Good prospects:

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

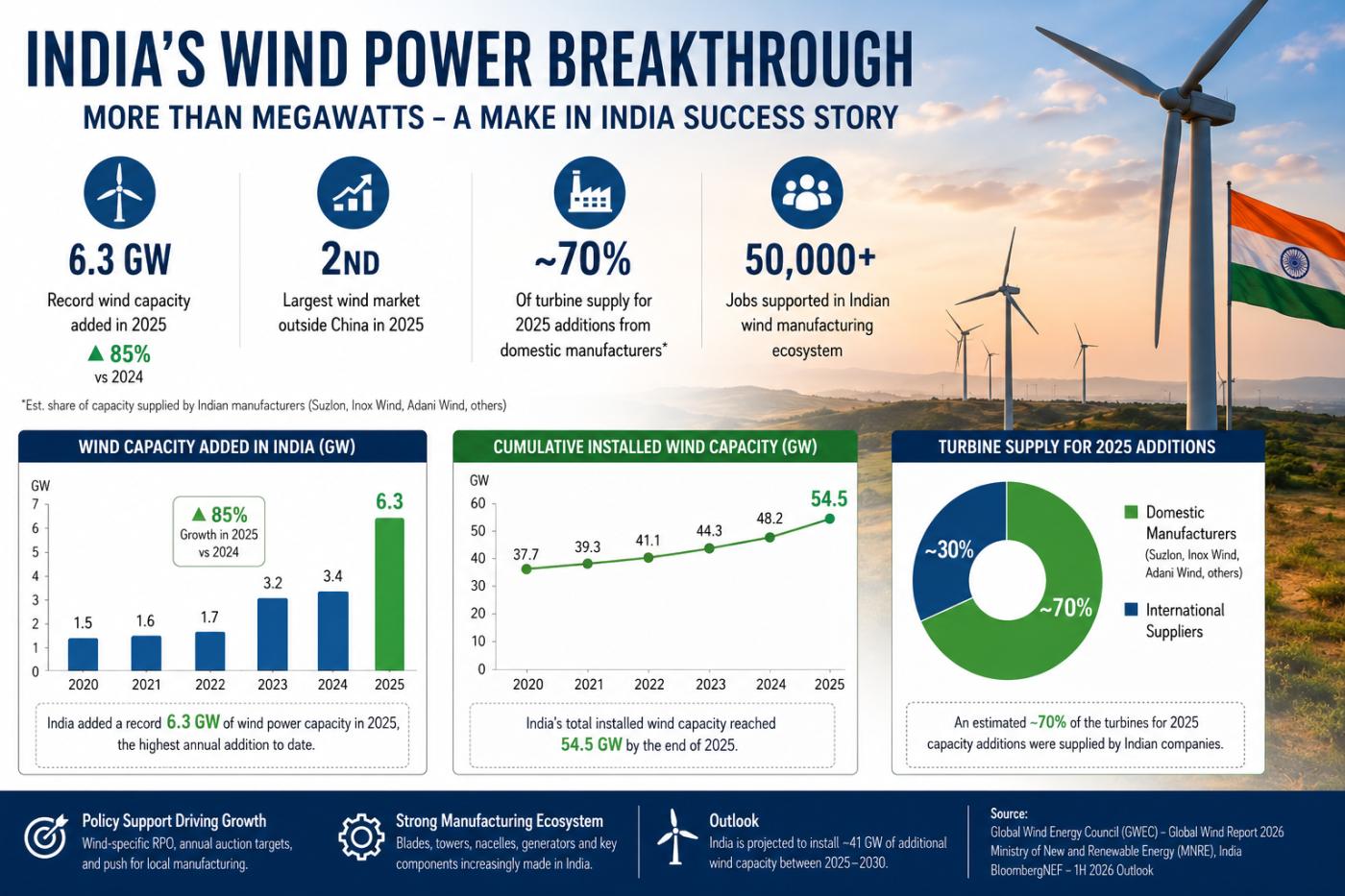

The Renewable Success Story Beyond Solar

Startups Mint India’s New Billionaires

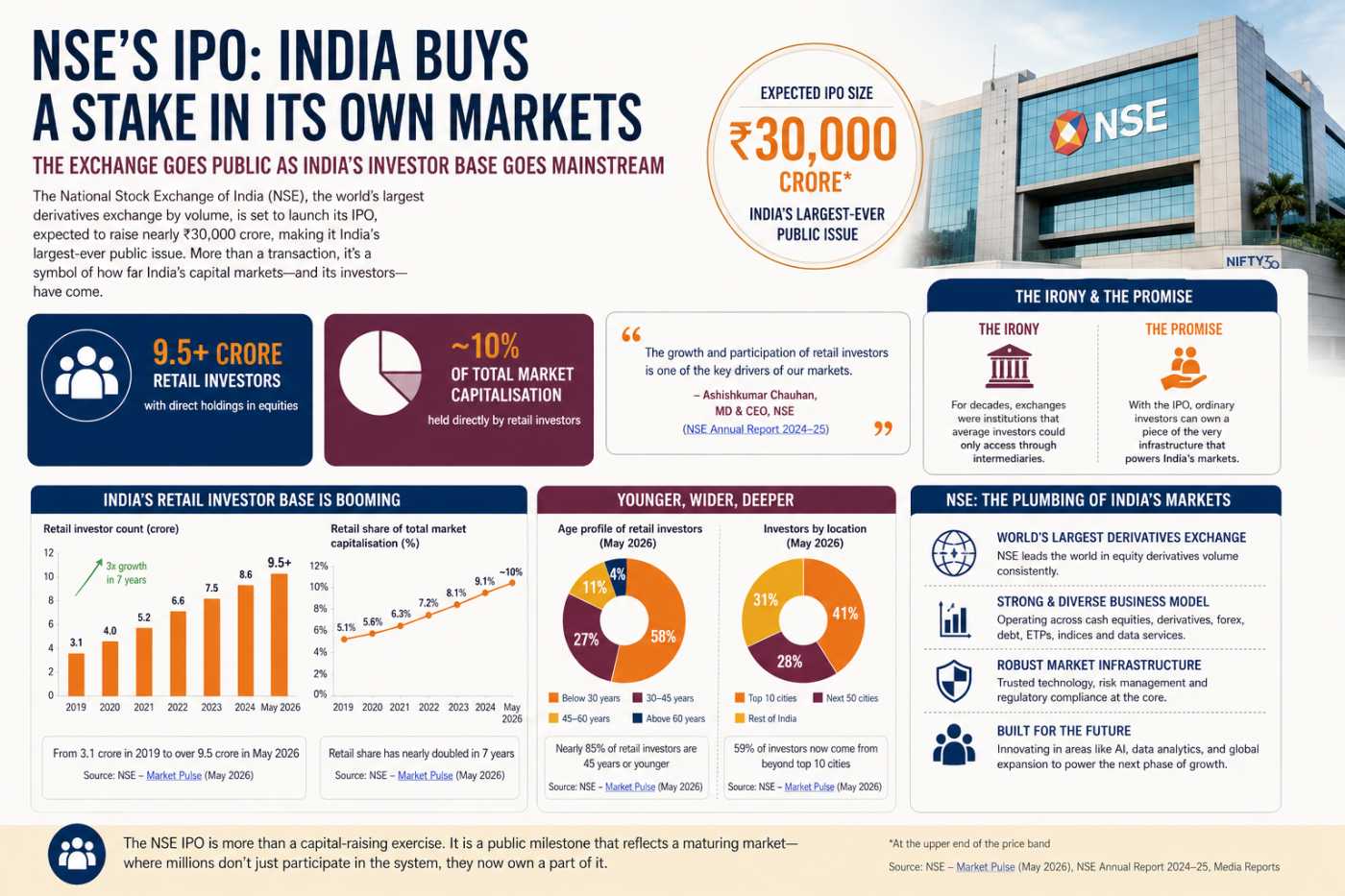

India's Biggest IPO Has a Bigger Meaning

From Watches to Wealth: Titan's New Empire

SEBI's New Gateway Is Rewiring Foreign Investment in India

Tier 2 Towns Are Outsaving India's Big Metros

For decades, India's financial geography ran on a simple script: ambition flowed toward four or five cities, and money followed close behind. Bengaluru, Mumbai, Delhi-NCR, Hyderabad and Pune absorbed the country's best-paid jobs, its biggest mutual fund branches and most of its disposable income. As of June 2026, that script is being quietly rewritten. A growing body of data on remote work, gig employment and retail investing suggests that India's financial centre of gravity is shifting outward, away from its five or six traditional capitals and into a constellation of Tier 2 and Tier 3 towns that were, until recently, treated as financial afterthoughts.

The Old Employment Compact Is Breaking

The most candid articulation of this shift has come not from a government white paper but from a working economist watching the data in real time. Marcellus Investment Managers founder Saurabh Mukherjea has spent much of 2026 arguing that India's traditional white-collar employment model is structurally weakening, and that the replacement is not unemployment but a more dispersed, flexible form of earning. Speaking to ETV Bharat earlier this year, Mukherjea pointed to a set of uncomfortable numbers: India's household savings rate sitting near a five-decade low, and a middle-class debt-to-income ratio of roughly 32 to 33 percent once home loans are stripped out, compared with under 20 percent in most large economies. "While writing Breakpoint, we met people carrying multiple personal loans just to manage expenses," he said, describing a middle class leaning on credit cards, personal loans and education loans to sustain lifestyles that real wage growth can no longer support on its own.

His prescription is not pessimistic, though. At a fireside chat in Seattle in early June, hosted by Remitly for its Prose and Kauns series, Mukherjea sketched out what he sees as the logical endpoint of this transition: a generation of Indians who no longer need to migrate to a handful of metros to build a career. "Let me stay in my hometown, do gig work across the world, earn money, build a small business if they want. That'll be the future," he told the audience, framing remote and gig work not as a fallback option but as a deliberate strategy for financial resilience in smaller, cheaper cities. The logic is straightforward: lower rent, lower commuting costs and lower overall cost of living in a Tier 2 or Tier 3 town can offset a salary that might look modest by Mumbai or Bengaluru standards, while global gig and freelance income, paid largely in dollars or pounds, stretches considerably further once converted into rupees and spent locally.

Gig Work, By the Numbers

This is not merely anecdotal optimism from one fund manager. India's gig and platform workforce has been one of the fastest-growing segments of the labour market over the past five years. According to the Economic Survey 2025-26, the gig workforce expanded to roughly 12 million workers in FY2025, a 55 percent jump from FY2021, and the original projections in the landmark NITI Aayog report on India's gig and platform economy put the workforce on a path to 23.5 million by 2029-30, accounting for nearly 7 percent of the non-agricultural workforce. Crucially, this growth is no longer concentrated in food delivery and ride-hailing alone. Medium- and high-skilled gig work, spanning IT, design, beauty services, tutoring and home repair, now makes up more than half of all gig employment, and a meaningful share of it is explicitly enabled by location-agnostic platforms that do not require a worker to live anywhere near a metro.

The demographic detail matters as much as the headline number. The Economic Survey also recorded a rise in female labour force participation to 41.7 percent, a shift partly attributed to gig and platform work that lets women earn without a daily commute to a fixed office, a structural barrier that has historically suppressed women's workforce participation outside major cities. Roughly a quarter of India's gig workforce is now female, with a disproportionate share engaged through home-based and hyperlocal service platforms in precisely the Tier 2 and Tier 3 markets that are emerging as the new financial frontier. Put together, the labour data and the migration commentary point in the same direction: work is decoupling from geography faster than India's financial infrastructure has historically assumed it would.

Where the Money Is Actually Going

The more interesting evidence, for anyone tracking household wealth-building rather than just employment trends, sits inside India's mutual fund flows. Mutual fund distributors classify Indian cities into two buckets: T30, the top 30 cities by assets under management, and B30, everything beyond them. For years, B30 was treated as a slow-growing, low-priority segment. That has changed sharply. According to data from the Association of Mutual Funds in India (AMFI) cited by Outlook Money, investors from beyond the top 30 cities accounted for 27.6 percent of total individual mutual fund assets as of February 2026. More tellingly, Systematic Investment Plan volumes originating in Tier 2 and Tier 3 cities have now overtaken those from the top 30 cities altogether, and new SIP registrations from smaller towns made up 56 percent of all incoming volumes in the same period.

Industry-wide AUM figures reinforce the same pattern. India's mutual fund industry held net assets of roughly Rs 81.58 lakh crore in May 2026, with monthly SIP contributions crossing Rs 30,000 crore for the third consecutive month, a 16 percent year-on-year increase even amid a turbulent macro backdrop of currency volatility and stalled US-Iran negotiations. B30 cities are increasingly the engine behind that resilience, now contributing close to a fifth of total industry AUM and, by some industry estimates, nearly 58 percent of all incremental SIP additions. Distribution has had to follow the money: Nippon India Asset Management's recent expansion of services into Leh, a town in Ladakh historically considered too remote for formal asset management infrastructure, is a small but symbolically significant marker of how far this geographic broadening has travelled. Fintech platforms such as Groww, Zerodha and ET Money, along with AMC-led digital onboarding tools, have done much of the heavy lifting by collapsing what used to be a multi-day, paperwork-heavy account-opening process into something that can be completed on a smartphone in a regional language.

Tier 2 and 3 Cities as the New Financial Frontier

What makes this shift worth dwelling on is not just that smaller cities are investing more, but what that investing represents. A household in Indore, Coimbatore or Jaipur that opens a SIP today is not simply diversifying a portfolio; it is, in many cases, formalising savings that would previously have gone into gold, land or an informal chit fund. NITI Aayog's vice chairman Suman Bery, speaking at the launch of the gig economy report that underpins much of today's policy thinking, described the underlying ambition plainly: the goal was to create "a valuable knowledge resource in understanding the potential of the sector," one that would let policymakers and markets alike take the geographic dispersion of work and income seriously rather than treating it as a rounding error. That dispersion is now visible in hard numbers rather than aspiration.

The consumption side tells a parallel story, even if it is harder to capture in a single statistic. As remote and gig income flows into smaller cities, local retail, real estate and services sectors in those towns are absorbing demand that would once have been captured exclusively by metro economies. A professional who relocates from Bengaluru to Mysuru or from Gurugram to Dehradun does not stop earning at metro-adjacent rates, particularly if a meaningful share of that income is gig-based and globally sourced, but they do redirect almost all of their spending and a growing share of their long-term savings into a Tier 2 or Tier 3 local economy. Over time, that redirection compounds into demand for better housing stock, more sophisticated retail formats and, eventually, more financial advisory capacity in towns that previously had none.

The Nuance That Gets Lost in the Headlines

None of this should be read as a frictionless success story, and the data itself carries useful caveats. The average mutual fund ticket size in B30 cities remains meaningfully smaller than in T30 cities, reflecting both lower average incomes and, more importantly, lower financial literacy. Outlook Money's reporting on the AMFI data flags this directly: many first-time investors in smaller towns lack a clear understanding of risk, product structure or long-term investment strategy, and often rely on informal peer advice rather than professional guidance. That gap matters because it shapes whether this new wave of small-town investing translates into durable wealth-building or into a more volatile, trend-chasing pattern of participation. SEBI's continued push on advertising guidelines, simplified disclosure norms and initiatives like AMFI's Chhoti SIP, which allows contributions as low as Rs 250 a month, are explicit attempts to narrow that gap rather than simply chase headline growth numbers.

There is also the harder structural issue Mukherjea raises: a rising debt-to-income ratio and a depressed household savings rate are not signs of a uniformly healthy transition. The small-town boom and the gig economy's growth are, in part, adaptive responses to a labour market that is no longer generating enough stable, well-paying jobs in the cities that used to absorb India's aspirational workforce. Framing this purely as an opportunity risks understating the pressure that is driving people toward it in the first place.

What It Means for the Next Phase of Household Wealth

Even with those caveats, the directional evidence is hard to dismiss. India's financial capitals are no longer the sole gravitational centres for either income or investment. Gig and remote work have made it economically rational, in a growing number of cases, to live in a smaller, cheaper city while earning at rates pegged to a metro, a global client base, or both. Mutual fund flows, SIP registrations and even niche moves like Nippon's Leh expansion are early but consistent evidence that the savings and investment infrastructure of the country is following that population shift rather than waiting for people to come to it. For households outside India's traditional financial capitals, the practical implication is that access to formal wealth-building tools, SIPs, digital brokerages, insurance and credit products, is arriving at a pace that would have been unthinkable a decade ago, even if awareness and advisory support still have real ground to cover before that access becomes durable financial security.

If you have enjoyed reading, spread the word:

Why Japan Backs India’s Truckers

India's $69B Eurasian Trade Power Play

Why Oman Is Now India's Most Strategic Trade Partner

Infrastructure Bet Fuels Cement Surge