains diversified exposure across private real estate, infrastructure funds, and institutional investment vehicles tied to urban redevelopment projects. In addition, local governments throughout the Portland metropolitan area relied on projected property tax growth to support long-term capital planning.

As valuations weaken, borrowing costs for municipalities may rise because investors begin questioning future tax base stability. Credit rating agencies have increasingly monitored the exposure of local governments to commercial real estate concentration. Analysts from Moody’s Ratings and S&P Global Ratings noted during 2025 that cities with prolonged office market weakness could experience greater fiscal pressure if downtown tax collections continue declining.

For residents, the consequences may emerge gradually rather than through sudden crisis. Transit expansion plans may be postponed. Water infrastructure upgrades may face delays. Public employee hiring could slow. Parks maintenance budgets may tighten. These incremental adjustments rarely generate national headlines, but they shape the long-term quality of urban life.

The Refinancing Wall Arrives

A major driver of current stress is the enormous refinancing wave confronting office owners between 2025 and 2027. During the low-rate years before 2022, many office properties were financed using assumptions that now appear unrealistic. Buildings purchased at extremely low capitalization rates suddenly face refinancing costs several hundred basis points higher while generating weaker rental income.

According to the Mortgage Bankers Association, hundreds of billions of dollars in commercial mortgages are scheduled to mature between 2026 and 2028. Office properties represent one of the most vulnerable segments because occupancy recovery has remained uneven.

In second-tier cities, refinancing becomes even harder because lenders are more cautious about local economic prospects. Institutional investors increasingly favor trophy properties in globally connected cities while reducing exposure to older downtown assets in smaller metropolitan regions.

That leaves pension-linked investment funds vulnerable to prolonged valuation stagnation. Unlike publicly traded securities, private real estate valuations often adjust slowly, meaning pension systems may not immediately reflect losses on balance sheets. Critics argue this accounting lag risks understating the scale of future funding pressure.

Researchers from the Urban Institute and the Pension Research Council at the University of Pennsylvania have highlighted how smoothing mechanisms in pension accounting can delay recognition of market stress, potentially pushing financial burdens into future municipal budgets.

The Local Taxpayer as Shock Absorber

The most significant aspect of the unfolding office valuation crisis may be who ultimately absorbs the losses. In many cases, local residents become the financial backstop even if they never owned a single office building.

When pension returns underperform, governments typically face limited options: increase contributions, reduce benefits for future workers, raise taxes, borrow more heavily, or cut spending elsewhere. Because pension obligations are legally protected in many states, infrastructure and discretionary services often become the adjustment mechanism.

This dynamic is particularly dangerous in cities already facing population stagnation or declining tax bases. If rising taxes encourage further outmigration while office valuations continue falling, municipalities can enter a reinforcing cycle of fiscal stress.

Public finance scholars including researchers from the Volcker Alliance and the Pew Charitable Trusts have warned that pension underfunding and commercial real estate weakness could increasingly interact over the remainder of the decade. The relationship remains poorly understood by most residents because the exposures are dispersed across bonds, private funds, and institutional investment structures rather than visible through direct property ownership.

By May 2026, the office downturn in America’s second-tier cities is no longer simply a commercial real estate story. It is becoming a municipal finance story, a pension stability story, and increasingly a public services story. The empty office towers standing over downtown districts from St. Louis to Hartford represent more than failed workplace assumptions. They are emerging as stress points in the financial architecture supporting roads, pensions, transit systems, and basic urban governance itself.

If you have enjoyed reading, spread the word:

Private Credit’s Secret Banking Backbone Is Growing Faster Than Anyone Expected

America's $5 Trillion Business Handoff Has Already Begun

The Repair Economy Boom in Rural America

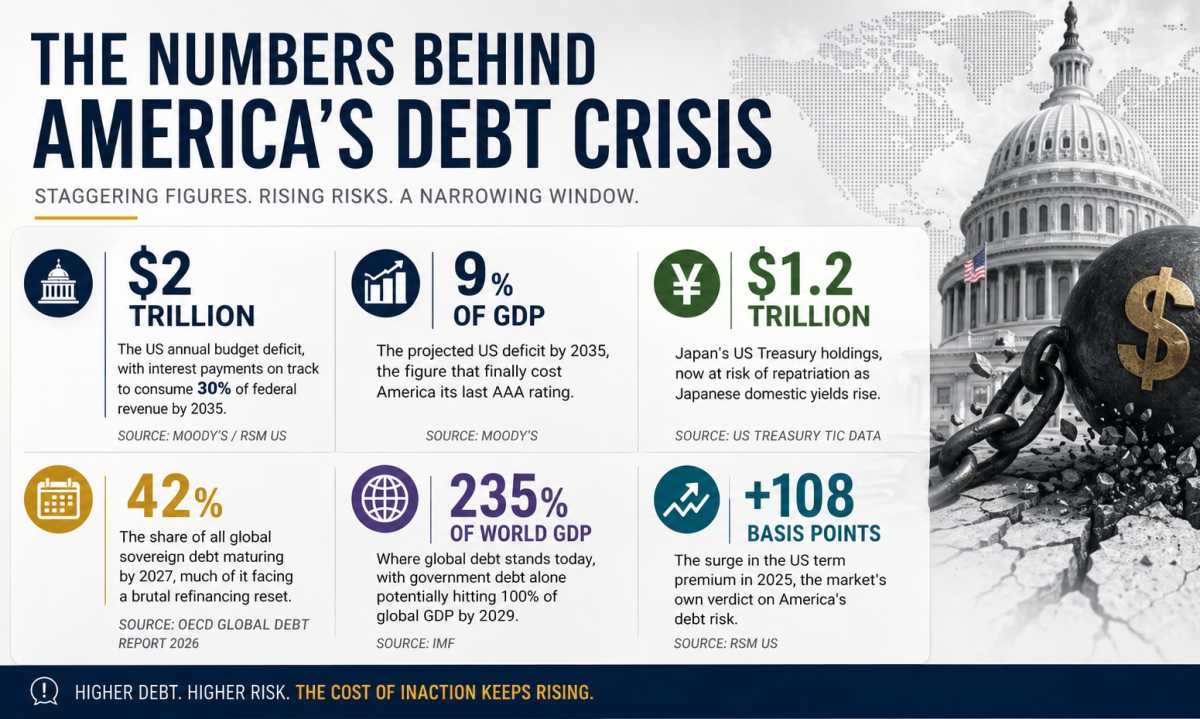

Debt, Deficits & Disaster: The Bond Market Crisis