More about Delhivery Limited

Fundamentals for Delhivery Limited

Regulatory Filings for Delhivery Limited

Apollo FY26: When Healthcare Becomes a Flywheel

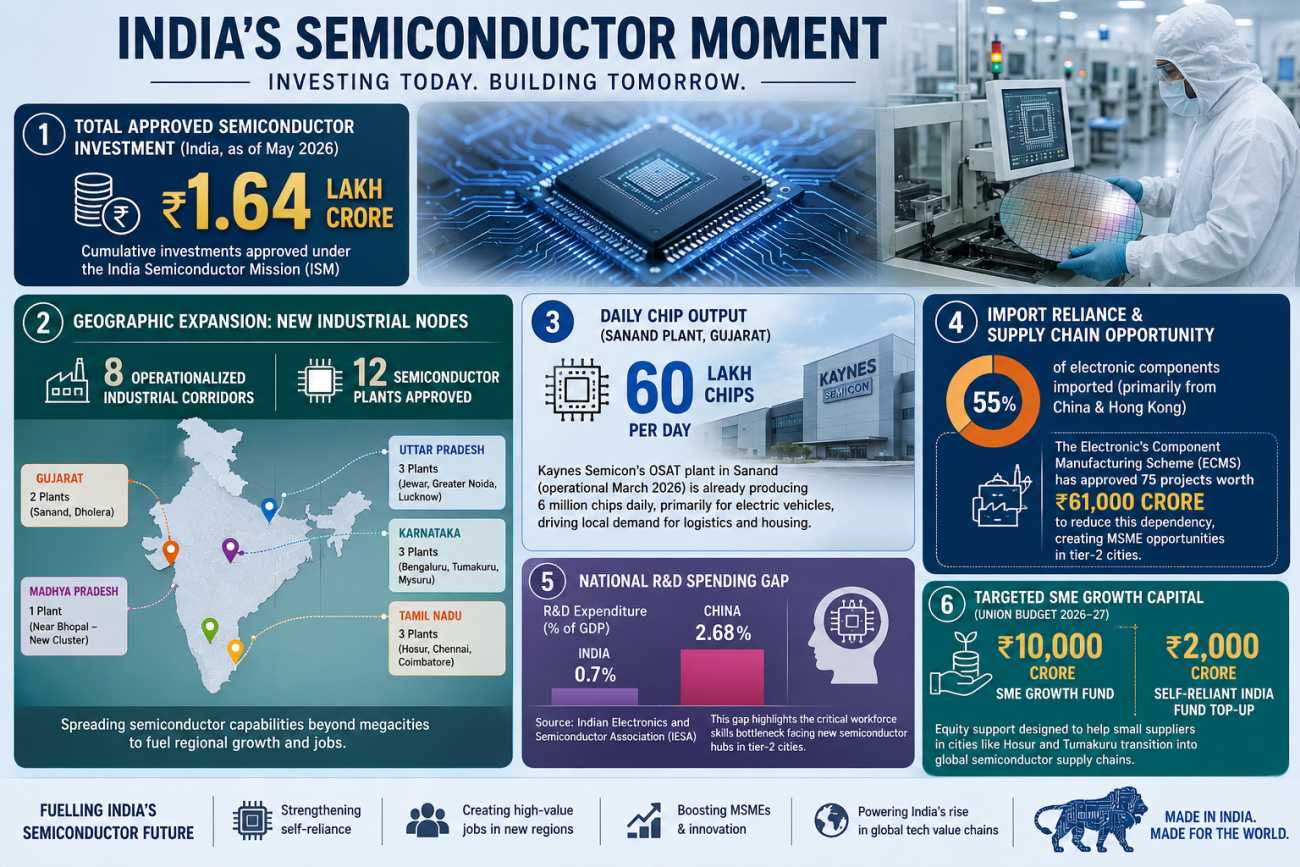

NITI Blueprint Could Turn Brain Drain Into $135Bn Engine

RAINMUMBAI Turns Rain Into a Financial Asset

India’s IT Sector Faces a Historic Breaking Point

Fundamentals for Delhivery Limited

|fundrankingplaceholder|

|techrankingplaceholder|

Business Operations:

Sector: IndustrialsIndustry: Integrated Freight & Logistics

Delhivery Limited provides supply chain solutions to e-commerce marketplaces, direct-to-consumer e-tailers, enterprises, FMCG, consumer durables, consumer electronics, lifestyle, retail, automotive and manufacturing industries in India. The company offers logistics services, including express parcel delivery, heavy goods delivery, part truckload freight, truckload freight, warehousing supply chain solutions, cross-border express, and freight services; supply chain software; and e-commerce return services, payment collection and processing, and fraud detection services. Delhivery Limited was incorporated in 2011 and is based in Gurugram, India.

Revenue projections:

With DELHIVERY's revenues forecasted to be lower than last year's, investors are expected to be cautious. A decline in revenue typically harms the company's bottom line, reducing profitability and making investors less confident about the company's ability to sustain its financial health.

Financial Ratios:

| currentRatio | 2.588000 |

|---|---|

| forwardPE | 42.103447 |

| debtToEquity | 15.098000 |

| earningsGrowth | -0.006000 |

| revenueGrowth | 0.300000 |

| grossMargins | 0.847310 |

| operatingMargins | 0.010860 |

| trailingEps | 2.000000 |

| forwardEps | 11.008600 |

DELHIVERY's current ratio being 2.588 suggests the company will have no issues paying off its short-term debt. With sufficient cash reserves and current assets, DELHIVERY can easily cover its immediate liabilities, reflecting solid financial health.

DELHIVERY's low Debt-to-Equity ratio demonstrates that the company maintains a healthy balance between equity and debt, avoiding over-leverage. This suggests a low-risk financial profile, giving investors confidence in the company's stability and ability to manage its financial commitments.

With a forward EPS greater than its trailing EPS, Delhivery Limited is expected to see higher profitability this year. The forecasted increase in earnings reflects optimism about the company's financial growth and potential for improved performance over the prior year.

Price projections:

DELHIVERY's price projections have been revised higher over time, reflecting increased confidence in the company's future potential. This steady upward trend suggests analysts expect DELHIVERY to continue its positive trajectory.

Recommendation changes over time:

Analysts' buy bias toward DELHIVERY suggests the stock is seen as a solid investment, potentially motivating investors to consider it for their portfolios. With this positive outlook, DELHIVERY is likely to be viewed as a secure place to allocate funds, driving further interest in the stock.

If you have enjoyed reading, spread the word:

Good prospects:

Companies with the best and the worst fundamentals.

Latest Regulatory Filings for NSE500

Companies with the best and the worst technicals.

How Independent Directors Failed Rs 2,500 Crore in Value

India’s Stock Market May Be Sitting on a Trap

Beyond Sugar: India's Bio-Economy Bets Big on Biofuel