Good prospects:

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

Startups Mint India’s New Billionaires

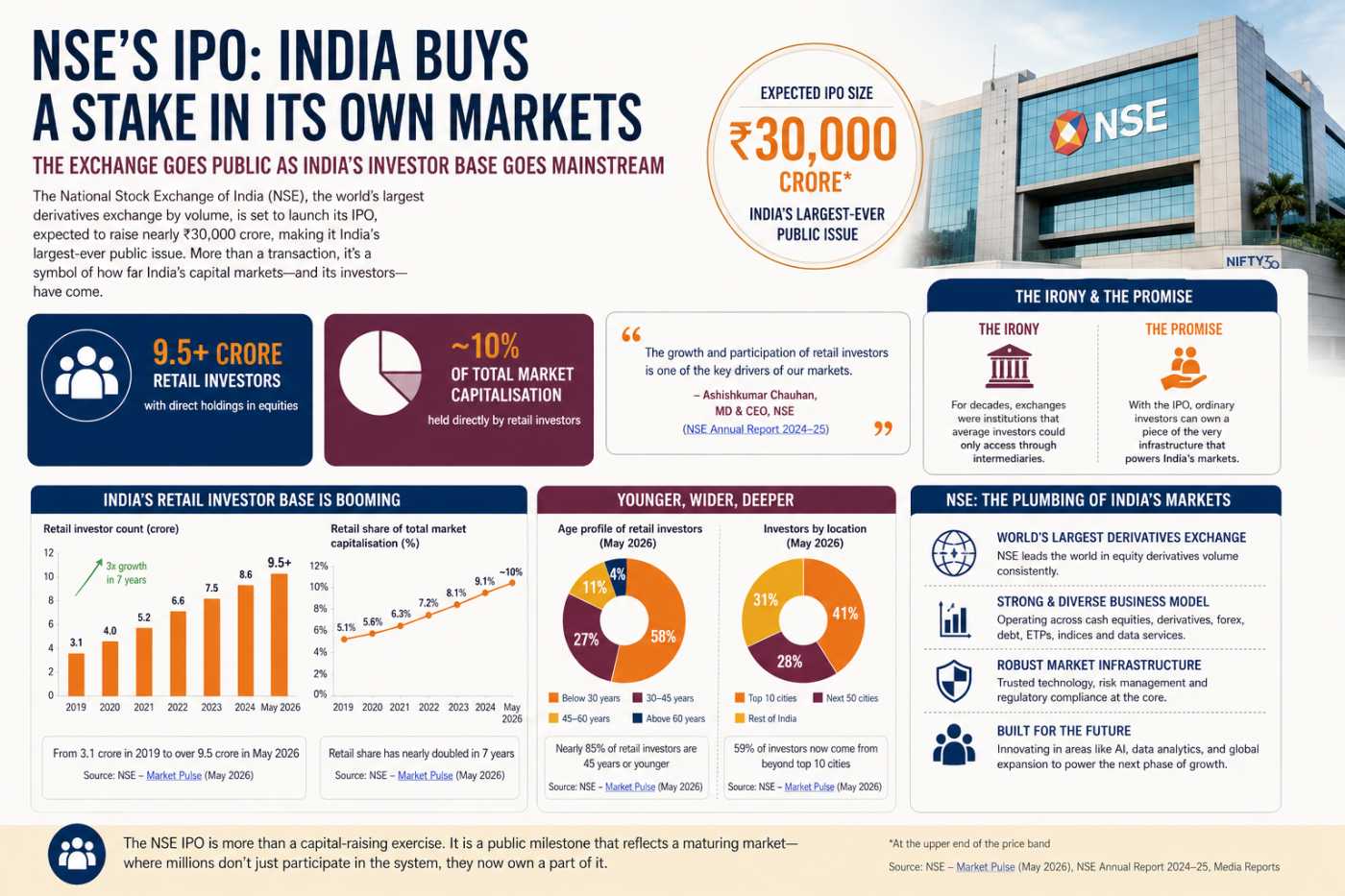

India's Biggest IPO Has a Bigger Meaning

From Watches to Wealth: Titan's New Empire

SEBI's New Gateway Is Rewiring Foreign Investment in India

Why Japan Backs India’s Truckers

The Renewable Success Story Beyond Solar

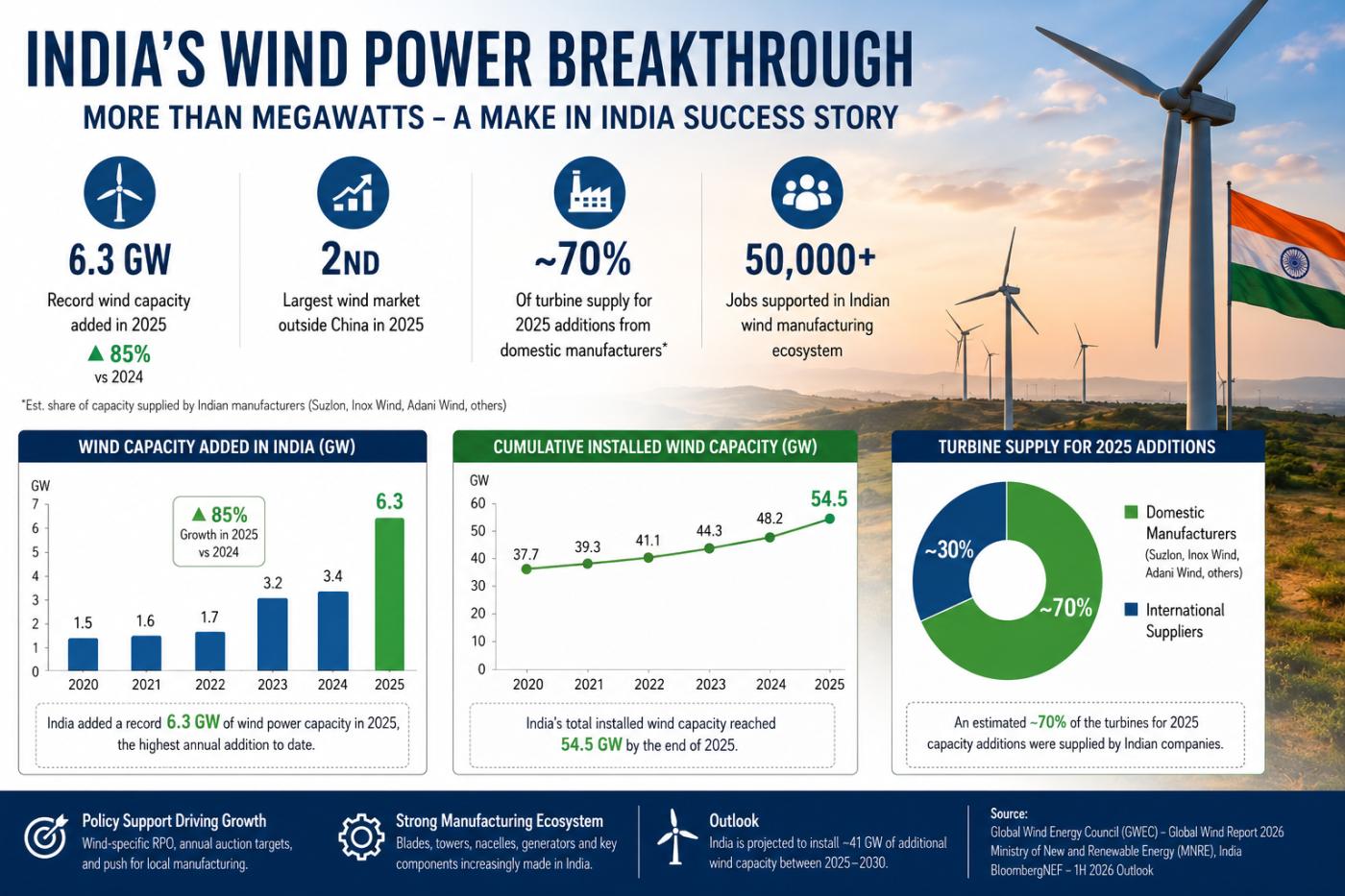

The Record That Matters Is Not 6.3 GW It Is Who Built It

India's wind power sector delivered a headline-grabbing achievement in 2025, commissioning a record 6.3 gigawatts (GW) of new capacity, an increase of roughly 85% from the previous year. According to data published by BloombergNEF and the Global Wind Energy Council (GWEC), the surge made India the largest wind market outside China and one of the fastest-growing renewable energy markets in the world.

Yet the most important development may not be the capacity itself. The deeper story is that a growing share of the turbines, blades, towers, nacelles and supporting equipment powering this expansion are increasingly being designed and manufactured in India. After years in which imported technology and foreign suppliers dominated large portions of the value chain, domestic companies such as Suzlon, Inox Wind and Adani Wind are capturing a larger share of the market and helping transform renewable deployment into an industrial manufacturing story.

This distinction matters. Countries can install renewable energy while remaining dependent on imported equipment. Building a domestic manufacturing ecosystem, however, creates skilled jobs, strengthens supply-chain resilience, improves trade balances and develops engineering capabilities that can spill over into other industries. In that sense, India's wind sector is becoming one of the clearest examples of what a successful "Make in India" strategy can look like beyond the heavily discussed solar manufacturing industry.

Why Wind Is Different From Solar

Much of India's renewable-energy manufacturing conversation over the past several years has focused on solar modules, solar cells and the country's efforts to reduce dependence on Chinese imports. Wind energy, however, presents a different challenge.

A modern wind turbine is a highly complex industrial product involving advanced materials, precision engineering, power electronics, bearings, gearboxes, generators, software systems and large-scale fabrication capabilities. Unlike solar panels, where global manufacturing is heavily concentrated in a handful of countries, wind turbines require substantial local industrial infrastructure because of their size and transportation requirements.

Wind-turbine blades can exceed 80 meters in length. Towers weigh hundreds of tonnes. Transporting these components across oceans and continents is expensive and logistically challenging. As a result, countries with large wind markets often develop domestic manufacturing ecosystems around them.

India had a head start in this regard. The country developed an indigenous wind industry decades ago, but growth slowed during parts of the late 2010s and early 2020s as policy changes, auction structures and market uncertainty disrupted investment cycles. The strong rebound in 2025 is therefore significant not only because installations accelerated but because domestic manufacturers were positioned to benefit from the recovery.

An Established Supply Chain Starts Paying Off

According to GWEC's Global Wind Report 2026, India now possesses an established local wind-energy supply chain and is expected to install roughly 41 GW of additional wind capacity through 2030. The report specifically highlighted the country's local manufacturing capabilities as one of the foundations supporting future growth.

India's cumulative installed wind capacity reached approximately 54.5 GW by the end of 2025, while annual additions hit a historic high of 6.3 GW. The growth was supported by wind-specific renewable purchase obligations, annual auction targets and expanding demand for hybrid renewable-energy projects that combine wind, solar and battery storage technologies.

More importantly, domestic manufacturers increasingly participated in fulfilling this demand. BloombergNEF noted that European and American manufacturers have been losing ground in India's turbine-order market relative to Asian suppliers, a trend that has benefited Indian companies such as Suzlon and Inox Wind. While Chinese suppliers remain important participants, local firms are no longer merely surviving they are expanding alongside the market.

That represents a meaningful shift from earlier periods when many observers questioned whether India's domestic turbine manufacturers could remain competitive against larger global players.

Suzlon's Revival Reflects a Broader Industrial Trend

No company better illustrates the transformation than Suzlon. Once viewed primarily through the lens of financial restructuring and debt challenges, the company has re-emerged as one of the key beneficiaries of India's wind revival.

Suzlon's recent order-book growth demonstrates that domestic manufacturers are increasingly winning large-scale commercial and industrial projects. These projects are not being secured because developers are forced to buy locally. Rather, Indian manufacturers have become capable of competing on technology, service networks, local execution expertise and supply-chain responsiveness.

The company's recovery also reveals an often-overlooked feature of renewable-energy manufacturing: scale matters. Once a domestic manufacturer reaches sufficient volume, it can support local suppliers, attract component investments and create engineering ecosystems that reinforce competitiveness.

The result is a virtuous cycle. More installations create more manufacturing demand. More manufacturing demand encourages supplier investments. Greater supplier density lowers costs and improves responsiveness, which in turn supports additional installations.

Inox Wind and the Rise of Domestic Competition

The story is not limited to one company. Inox Wind has also emerged as a significant participant in India's wind-energy expansion, securing new partnerships and project pipelines as demand increases.

The presence of multiple competitive domestic manufacturers is critical. A manufacturing strategy built around a single national champion can create vulnerabilities. A broader ecosystem featuring multiple turbine makers, component suppliers, engineering firms and project developers is more resilient and better positioned for long-term growth.

Competition between domestic firms also drives innovation. Turbine ratings continue to increase, operational efficiency improves and maintenance costs decline as manufacturers attempt to differentiate themselves. These dynamics help India's renewable-energy ambitions while simultaneously strengthening industrial capabilities.

The Policy Shift Toward Localisation

Government policy has increasingly reinforced this trend. In 2025, India introduced new requirements aimed at strengthening domestic participation in wind-turbine manufacturing. The rules require key components including blades, towers, generators, gearboxes and certain specialized parts to be sourced through approved domestic supply chains, while also imposing data-localization and operational-control requirements.

These measures differ from traditional protectionist policies. Instead of simply restricting imports, they attempt to ensure that critical industrial capabilities remain within India. Policymakers appear increasingly focused on supply-chain security, technological sovereignty and long-term industrial development rather than only short-term installation targets.

This reflects a broader shift in global industrial policy. The United States, European Union and China have all adopted measures linking clean-energy deployment with domestic manufacturing objectives. India's wind-sector policies increasingly align with this global trend.

Why Wind Manufacturing Matters More Than Many Realize

Wind manufacturing generates economic benefits that extend far beyond electricity production. A utility-scale wind project requires steel fabrication, heavy engineering, transportation services, electrical equipment, software systems, construction expertise and long-term maintenance operations.

Each turbine deployed creates demand across numerous industrial sectors. Tower manufacturing supports steel producers. Blade manufacturing creates advanced-composite industries. Generator production strengthens electrical-equipment capabilities. Maintenance requirements support long-term technical employment.

In other words, every gigawatt of domestically manufactured wind capacity produces a larger economic footprint than a simple capacity statistic suggests.

This is particularly important for India because the country seeks not only to decarbonize but also to expand manufacturing employment. Renewable energy is increasingly being viewed as an industrial-development strategy rather than merely an environmental policy.

The Strategic Lesson Beyond Solar Panels

The success of wind localisation offers a broader lesson for Indian industrial policy. Solar manufacturing often receives the most attention because of the country's effort to reduce import dependence. However, wind may ultimately provide a more complete demonstration of industrial self-reliance because the value chain is deeper and technologically more complex.

Building competitive capabilities in turbines, gearboxes, generators and power electronics requires engineering expertise that can spill over into aerospace, transportation, industrial machinery and grid technologies.

That makes wind manufacturing strategically valuable in ways that are not always captured by renewable-energy statistics.

As Ben Backwell, Chief Executive Officer of the Global Wind Energy Council, observed while discussing the sector's global growth, "the wind sector has demonstrated its ability to scale at speed." India's experience suggests that the ability to scale manufacturing may ultimately prove just as important as the ability to scale generation capacity.

The Next Challenge: Moving Up the Technology Ladder

The next phase of India's wind story will not be determined solely by installation numbers. It will depend on whether domestic manufacturers can move further up the technology ladder.

Future competitiveness will require larger turbine platforms, advanced digital monitoring systems, offshore-wind capabilities, next-generation materials and stronger export competitiveness. India's manufacturers have made substantial progress in establishing domestic market positions, but global leadership requires continuous innovation.

The opportunity is significant. GWEC projects continued growth in India's wind market through the remainder of the decade, while policymakers continue targeting 500 GW of non-fossil-fuel capacity by 2030. If domestic manufacturers capture a substantial portion of this growth, the sector could evolve from a domestic success story into an export-oriented industrial platform.

Viewed through that lens, India's record 6.3 GW installation figure becomes less important than the industrial transformation occurring behind it. The turbines spinning across Gujarat, Tamil Nadu, Karnataka and Rajasthan are generating more than electricity. They are helping build engineering expertise, manufacturing capacity and supply-chain resilience.

For years, India's renewable-energy narrative was largely about deployment. Increasingly, it is becoming a story about production. The country's wind sector suggests that the most valuable output of the energy transition may not simply be clean power, but the industrial capabilities created along the way.

Sources cited in reporting include the Global Wind Energy Council (GWEC) Global Wind Report 2026, BloombergNEF market analysis, India's Ministry of New and Renewable Energy, Reuters reporting by Rajendra Jadhav, and reporting by Nandini Keshari in Business Standard. For original source material, see GWEC, Reuters, and Business Standard.

If you have enjoyed reading, spread the word:

India's $69B Eurasian Trade Power Play

Why Oman Is Now India's Most Strategic Trade Partner

Infrastructure Bet Fuels Cement Surge

Apollo FY26: When Healthcare Becomes a Flywheel